THE GOVERNMENT made a partial award of the Treasury bills it offered on Monday. — BW FILE PHOTO

THE GOVERNMENT partially awarded the Treasury bills (T-bills) it offered on Monday at lower rates as investors flocked to shorter tenors on expectations of more hikes from the Bangko Sentral ng Pilipinas (BSP) and the US Federal Reserve.

The Bureau of the Treasury (BTr) awarded just P10 billion in T-bills at its auction on Monday even as total tenders reached P42.88 billion, nearly thrice as much as the P15 billion on offer.

The Treasury made full awards of the shorter 91- and 182-day tenors and rejected all bids for the one-year T-bill as investors wanted higher returns in exchange for keeping their money locked up for a longer duration.

Broken down, the government fully awarded the 91-day T-bills, raising P5 billion as programmed as tenders for the tenor reached P22.34 billion. The average yield of the three-month debt papers was at 1.46%, 21.5 basis points (bps) lower than the 1.675% seen at last week’s auction.

The BTr also raised P5 billion as programmed from the 182-day securities as bids for the tenor reached P14.96 billion. The average rate on the six-month T-bill was at 1.812%, down by 8 bps from the 1.892% fetched at the previous auction, where the government made a partial award of the tenor.

The 91- and 182-day tenors fetched yields of 1.4533% and 1.7681% at the secondary market before Monday’s auction.

Lastly, the Treasury rejected all bids for its P5-billion offer of one-year T-bills even as bids reached P5.58 billion. Had the government made a full award, the average rate of the one-year tenor would have been at 2.716%, 67.59 bps higher than the 2.0401% fetched at the secondary market prior to the auction, based on the PHP Bloomberg Valuation Reference Rates published on the Philippine Dealing System’s website.

National Treasurer Rosalia V. de Leon said in a Viber message to reporters that the BTr made a full award of the 91- and 182-day tenors as they were over twice oversubscribed and fetched lower rates.

Ms. De Leon said they rejected all bids for the 364-day securities due to “tepid demand and unacceptable rates” as the market priced in expectations of hikes by the BSP and the Fed in their bids for the longest T-bill tenor on offer.

The first trader likewise said demand for the one-year T-bill was weak amid rate hike fears.

“Despite the prospects of higher policy rates in June, yields for the 91- and 181-day [T-bills] eased. I think most investors continued to be on wait-and-see and just prefer to park cash in short-term investments while waiting for firm leads,” the second trader said.

The BSP is likely to raise key interest rates by another 25 bps at its next policy review on June 23, its chief said last week.

“We are probably inclined to have another 25-basis-point adjustment on our next Monetary Board meeting which is on June 23,” BSP Governor Benjamin E. Diokno said.

The BSP raised benchmark interest rates by 25 bps on May 19, marking its first hike since November 2018, as it tries to temper rising inflationary pressures.

The Monetary Board increased the key policy rate by 25 bps to 2.25%. Interest rates on the overnight deposit and lending facilities were also hiked by 25 bps to 1.75% and 2.75%, respectively.

At that meeting, the central bank upwardly revised its average inflation forecast for 2022 to 4.6% from the previous forecast of 4.3%, exceeding the 2-4% target band. For 2023, the BSP’s inflation forecast was hiked to 3.9% from 3.6% previously.

Inflation climbed to 4.9% in April, the highest in more than three years.

Meanwhile, all participants of the Fed’s May 3-4 policy meeting backed a half-percentage-point rate increase to combat inflation that they agreed had become a key threat to the economy’s performance and was at risk of racing higher without action by the central bank, Reuters reported.

This month’s 50-basis-point hike in the Fed’s benchmark overnight interest rate was the first of that size in more than 20 years and “most participants” judged that further hikes of that magnitude would “likely be appropriate” at the Fed’s policy meetings in June and July, according to the minutes released last week.

The BTr wants to raise P250 billion from the domestic market in June, or P75 billion through T-bills and P175 billion from Treasury bonds.

The government borrows from local and external sources to help plug a budget deficit capped at 7.7% of gross domestic product this year. — T.J. Tomas with Reuters

In recognizing the part of the banking industry to pursue sustainable financing or green financing in the country, the Bangko Sentral ng Pilipinas (BSP) has released the Philippine Sustainable Finance Roadmap and Sustainable Finance Guiding Principles to serve as the foundation in promoting successful strategies in implementing sustainable finance in the country.

Banks were all encouraged to study and apply all the guidelines written in the roadmap to improve the banks’ process in adopting sustainable finance in their investment activities that will not only give sustainability-positive outcomes and investible returns but also environmental safety and considerations.

The roadmap, launched in October last year, formed a comprehensive approach that will serve as the foundation for effective strategies to facilitate the mainstreaming of sustainable finance in the country. Meanwhile the guiding principles establishes a common understanding among various stakeholders of the economic activities considered “sustainable.”

