The rise of revenge property investing in PHL

WE’VE HEARD of revenge spending and dining in 2022 and 2023 and how personal consumption expenditures helped sustain Philippine economic growth the past two years. Filipinos also did a lot of revenge travel in the past 24 months, resulting in a substantial increase in domestic tourists, local visitor receipts, average daily rates and hotel occupancies across the Philippines.

But what appears to be becoming mainstream now is revenge investing. And massive property investments are not just trickling in from the affluent market but also from the young and millennial workforce. In fact, some developers are actively targeting this young segment given their rising purchasing power and the potential of their disposable incomes to further surge in the years to come.

What’s also quite surprising is that these young buyers of residential units are acquiring properties not just for end-use but also as investments, banking on the properties’ live-work-play-shop features, proximity to public infrastructure, and the units’ attractiveness as possible sources of passive income once turned over.

UNDERSTANDING DEMAND OR LUXURY UNITS

While the millennial buyers help fuel the demand for affordable to lower mid-income residential units and have become a key segment to target for some developers, we cannot deny the fact that the demand for the upscale to luxury units remains strong, with take-up mainly coming from the affluent market.

Colliers has seen the upscale and luxury segments’ resilience even at the height of the pandemic in 2020 and 2021. Now that the property market is rebounding, especially the residential market, developers are lining up their luxury projects to tap demand from an affluent and discerning segment.

Over the past few years, local developers have aggressively partnered with foreign firms and we see more pronounced joint ventures (JV) with foreign property firms moving forward.

Take-up for upscale to luxury projects remains strong with demand focused on major business districts such as Fort Bonifacio, Makati CBD and Ortigas Center. Colliers believes that the luxury and ultra luxury segments will likely remain resilient amid the rising interest and mortgage rates. We attribute it to investors mainly banking on the capital appreciation potential of these upscale and luxury residential projects.

ROOM FOR PRICE ACCELERATION

Colliers sees the rising interest rates as among the headwinds in the residential market, especially their potential impact on mortgage rates.

Despite higher interest rates, Colliers has seen a stable demand for upscale to ultra luxury condominium projects in Metro Manila. Over the past few years, we have also recorded a healthy level of price increases for these residential projects.

Colliers Philippines believes that the increase in prices will only result in investors and end-users looking for greater amenities as well as innovative facilities.

Due to Metro Manila traffic, there will be greater demand for connectivity to master planned communities and topnotch concierge services. With more luxury and ultra luxury projects being launched in Metro Manila, Colliers Philippines sees the rise of more discerning buyers. Hence, developers need to further innovate and differentiate in a highly competitive luxury residential segment.

