Taxwise Or Otherwise

By Elyse O. Lui

With steadily increasing COVID-19 cases, major cities on lockdown, and most businesses closed, the government has appealed to the private sector to contribute to relief efforts in the spirit of bayanihan. The Bureau of Internal Revenue (BIR) released Revenue Regulations (RR) No. 9-2020 in line with Republic Act No. 11469, otherwise known as the Bayanihan to Heal as One Act, the main objective of which is to adopt urgently-needed measures to address the novel coronavirus outbreak. In particular, RR No. 9-2020 liberalizes the grant of incentives for certain donations in response to the COVID-19 crisis.

The Tax Code grants donor’s tax exemptions and full/partial income tax deductibility for qualified donations made to the national government for NEDA-approved projects, and to accredited non-stock, non-profit organizations (NSNP) formed and operated exclusively for social welfare and charitable purposes, among other purposes.

RR No. 9-2020 broadens the coverage further by granting full deductibility for COVID-19 related donations given to the national government during this state of emergency, even if not included in NEDA’s annual priority plan. More importantly, the RR allows donors to donate directly to other donees and still avail of donor’s tax exemption and full deductibility. These additional donees are: private hospitals, NSNPs (even if non-accredited); and entities which serve as conduits in the relief activities of accredited NGOs, and/or the national government.

The tax incentives under the RR cover donations for the sole purpose of combating COVID-19, given from March 16, the start of the Luzon-wide enhanced community quarantine (ECQ), until the end of the three-month effectivity period of the Bayanihan Act. The donations mentioned in the RR are not only limited to cash, but also include health care equipment or supplies, relief goods, and the use of personal and real property.

For donations in kind, the input VAT attributable to the purchase of goods may be creditable against the donor’s output VAT. Needless to say, such input VAT credits must be supported with official receipts or sales invoices. Such donations will not be treated as transactions deemed sales subject to VAT.