BANKS ROLE ON SUSTAINABLE FINANCING According to the International Capital Market Association, sustainable finance “incorporates climate, green, and social finance while also adding wider considerations concerning the longer-term economic sustainability of the organizations that are funded, as well as the role and stability of the overall financial system in which they operate.”

Sustainable finance has been implemented across the financial system due to its economic benefits with the environment. Some banks have already invested even before the roadmap was released several years ahead.

Rizal Commercial Banking Corp. (RCBC) believes that good sustainable practices are a key pillar of responsible lending which impacts on the environment and communities. RCBC’s Sustainability Report is in response to the BSP’s call for financial institutions to be enablers of environmentally and socially responsible business decisions.

“RCBC is a pioneer in sustainable financing. Its environmental and social management system (ESMS) and its own Sustainable Finance Framework are aligned with the strategic pillars of the sustainable financing Roadmap and Guiding Principles,” the bank said in an e-mail.

The lender said it has implemented its ESMS since 2011, several years ahead of the central bank’s issuance for the banks to incorporate sustainability principles into their operations. It developed its own sustainable finance framework in 2019.

RCBC issued the first Peso Green and Sustainability bonds under the Association of Southeast Asian Nations (ASEAN) Sustainability Framework and the first US Dollar Sustainability bond by a Philippines corporate or bank issuer. This year, RCBC was the first bank in the Philippines to offer a Peso Green Time Deposit. All of these products offer market rates of interest. Proceeds are allocated to refinancing of the Bank’s green and social asset portfolio, thus guaranteeing investors of environmentally and socially positive outcomes.

“Since the implementation of RCBC’s Sustainable Finance Framework in 2019, RCBC has issued $1.4 billion in sustainable financing instruments, which attracted strong demand from investors all over the world. The P17.87 billion issuance in March 2021 was the only peso-denominated sustainability bond to be issued in the country in 2021 and the largest bond issuance in RCBC’s 61-year banking history,” added RCBC.

According to RCBC, these sustainable investments are offered to companies or individuals who are looking to place their funds into assets that help protect the environment with socially positive outcomes, and the economic impact or pricing was never the motivation for the issuance of these sustainable financing instruments.

“Although, it has been recently observed that there is a small pricing benefit particularly in offshore markets — this is the result of investors wanting to increase the share of these assets in their portfolios and funds dedicated solely to sustainable assets,” RCBC said.

Meanwhile, Maybank Philippines, Inc. (MPI) is poised and has adopted sustainable financing, being part of the Bank’s environmental social and governance (ESG) framework in their business agenda.

“MPI is leveraging on the roadmap and activities of our parent bank and its sustainability office, being the forerunner in sustainable finance/ESG in the region.

It has made the following sustainability commitments:

a.) Mobilization of 50 billion Malaysian ringgit (MYR or about $1.14 billion) in sustainable finance by 2025;

b.) Improving and the lives of one million households across ASEAN by 2025;

c.) Achieving a carbon neutral position for scope 1 and 2 emissions by 2030 and net zero carbon equivalent position by 2050; and

d.) Achieve one million hours per annum on sustainability & delivering one thousand significant sustainable development goals (SDG)-related outcomes by 2025.

“Maybank Group’s focus is to integrate ESG principles into the prevailing risk management strategies as well as to bring impact to all stakeholders, internal and external,” MPI Chief Risk Officer Rajagopal Ramasamy said in an e-mail.

Mr. Ramasamy said that there seems to be lack of awareness on the benefits of sustainable products, though this is viewed as not of higher risk compared to other financial instruments.

“This misperception may result in negative outcome amongst investors on green financing. Educating stakeholders on benefits of ESG/sustainable financing is crucial, thus MPI has outlined, conducted and committed to various learning and client engagement initiatives to support our sustainability agenda,” Mr. Ramasamy said.

Mr. Ramasamy said that sustainability shall be embedded in business process for positive economic impact. He added that there are larger market opportunity for sustainable financing, and various elements could be incorporated to offer attractive sustainable financing solutions. Markets that are already into sustainable businesses with embodied ESG principles and players in transition towards sustainable businesses can be the target.

“Rate of return remains to be a primary objective of any investors. Hence, it is important for lenders to demonstrate to the investors the advantage in such instruments towards environment, ecosystem, and community without diminishing monetary returns,” Mr. Ramasamy said.

FURTHER DEVELOPMENT Banks plan to develop or further its involvement in green financing and develop specific strategies of action for this segment this year or in the future.

RCBC intends to provide further support for renewable energy (RE) by tapping 12 RE projects, with a combined capacity of 1.6 gigawatts (GW) in the next two years. This goal supports its public commitment to cease funding for the construction of new coal power plants (since December 2020) and gradually taper off its P42 billion coal exposure until full maturity in 2031. Since 2012, the Bank has supported around 3 GW of RE projects.