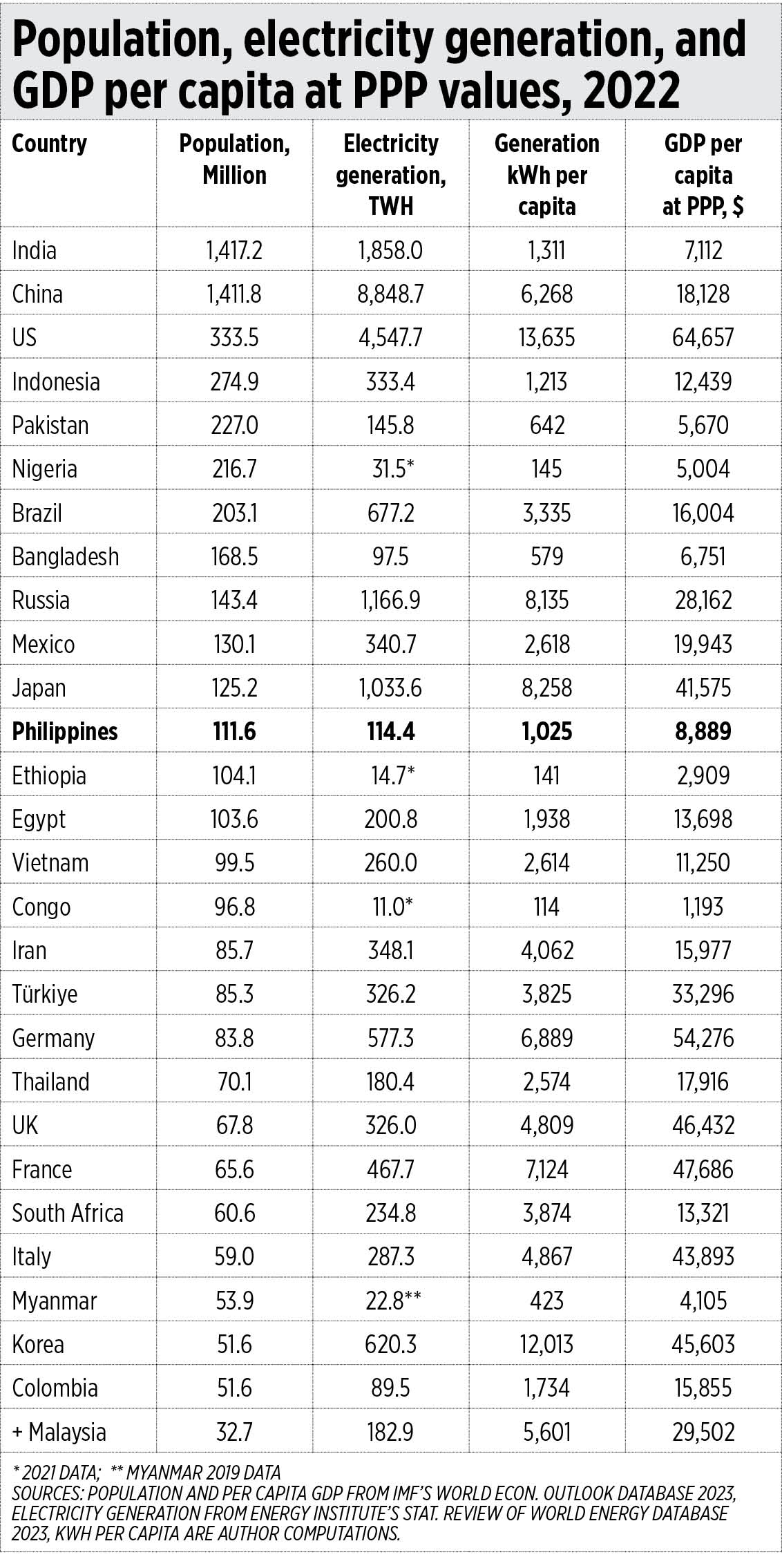

Based on regional prices, it appears that there is still room for further expansion of Metro Manila prices on a per square meter basis. What we can conclude based on this regional comparison is that the Philippines is barely scratching the surface. The price per square meter of Metro Manila’s most expensive condominium units is much cheaper compared to the most expensive ones in more affluent cities such as Hong Kong, Tokyo, and even Bangkok.

SUSTAINED GROWTH TO FUEL PROPERTY

Overall, we are optimistic with the Philippines’ strong macroeconomic fundamentals. The Philippine economy continues to expand despite soaring commodity prices and global geopolitical headwinds. The country remains one of the fastest-growing economies in Asia, primarily backed by resilient personal consumption and private investments.

Sustained recovery is likely to benefit major economic sectors including property development. The luxury and ultra luxury condominium segments showed resilience during the pandemic. Hence, it won’t be startling to see these developments proliferating in the near to medium term as the Philippines recovers from the pandemic.

The luxury and ultra luxury projects are also likely to benefit from the reopening of Philippine tourism and the return of foreign employees. Affluent investors are likely to continue buying luxury units as they upgrade, bank on potential price appreciation, and look for a viable hedge against inflation.

CASHING IN ON PROPERTY’S VIABILITY AS AN INVESTMENT OPTION

Revenge property investing is likely to persist, especially for the Philippines where investors do not have several options to choose from. Colliers sees young buyers and the affluent investors continuously looking for residential units that have strong rental prospects and potential for price appreciation.

Colliers Philippines believes that developers should highlight their projects’ attractiveness for lease or potential for capital value growth, whether targeting local buyers or foreign investors.

With tempered launches and availability of substantial number of ready for occupancy (RFO) units in Metro Manila, we expect aggressive marketing initiatives from property firms over the next 12 months. Developers should also curate promotions and offerings based on their target markets, whether overseas Filipino workers (OFW), young local investors, or the experienced and affluent buyers.

Joey Roi Bondoc is the research director for Colliers Philippines.