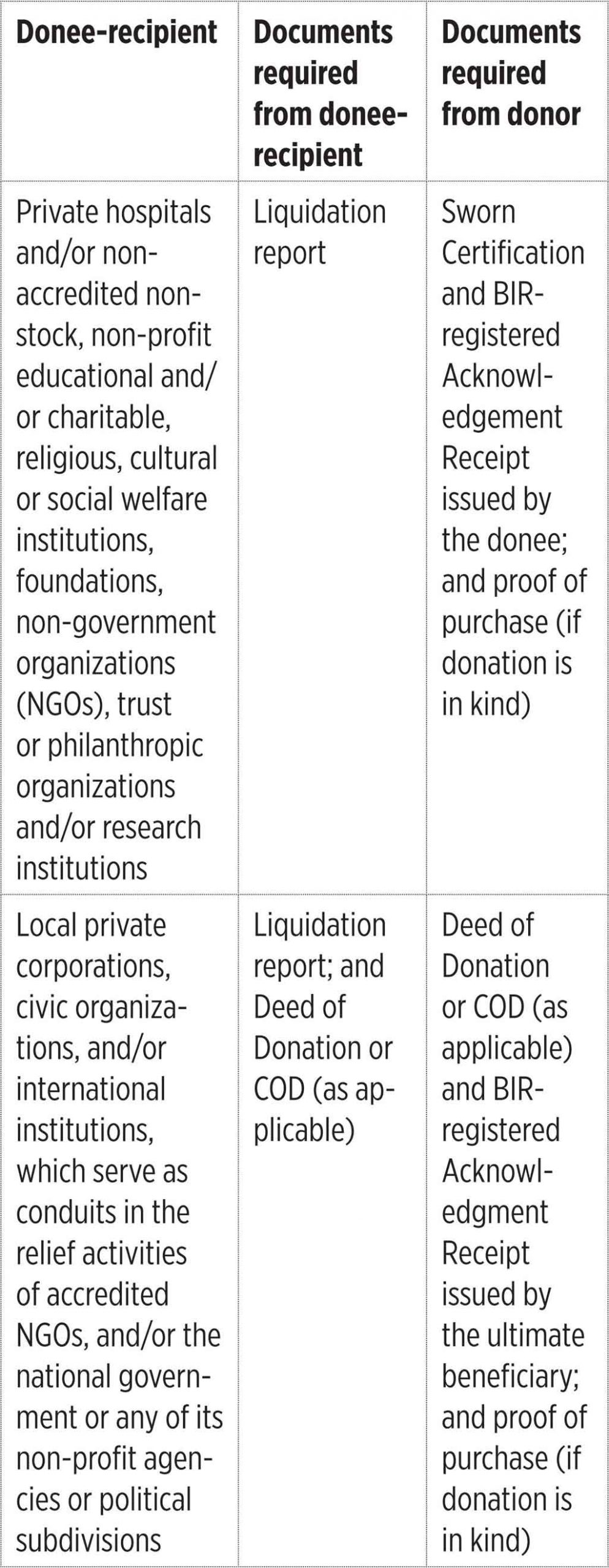

DOCUMENTARY SUPPORT FOR TAX-EXEMPT DONATIONS

The availment of the tax incentives is subject to the timely submission of the following required supporting documents by both the donor and donee:

As RR 9-2020 did not provide for a specific timeline, it appears that the COD must be filed by the donee with the BIR following the deadlines in other existing regulations. Normally, the COD must be filled within thirty days (30) from the receipt of the donation. Pursuant to RR No. 10-2020, the filing of the COD is extended for thirty (30) days from the lifting of the ECQ.

The donor’s obligation to file a Notice of Donation has been waived by the BIR during this period.

The above documents must be submitted by both parties within 60 days from the lifting of the ECQ to their registered Revenue District Offices.

Despite the seemingly stringent requirements, the RR leaves ample room for flexibility. For one, if the donee does not have any BIR-registered Acknowledgement Receipt, it may use the template for an acknowledgment receipt provided under the RR.

Also, the Sworn Certification may be executed by the donor, instead of the donee.

To curtail possible abuse, the BIR reiterated its right under the Tax Code to audit the exemption and deductibility of the donations by checking the documents submitted by the donor and donee.

While RR No. 9-2020 is a timely perk to taxpayers who want to join the fight against COVID-19, there is room to enhance the guidelines by clarifying a few points:

• In prescribing the documentary requirements for donations to the additional donees under Section 4, the RR appears to have erroneously included accredited NSNPs in the list. The supporting requirements on donations to accredited NSNPs are already separately discussed in Section 3 of the RR.

• The RR did not provide guidance on how the donor should determine the value of the deductible expense related to the use of his property (such as vehicles, lots, or buildings) and how this should be taken up in the liquidation report, Sworn Certification and BIR-registered Acknowledgment Receipt.

• It is not clear whether the input VAT incentive on donations in kind is also applicable to those made to the additional donees since the RR referred only to donations enumerated in Section 3.

• For donations coursed through another entity, it is not clear if the liquidation report must be filed by the donee-recipient or the ultimate beneficiary.

• It might be good if the RR can further clarify which donations may be classified as relief goods entitled to the incentives. For example, would items such as shampoo, toothpaste (or even deodorant) qualify? If not allowed, then such items may qualify for tax incentives only if donated to the National Government or accredited NSNPs.

Despite these inconsistencies which I hope will be clarified subsequently, the RR is still a welcome development to taxpayers who have aligned their resources with their values during these times. With these tax perks, hopefully more taxpayers will be encouraged to participate in social welfare initiatives.

The views or opinions expressed in this article are solely those of the author and do not necessarily represent those of Isla Lipana & Co. The content is for general information purposes only and should not be used as a substitute for specific advice.

Elyse O, Lui is a senior associate with the Tax Services Group of Isla Lipana & Co., the Philippine member firm of the PwC network.

(02) 8 845-27 28