MPI will provide funding to RE-related activities and projects while reducing exposures to non-renewable energy investments such as coal-fired power plants.

MPI will also finance related businesses in the value chain financing promoting ESG. Help counter rapid global warming by supporting activities leading to net-zero carbon emissions.

According to MPI, the Maybank Group has achieved 13.6 billion Malaysia ringgit in sustainable financing to date, with 6.1 billion Malaysia ringgit worth of green buildings accounting for the largest segment. It has played a role in the world’s first Islamic Green Financing in Singapore and in the first Malaysian Sustainability Sukuk.

“Maybank Philippines plans to play similar role in the Philippines for in the area of green financing, both at corporate and retail markets,” Mr. Ramasamy said. — Lourdes O. Pilar

SEMIRARA Mining and Power Corp. (SMPC) has remitted P5.9 billion in government royalty to the Department of Energy, which the listed energy company described as “the highest in its corporate history.”

“We had an exceptionally strong start, so much so that in three months, we surpassed our previous full-year royalty payments,” said SMPC President and Chief Operating Officer Maria Cristina C. Gotianun in a statement on Monday.

The record amount, which is nearly nine times more than the P656 million a year ago, comes as the company registered all-time-high coal shipments and average selling prices.

Of the P5.9 billion remitted to the Energy department as the government share, more than P3.5 billion will be retained by the national government.

The rest of the amount will go to the host local government units of SMPC’s mine site. Antique province will receive P476 million while Caluya town and Brgy. Semirara will receive around P1.1 billion and P833 million, respectively.

Local government units are entitled to a 40% share of royalty proceeds from petroleum, coal, geothermal, hydrothermal and wind resources, as called for by the Local Government Code of 1991.

Last year, SMPC said it paid a total of P5.4 billion to department “as improved coal output and favorable market conditions allowed the company to ship more coal at elevated prices.”

SMPC, the country’s largest coal producer, describes itself as the only vertically integrated power generator in the country that produces its own fuel. It supplies coal to local power plants, cement factories and other industrial facilities.

On Monday, shares in the company rose 1.36% or 45 centavos to close at P33.50 apiece.

CCP screens classic films Macho Dancer, Manila By Night for free

LOOK back at the socio-political landscape of the 1980s Manila through the Cultural Center of the Philippines (CCP) Arthouse Cinema’s back-to-back screenings of National Artist for Film Lino Brocka’s Macho Dancer and National Artist for Film Ishmael Bernal’s Manila By Night on June 3, starting at 2 p.m., at the Tanghalang Manuel Conde. Macho Dancer follows the story of a handsome teenager from the mountains who journeys to Manila in an effort to support his family after he was abandoned by his American lover. With a popular call boy as his mentor, Paul enters the glittering world of the macho dancer. Mr. Brocka captured a world of male strippers, prostitution, drugs, sexual slavery, police corruption and murder in this classic film. In Manila By Night, the hidden nightlife of ordinary people living in Manila is unveiled. Lovers and families’ conflicts are radically pitted against each other as they live in the night streets rampant with drugs and prostitution. The outstanding narrative explicitly unravels the various characters and episodes. This landmark film by Ishmael Bernal depicts the darkness of city life so vividly that it was once prohibited to use the word “Manila” on its title. To watch the films, pre-register through this link: https://bit.ly/38RCR03. The film screenings celebrate the National Heritage Month, and commemorate Mr. Bernal’s death anniversary on June 2.

GMA premieres sports-oriented seriesBolera

GMA ENTERTAINMENT Group sets out to prove that women can rise to the top and become champions with hard work, skill, and talent in its newest primetime series, Bolera. Directed by Dominic Zapata and Jorron Lee Monroy, the story follows Joni (Kylie Padilla), a billiard prodigy who was taught to play by her father, a former billiard champion. But when her father dies, it is up to her to support her family, and playing billiards is suddenly the last thing on her mind. Joining Padilla in the series are Rayver Cruz, Jak Roberto, Gardo Versoza, Joey Marquez, Al Tantay, and Jaclyn Jose. Bolera airs on weeknights at 8:50 p.m. after First Lady on GMA Telebabad.

Tate McRae releases debut album

SINGER, songwriter, and dancer Tate McRae has released her debut album, i used to think i could fly ,via RCA Records/Sony Music. The album features writing collaborators and producers like Greg Kurstin, Finneas, Charlie Puth, Alexander 23, Blake Slatkin, Louis Bell and more. The album includes the already released tracks “feel like shit,” “she’s all i wanna be,” “chaotic,” “what would you do?” and more. Ms. McRae’s latest single, “she’s all i wanna be,” has over 230 million streams and is currently in the Top 12 on the Top 40 chart. Ms. McRae just wrapped her 2022 North American Tour and is currently performing in the European Union with dates in the UK and Australia later this summer. Starting in September, she will tour as the special guest on Shawn Mendes’ Wonder: The World Tour 2022. The new album is available on all digital music platforms.

