Economic slowdown, rate cuts weigh on listed banks

By Isa Jane D. Acabal, Researcher

By Isa Jane D. Acabal, Researcher

LISTED big banks fell in the fourth quarter of 2025 as weak economic growth dampened investors’ sentiment and policy rate cuts put pressure on banks’ lending margins, analysts said.

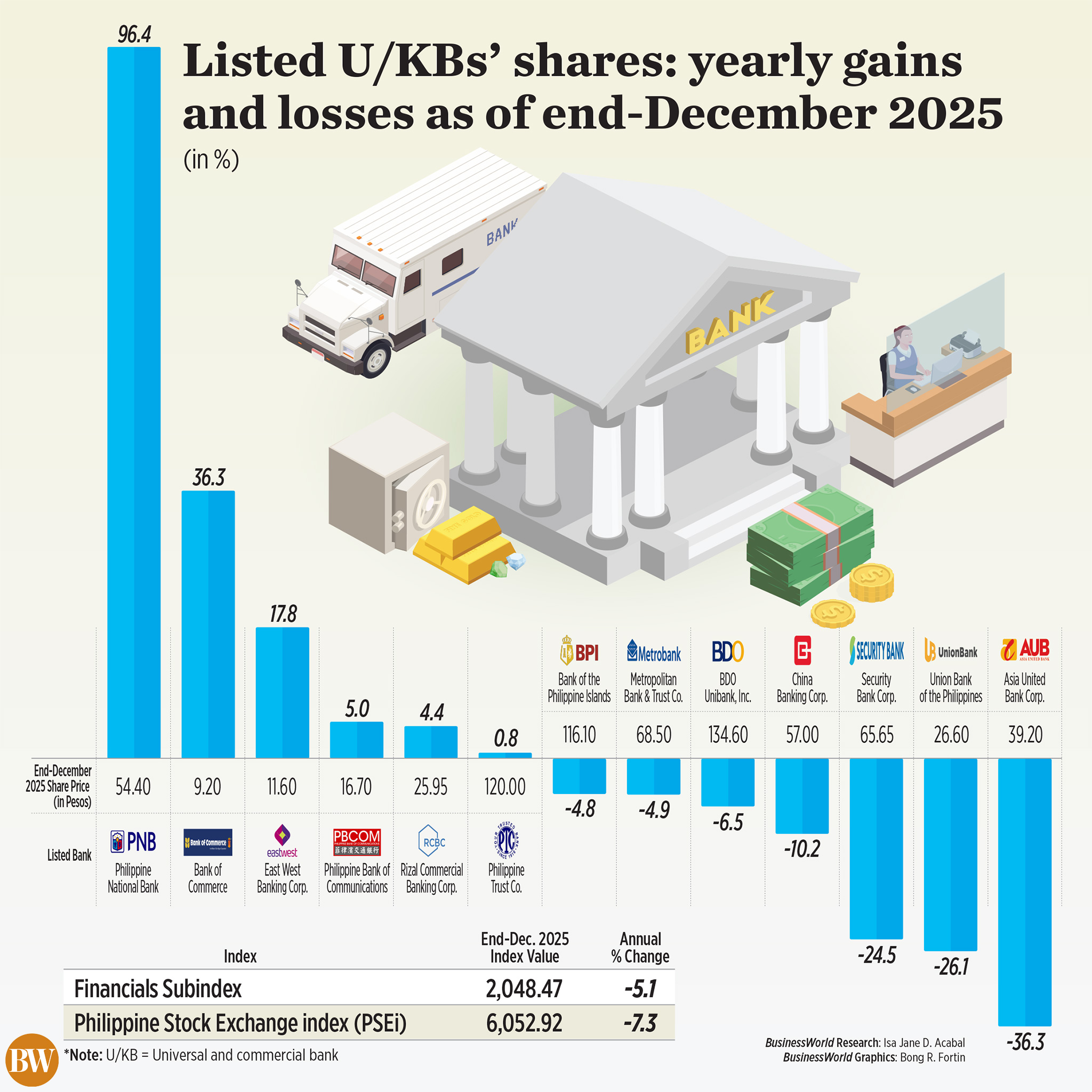

The Philippine Stock Exchange index (PSEi) inched down by 7.3% year on year to 6,052.92 at the end of the fourth quarter.

Meanwhile, the financials subindex, which includes the banks, also declined by 5.1% annually to 2,048.47 during the quarter.

As of end-December, the share prices of seven out of 13 listed universal and commercial banks (U/KBs) contracted year on year.