EJ DE Perio releases first single

FILIPINO singer-songwriter EJ De Perio defies the concept of perpetuity on “Panandalian,” his first official single under Sony Music Philippines. Featuring laid-back acoustic guitars and minimal instrumentation, the ballad asserts his sentiment that despite the uncertainty of the future, there will always be one person who is willing to stick with you through thick and thin. “I wrote ‘Panandalian’ out of the realization that nothing’s gonna last forever, and everything must come to an end,” Mr. De Perio said in a statement. “The song is about preparing yourself for the inevitable change, and making sure to protect that one person who is willing to keep things the same way — even if everything around you is constantly evolving.” The stripped-down track is produced by fellow singer-songwriter Migz Haleco.“Panandalian” is available on all digital music platforms worldwide.

Kangdaniel releases new album

K-POP ICON KANGDANIEL marks a return to music-making with the release of his new full-length album, The Story. Featuring 10 songs co-written by the Korean pop singer, the record chronicles stories from his own perspectives and experiences. “I want to tell the stories as a storyteller,” the South Korean artist said in a statement. “I would be grateful if you just enjoy and feel relaxed with The Story. I hope you like it.” The Story is his first full-length album, and follows the release of his chart-topping EP, Yellow, which is certified platinum in South Korea. KANGDANIEL’s new album also includes collaborations with some of the biggest names in K-Pop: Korean-American singer/rapper Jessi on “Don’t Tell,” sokodomo on “How We Love,” and Dbo on “Loser.”The Storyis available on all digital music platforms worldwide.

MORE FILIPINOS became part of the financial system through basic deposit accounts (BDAs) as of December last year, according to the Bangko Sentral ng Pilipinas (BSP).

Data from the central bank showed BDAs rose by 19% to 7.9 million in the last quarter of 2021 from 6.6 million in the same period a year earlier.

The total value of BDA deposits also increased by 7.6% to P5.1 billion as of end-December 2021 from the P4.7 billion seen a year prior.

“The BDA was created to meet the needs of the unbanked and low-income sector and foster greater financial inclusion,” the BSP said in a press release on Monday.

“Since ownership of an account is an important first step to perform digital payments, BDAs support BSP’s mutually reinforcing goals of financial inclusion and payments digitalization,” the central bank added.

Basic deposit accounts are being offered by 138 banks to date.

The BDA framework was introduced by the central bank in 2018 to encourage more Filipinos to become part of the financial system.

This type of account has a low opening amount capped at P100, no maintaining balance requirement, no dormancy charges, and simple identification requirements.

The lack of valid identification, which hinders account opening, is being addressed by the ongoing registration for national IDs.

Lenders offering BDAs can customize their deposit products by using technological innovations for client application and services.

Based on the 2019 Financial Inclusion Survey, only 29% of adult Filipinos are part of the banked population, leaving some 51.2 million individuals unbanked.

The BSP wants 70% of Filipino adults to have accounts in financial institutions by 2023. — K.B. Ta-asan

IN THE GROWING SPACE of financial technology (fintech), the proliferation of the Buy Now Pay Later (BNPL) system made its way in the Philippines. The coronavirus disease 2019 (pandemic) accelerated the process of shifting Filipino consumers to digital payment and resulted to its pervasive adoption, particularly in the e-commerce industry.

For those who do not own credit or debit cards, BNPL allows consumers to purchase and pay for them in several installments.

According to the Q4 2021 BNPL Survey by ResearchAndMarkets.com, the Philippines’ BNPL payment is seen to grow by 109.7% year on year to $803.5 million this year. BNPL payment adoption is expected to climb steadily between 2022 and 2028 with a compound annual growth rate of 50.9%.

GEORG STEIGER, chief executive officer and co-founder of First Digital Finance Corp.

One such provider in the country is BillEase. Launched in 2017, it is operated by fintech company First Digital Finance Corp. (FDFC), a wholly owned subsidiary of Singapore-headquartered Jin Chan Invest Pte. Ltd. It also operates Balikbayad, a loan app targeting overseas Filipino workers.

BillEase provides a range of in-app services like low-cost cash loans, e-Wallet top-ups, mobile loads, and gaming credits.

FDFC’s revenue more than doubled to P370.41 million last year from P148.83 million in 2020 as interest income from loans jumped during the period. It also earns from loan processing fees and penalties.

Its bottom line, meanwhile, swung to profit last year to P22.57 million a year ago from P23.82 million net loss previously.

Its lending surged last year as loans receivables amounted P667.17 million, 2.6 times more than P258.59 million previously.

BillEase has so far secured $31 million in various funding rounds this year, which will be used to expand its services.

In a statement, FDFC said that the facility is “a further validation of FDFC’s business and the platform their team has built over the past few years and helps to firmly position BillEase as the leading BNPL brand in the Philippines.”

To know more about BillEase, BusinessWorld reached out to Georg Steiger, chief executive officer and co-founder of FDFC, through an e-mail interview. Here is the excerpt:

What is BillEase? Some may not yet be familiar with this BNPL platform and given this, how will you introduce BillEase, which is under FDFC and the leading BNPL brand in the country?

Mr. Steiger: BillEase is a buy now, pay later plus (BNPL+) app. We allow consumers to purchase products and services online and offline through flexible installment plans even without signing up to a credit card or debit card. What makes us different is that customers are not required to top up their account for them to use BillEase as a payment method as we provide instant credit they can use. Unlike other players, we’re not a pure play BNPL. We provide other financial services hence BNPL+. Right now, we offer in-app services such as low-cost cash loans, e-wallet top ups, prepaid, and gaming credits.

What services does BillEase provide or cater to?

Mr. Steiger: We’re catering to mostly millennials and Gen Z cohorts as there is a general trend to move away from credit cards and we see this in other more developed countries. With credit cards, sometimes consumers are tempted to run up a balance and just keep paying interest.

The difference with BillEase is that from the start you already know your monthly payments. So especially if you are new to credit, this is an approach that instills more discipline, and we think is a good way to get started. Our installment plans can range from 3-12 months and due dates are aligned with the customer’s pay days — it’s designed to be a shorter commitment and less of a burden than personal loans offered by banks.

What makes BillEase different from other BNPL providers?

Mr. Steiger: Among the major differentiators of BillEase is our ability to price our products competitively. This is due to our proprietary credit decision technology (machine learning) which we developed over time. We have a strong understanding of customers from the get-go and provide rates that are competitive.

Additionally, for merchant partners, we provide not a one-size-fits-all solution as we provide customizable payment plants. For example, if you’re a grocery or food delivery platform (F&B category) instead of installment payments, we can offer Pay Later which allows you to offer a small credit line that customers can use to pay in 10-20 days or next payday. If you’re an electronics merchant, we can also offer longer financing terms.

Essentially, we can have an adaptive checkout page for retailers and offer the right payment plan for their customers. We’re also the only BNPL with more than five payment gateway partners, which means retailers can easily add our solution on their checkout pages via Dragonpay, Xendit, Paynamics, 2C2P, and Bux.

How would you describe the BNPL services in the current landscape of the Philippines?

Mr. Steiger: The BNPL is the fastest growing space in fintech and more customers are opting to use BNPL when buying online and offline due to its fast and easy UX (user experience)/Sign Up process vs. legacy platforms like credit card or traditional point-of-sale (POS) financing methods. In the Philippines, BNPL is still a nascent industry although the installment concept or “hulugan” has been here for quite some time now.

Were the BNPL platforms already popular in the pre-pandemic era? What propelled them to become prevalent in the country?

Mr. Steiger: Yes, the BNPL industry was on track to become the fastest growing industry and a lot of e-commerce businesses and retailers took notice of its importance in selling and acquiring customers, hence, it became one of the most potent sales optimization tools for many merchants pre-pandemic.

In the first quarter of 2020 and the following months, more businesses realized the importance of BNPL for consumers as the pandemic bites the customers’ income. The pandemic pretty much propelled the growth of the industry five times, and it continues to be on demand post-pandemic era.

How will you describe the progress of these services?

Mr. Steiger: Most providers almost offer the same services with different target niche market and/or pricing models and this is particularly good for the customers. Some other banks/legacy players are also offering this through their credit card products and on the alternative lending space you have Atome, Tendopay, and Home Credit. Most of these alternative players have specific niche target markets.

BillEase has recently secured $20 million through a funding round to expand its BNPL platforms in the country and this was granted by Lendable, an emerging market credit facility. How will you use these funds — bringing the total to $31 million — raised?

Mr. Steiger: Our partnership with Lendable would enable us to further drive our mission to financial inclusion that provides more alternative financial services to Filipino consumers, particularly the younger generation and move people from informal to formal financial sector. The facility granted allows us to expand our loan portfolio which means extended opportunity to provide credit to more customers.

What are BillEase’s upcoming projects that may drive innovation and/or help consumers?

Mr. Steiger: We’re constantly looking for ways to innovate and can’t provide much detail. However, one thing we’re particularly excited about is the launch of our in-store QR (quick response) payment solution. Point-of-sale financing has been traditionally manual e.g., customers have to talk to a financing personnel in stores to apply for a loan. But with our in-store QR payment, customers can easily scan the code, install our app, sign up in less than five minutes, and proceed with the payment of goods and services they’re availing at brick-and-mortar stores. This, we believe will contribute to the goal of Bangko Sentral ng Pilipinas (BSP) to promote more cashless payments both online and offline.