Among the decliners were Asia United Bank Corp. (AUB), Union Bank of the Philippines and Security Bank Corp.

On the other hand, six listed U/KBs posted annual growth in their share prices during the period.

In a statement sent to BusinessWorld, AUB President Manuel A. Gomez, AUB’s price movement resulted from the 100% stock dividend declared on June 2025.

“This dividend doubled the number of outstanding shares, so the PSE automatically adjusted our stock price on the July 24 ex-dividend date to keep the overall market value balanced. AUB’s closing price before the adjustment (July 23, 2025) was P91.50, meaning the base price was adjusted to P45.75 per share. Payment date was on August 15, 2025 to shareholders as of July 25, 2025, record date,” Mr. Gomez said in an e-mail.

“When evaluating the stock’s performance, AUB actually experienced growth, not a decline, during this period. In December 2024, its normalized price was P30.75 (which was P61.50 per share pre-stock dividend),” he added.

“By the end of December 2025, this price increased to P39.20 per share, a 27% increase year-on-year.”

Aggregate net income of U/KBs grew 4.1% to P381.18 billion as of end-December from P366.02 billion in the same period in 2024, data from the Bangko Sentral ng Pilipinas (BSP) showed.

Gross total loan portfolio of these big lenders rose by 11.2% to P15.80 trillion as of end-December 2025 from P14.20 trillion in the previous year.

The big bank’s gross nonperforming loan (NPL) ratio narrowed down to 2.80% as of end-December 2025 from 2.99% a year ago.

The big banks’ net interest margin (NIM) — a ratio that measures banks’ efficiency in investing their fund by dividing annualized net interest income to average earning asset — inched up to 4.18% in the fourth quarter from 4.04% in the same period a year earlier.

Provision for credit losses by these big banks reached P157.95 billion, up by 56.2% from P101.15 billion in December 2024.

“A softer gross domestic product (GDP) print heightened geopolitical tensions, and a declining interest rate environment weighed on bank stocks in [the fourth quarter of 2025],” Jarrod Leighton M. Tin, an equity research analyst at DragonFi Securities, Inc., said in a Viber message.

Mr. Tin said the weak economic growth cast doubt on whether banks can sustain double-digit loan growths this year, citing strong correlation between GDP and credit demand.

The Philippine economy grew by 3% in the fourth quarter, slower than the 5.3% growth in the same period in 2024 and the revised 3.9% in the third quarter. This brought full-year 2025 GDP to 4.4%, the weakest in five years.

Unicapital Securities, Inc. Research Head Wendy B. Estacio-Cruz said the slower economic growth weakened investor confidence in equities, especially bank stocks.

“The softer economic momentum likely tempered credit demand and weighed on corporate profitability, which are critical to banks’ earnings growth,” Ms. Estacio-Cruz said in an e-mail.

According to Kervin Laurence Sisayan, head of research at Maybank Securities Philippines, Inc., the slower GDP print signals a potentially “weaker loan growth for the financial industry.”

RATE CUTS

The BSP’s continued rate cuts also weighed on banks’ NIMs and profitability, analysts added.

“The decline in interest rate policy has reduced the funding cost of banks in general. On the flip side, it also puts downward pressure on earnings yield and overall put downward pressure on [NIMs],” Mr. Sisayan said.

Key policy rate stood at an over three-year low of 4.5% by the end of 2025. Meanwhile, inflation increased to 1.8% in December, but full-year average eased to 1.7% in 2025 — the slowest in nine years.

On Feb. 19, the Monetary Board lowered the target reverse repurchase rate by another 25 basis points (bps) to 4.25%. The BSP has reduced key interest rate by a total of 225 bps since it started its monetary policy easing in August 2024.

“While lower rates likely supported loan demand and borrowers’ repayment capacity amid low inflation, they also compressed net interest margins as asset yields repriced faster than funding costs,” Ms. Estacio-Cruz said.

She said this resulted in “tighter spreads and more cautious lending behavior.”

Linncon M. Lahip, equity analyst at Regina Capital Development Corp., said the stable inflation signaled a slower yet steady economic environment.

“However, despite the easing environment, loan growth is beginning to slow down and may signal that it has already reached its peak, signaling a more cautious phase for the sector,” he added.

Mr. Tin said banks have been “partially mitigating” pressure from lower rates by “shifting their loan mix toward higher-yielding consumer segments, supporting asset yields.”

He noted that with benign inflation and subpar GDP growth, the central bank may have room for further rate reductions to spur demand and bolster economic activity.