How does this platform meet the needs of its consumers?

Mr. Steiger: BillEase fulfills the financing needs of the young and upwardly mobile individuals. Our customers are mostly digital natives, often between 25- to 35-year-olds, recent college graduates, early in their career. Given the tedious and strict standards for credit card applications, most of our customers will probably not be interested or qualify, but still want the flexibility to split the purchases into more accommodating monthly installments.

What are the advantages or benefits of this BNPL platform?

Mr. Steiger: BillEase is supportive towards a greater financial inclusion and the formal credit system. All BillEase customers have a credit record in both government and private credit bureau. So far, we think we are the only online platform that supports both government and private credit bureaus. Therefore, with time, and given a good credit record, our customers will be able to more easily access the formal credit system, for example for when they want to buy a car, or maybe get a mortgage for a house, with a positive credit record, the banks will naturally be more accommodating to their applications.

What are the pitfalls or disadvantages of BNPL?

Mr. Steiger: There are some advantages of using BNPLs in general, for example consumers spending impulsively, late payments fees, and minimal credit checks — for some providers which could affect the customers in many ways instead of getting the benefits of the financial product.

From our end, we’re making sure that these are pretty much handled properly. That’s why we always allow customers to choose the installment plan they want and make sure that they’re always on top of their repayments and we manage total exposure based on the customers capability to repay.

With the pervasive use of online shopping or purchases, what regulations can be employed to prevent consumer overspending?

Mr. Steiger: The regulations are fairly placed. If you look at the financing landscape in the past two years, there have been a lot of improvements. The Securities and Exchange Commission (SEC), in particular, has been proactively going after unscrupulous players. When it comes to the pitfalls of consumer overspending, we think that an installment product like BillEase where the consumer always has a clear schedule to pay off a purchase compares favorably with credit cards where many consumers run up a balance and then just keep making the minimum payment.

We believe that having a clear timeline to repay is a much better product, especially for customers who are new to credit. Most of our installments are also relatively short term so it does not create a long-term burden for customers.

What are the notable accomplishments that BillEase has done?

Mr. Steiger: Earlier this year, we reached over 1.5 million+ users and/or app downloads and we plan to triple this in the next one to two years as we continue to roll out new products and partnerships. On strategic partnerships, we’ve been able to work with top retailers in the country and five major payment processors, which pretty much put us ahead and allows us to become as ubiquitous as possible for consumers and retailers.

What can consumers expect in the BNPL services in the country? In BillEase, particularly?

Mr. Steiger: If you look at the consumer finance space in the Philippines, this is still a seriously supply-constrained segment. With a consumer lending over a GDP (gross domestic product) ratio of 4.3% (vs., for example, Indonesia with 10%) there is still a lot of pent-up demand — if you can develop the right products to serve this market. For BillEase, customers and merchants can expect more and more product offerings in the coming months.

Anything else you would like to share with us?

Mr. Steiger: So far, we have received very positive feedback from both customers and merchants. Our Play/App Store ratings are currently 4.8/5.0 — one of the highest in the Finance Category. We feel that this is just the start, as we gain momentum, and the increased level of general acceptance towards dealing with online financial solution providers and BNPLs in the Philippines, we are very excited with the potential future developments yet to come from BillEase. Customers see it as a convenient, and safe way to transact online, while also establishing a formal credit record.

Because BillEase was the first online Buy Now Pay Later (BNPL) in the market, there is always a natural hesitation at the beginning for fear of the unknown or even potentially fraud. However, as people get more comfortable dealing with online transactions, and with our ever-increasing footprint and visibility, we feel more customers would feel safe and confident in transacting with BillEase. Merchants are happy that their customers can buy what they want and pay for it in a more convenient manner. Our merchant partners have grown close to 1,000 merchants — including some of the country’s biggest names – and we foresee this growth to continue. Our recent partnership with Philippine Airlines and Giordano, KitchenAid, BAYO, Power Mac Center for in-store POS financing are recent examples of our ever-expanding merchant partners. — Abigail Marie P. Yraola

Visit First Digital Finance Corp. website at https://www.firstdigitalfinance.com/ and BillEase at https://billease.ph/ to know more about them.

THE Energy Regulatory Commission (ERC) has granted temporary approval to a power supply agreement (PSA) between an energy provider in Occidental Mindoro and an electric cooperative in the same province.

In a statement on Monday, ERC Chairperson and Chief Executive Agnes VST Devanadera said the grant of provisional authority to the supply deal “will greatly help alleviate the power shortage within its franchise area.”

The PSA was forged between Occidental Mindoro Electric Cooperative, Inc. and Occidental Mindoro Consolidated Power Corp. for Mamburao, Paluan, Sta. Cruz, and Abra de Ilog (OMCPC-MAPSA). It will allow the parties to implement an additional power supply of about 7 megawatts (MW).

Occidental Mindoro has a power demand of around 27 MW, but only 20 MW is provided by OMCPC’s bunker-fired diesel power plant in San Jose, located in the southern part of the province, the ERC said. OMCPC is said to be the lone supplier in the area.

As a result, the province has been experiencing rotational power outages of as much as five to six hours per day due to a significant shortage in the available power supply.

The electric cooperative was previously able to source 4 MW of power from a diesel power plant of the National Power Corp. in Mamburao, which is in the northern part of the province. But its supply contract with the state-owned entity expired in December last year, the ERC said, adding that the power plant is no longer available.

“The additional power supply to be sourced from OMCPC-MAPSA will be able to cover the power requirements, particularly in the areas of Mamburao, Paluan, Sta. Cruz, and Abra de Ilog in the Province of Occidental Mindoro, and will help address the supply shortage in the area,” Ms. Devanadera said.

Laura Dern and DeWanda Wise in Jurassic World Dominion

LONDON — Casts old and new return for more dinosaur misadventures in Jurassic World Dominion, in a final outing concluding the second trilogy of films in the popular franchise.

The movie is set four years after the destruction of the remote island of Isla Nubar, and dinosaurs roam the entire world, living and hunting among humans.

Jurassic Park actors Laura Dern and Sam Neill reprise their roles as paleobotanist Dr. Ellie Sattler, now a soil and climate change scientist, and paleontologist Dr. Alan Grant, reuniting with their castmate from the 1993 movie Jeff Goldblum, who plays mathematician Dr. Ian Malcolm.

The movie sees them join forces with Chris Pratt’s animal behaviorist Owen Grady and Bryce Dallas Howard’s activist Claire Dearing, who have starred in the more recent Jurassic World trilogy of films.

“Both of them (Dern and Neill are) terrific friends… and changed my life for having known them for all these 30 years… We were in a movie that got people’s attention and entertained people,” Mr. Goldblum, who featured in 2018’s Jurassic World: Fallen Kingdom, told Reuters at a London press event for the movie on Friday.

“And now, for the first time, being reunited on screen and getting a chance to work together under these interesting circumstances with this new cast… what a parade and a cobb salad of lucky teammates for me.”

The film, which begins its global cinema roll-out on June 1, features plenty of stunning visual effects showing the dinosaurs living alongside humans. Soon enough, threats emerge.

“What I’m so grateful for and why I felt privileged to come back as Dr. Ellie Sattler is it has a deeply rooted environmental message as the entire franchise does, because ultimately it’s about corporate greed and previous extinction,” Ms. Dern said.

Ms. Howard, whose character was former operations manager at the now closed dinosaur park in the first Jurassic World movie, said wrapping up the trilogy which began in 2015 was emotional.

“I cried so much,” she said.

“There were some of the actors on my flight home, and they messaged everyone going like, ‘Bryce cried the entire 10 hours home.’ I’m like, ‘I know’.” — Reuters

THE Ortigas business district is seen from Antipolo. — PHILIPPINE STAR/ MICHAEL VARCAS

By Cathy Rose A. Garcia, Managing Editor

THE PHILIPPINES saw an increase in the number of buildings certified as “green” during the coronavirus disease 2019 (COVID-19) pandemic.

Angelo Tan, country lead for the Philippines at the Climate Business Department of the International Finance Corp. (IFC), said there are currently over 50 projects, which cover roughly 86,0000 square meters (sq.m.), that have received EDGE (Excellence in Design for Greater Efficiencies) certifications in the country.

“What is interesting is that more than half of those projects were certified in 2022 alone. You’re seeing a lot of interest in recent years. In addition to that we have 3.7 million sq.m. in the pipeline that are pursuing EDGE,” he said during a fireside chat at the BusinessWorld Virtual Economic Forum on May 25.

EDGE is a building certification system created by the IFC for emerging markets. It seeks to promote resource efficiency in buildings by adopting designs that help reduce materials, water, and electricity consumption.The IFC is a member of the World Bank Group.

“During the lockdowns people had to pause and reevaluate how they can ensure a green, resilient and inclusive recovery from pandemic. At the same time, the pause allowed them to think how they can do retrofits for their projects,” Mr. Tan said.

However, the development of green buildings in the Philippines is still slow compared to its Southeast Asian neighbors.

“In the area of green buildings so far, we have a little over 200 plus green buildings — the majority of which are office towers in Metro Manila. It’s been very slow, largely focused on the elite segment of the property sector. We need to make green and resilient infrastructure more accessible to a greater part of the population,” Mr. Tan said.

The IFC is working to dispel the widespread notion that green buildings are expensive and complex.