Chinabank Securities Corp. Research Associate Ralph Jonathan B. Fausto said that while rate cuts amid benign inflation supported credit demand and consumption, investors remained concerned on growth uncertainties and weak sentiment.

This weighed on loan demand prospects and banks’ profit outlook, he said.

Jash Matthew M. Baylon, equity analyst at The First Resources Management and Securities Corp., noted that flood control corruption scandal during the second half of 2025 resulted to weaker net foreign investments, affecting the financial sector’s operations and flows.

“The weaker business confidence and foreign direct investments also put pressure [on] our local currency to weaken, reaching the high at P59 per dollar,” he said.

Mr. Baylon said that given the pressure on banks’ NIM, the sector’s net interest rate profit may decline, leading to slower growth in earnings.

“But on the positive note, the lower rates could boost more spending and investments, which could translate to higher loan volume,” he added.

“Geopolitical developments further dampened overall investor sentiment, with risk-off flows pressuring the broader market, including the banking sector,” Mr. Tin said.

STANDOUTS

Despite headwinds, Mr. Baylon said banks’ performance “showed a modest recovery” in the fourth quarter compared to the July-to-September period, as holiday season remittances and consumer credit fueled spending.

According to Mr. Fausto, midsized banks like EW and PNB stood out during the quarter.

“EW benefited from resilient core lending income, supported by its established consumer portfolio despite increasing competition in the space. PNB saw its profitability bolstered by lower provisions, as the bank implemented its dynamic risk management strategy to improve asset quality and stabilize NPLs,” he said.

Meanwhile, Mr. Tin said the Bank of the Philippine Islands also stood out in the fourth quarter, citing resilient NIM amid low-interest rate environment.

“The continued repricing of the loan book toward higher-yielding consumer segments — where average yields exceed 12% — provides a structural buffer to net interest income should the BSP deliver further rate cuts,” he said.

For Mr. Lahip, banks that gained a larger share of consumer lending stood out as they benefited from higher-yielding retail products like credit cards and personal loans.

“In addition, we think that those banks who also saw support from growing fee-based revenues tied to increased card usage and transaction volumes also stood out while maintaining disciplined risk management and adequate provisioning, enabling them to preserve asset quality and sustain profitability despite the inherently higher risks associated with consumer lending,” Mr. Lahip added.

Ms. Estacio-Cruz said that banks with strong current account and savings account franchise and diversified income stream stood out during the quarter because they were “better positioned” to withstand the margin pressure from lower interest rates.

“Banks with solid consumer and MSME [micro, small, medium enterprise] loan exposure performed relatively well, supported by steady loan growth and resilient fee-based income from cards, bancassurance, and transaction banking,” she said.

“Some banks also benefited from treasury and trading gains amid market volatility, which helped offset pressure on core interest income,” she added.

OUTLOOK

Ms. Estacio-Cruz expects listed big banks to record growth in year-on-year earnings for the first quarter of 2026, supported by steady loan expansion, resilient consumer demand, and still-benign inflation.

“However, margin growth may remain constrained as the full impact of the 2025 rate cuts continues to filter through balance sheets, keeping net interest margins relatively tight,” she added.

For full-year 2026, Ms. Estacio-Cruz forecasts gradual improvement in banks’ performance “driven by stronger credit demand, potential margin stabilization if policy rates hold or eventually normalize, and continued growth in fee-based income.”

Mr. Lahip, on the other hand, expects banks to continue expanding to higher-yielding loans and fee-based income.

“At the same time, sustained investments in IT and digital infrastructure will remain crucial to enhance operational efficiency, strengthen risk management, and support long-term customer acquisition,” Mr. Lahip added.

Mr. Sisayan sees “slightly muted” loan growth for the first quarter of 2026, noting the slower economic growth in the fourth quarter.

“While double-digit loan and net income growth remain achievable, we would not be surprised to see expansion taper to the high single-digit range as normalization sets in,” Mr. Tin said.

According to Mr. Tin, investors should monitor upcoming GDP prints and policy rates.

“If 4% proves to be the BSP’s terminal rate, margin pressure may stabilize; however, further easing could drive additional NIM compression, particularly if banks are unable to recalibrate their asset mix and funding structure efficiently,” he added.

Apart from macroeconomic factors, First Resources’ Mr. Baylon said investors should also monitor geopolitical risks, updates on local corruption issues, and peso movement against the dollars.

Meanwhile, Chinabank’s Mr. Fausto said investors are likely to stay focused on loan growth, NIM resilience, and asset quality.

“The key question for investors is whether growth can be sustained despite prospects for lower NIMs and increasing credit costs,” he said.

")