“What we do in the IFC Climate Business Department is we develop standards such as EDGE and Building Resilience Index that make it easy and less expensive to develop green and resilient buildings… We are able to come up with demonstration projects that have the image of greater accessibility for more people,” Mr. Tan said.

With EDGE, the IFC has brought down the price of certification fees for green buildings compared to other conventional green building certifications.

“We offer a lot of flexibility so developers can reach the required levels of green building certifications… We also reduce the complexity of the green building process… by identifying the most cost-effective measures to build green,” he said. “(EDGE) streamlines the green building certification process.”

One of the EDGE “champions” is Imperial Homes Corp., whose affordable housing projects received EDGE certifications.

“Their projects have reached a very high level of sustainability, high and advanced level of certification. If projects like that can be designed and built as green, then even other projects can achieve the same level of sustainability,” he said.

Aside from housing projects, Mr. Tan said they have also working on projects not traditionally seen as “green” such as industrial warehouses, a healthcare facility, hotel and resort.

“By reaching out to other building typologies, we are sending out the message that green is not just for high-end office towers in Metro Manila,” he said.

Local government units (LGU) can also help support the advancement of green buildings by creating an enabling environment.

“Governments can put in place incentives that can help encourage the creation of more green buildings. These don’t have to be financial of fiscal incentives, it can be non-financial incentives… Non-financial incentives include an increase in allowable floor area or building height if they certify their projects as green,” Mr. Tan said.

Mr. Tan believes green buildings are not just a trend, but are here to stay. He cited the buildings’ efficiencies that result in savings for owners and tenants, as well as the positive impact on real estate brands.

“We’re seeing lot of investors now want to put money in climate smart investments. They are right to believe brown assets can stagnate in a couple of years… Green buildings make sense. A lot of early adopters are benefiting from the advantages of green building certification,” he said.

TAIWAN’S worst coronavirus disease 2019 (COVID-19) outbreak has left the island’s insurers bracing for more than $1 billion in claims that the financial regulator is urging them to honor.

The head of the Financial Supervisory Commission (FSC), Huang Tien-mu, has ordered insurers to pay out on valid COVID-related insurance policies after they faced criticism from lawmakers for dismissing claims, canceling policies and delaying payouts.

Insurers are looking to limit their losses on policies after underestimating the extent of the disease. There are currently more than 6.3 million still-active COVID-related policies and another million waiting for approval, according to the FSC. This year, insurers have already paid out more to customers — NT$2.6 billion ($89 million) — than the NT$2.1 billion in revenue they have received from premiums.

And with only around 2% of policies subject to claims so far and Taiwan’s outbreak showing no sign of abating, insurers are facing a wave of further claims in June and July. Speaking to lawmakers last Monday, Huang said payouts will likely be higher than the NT$41 billion estimate mentioned by lawmakers.

While that is just a tiny fraction of the NT$2 trillion in net assets held by Taiwan’s insurance industry, the majority of those are held by the large life insurers. The potential claims represent around 25% of the assets held by property insurance companies, which were among the most active in selling COVID-19 policies.

RISK MODELS Property insurers, which focus primarily on car protection, have struggled to find growth in recent years and saw COVID-19 as a great opportunity, according to Andy Chang, director of Taiwan Ratings Corp. When working out their risk models, many miscalculated the potential number of cases by a factor of almost 100. They also didn’t adequately estimate the necessary capital buffer.

“They shouldn’t have just said, ‘how much are our competitors selling? We want to sell that much too,’” Chang said in a phone interview.

Even Taiwan’s largest insurers are likely to take a hit. Claims at Fubon Life Insurance Co. and Cathay Life Insurance Co. could reach NT$5 billion, equivalent to about 2% of their net income this year, Bloomberg Intelligence analyst Steven Lam wrote in a May 13 note.

The generosity of the policies insurers sold is a major part of the problem. Since the beginning of the pandemic, many companies have offered policies protecting customers against negative health impacts of COVID-19 and the associated costs.

Quarantine insurance is among the most popular. For as little as NT$666 a year, the insurers guarantee to pay out NT$50,000 if the customer is required by the government to isolate. If the client later tests positive for COVID-19, they can get another NT$50,000.

‘BLOW UP’ Until recently, Taiwan had managed to keep the pandemic broadly under control, making COVID-related policies a solid source of revenue. But cases began surging in late April as the omicron variant breached the island’s border controls.

Taiwan reported more than 76,000 local cases and a record-high 145 deaths on Sunday, according to data from the Centers for Disease Control. The health minister has said around 15% of the population — about 3.5 million people —could end up getting COVID-19.

Siang Lin, a financial industry professional working in Taiwan, bought a COVID-19 insurance policy that he renewed once it expired.

“I thought, sooner or later it’s going to blow up here,” he said. “We’re all going to end up getting it — that’s why I extended my policy.”

Lin was right. He got COVID-19 in early May and is currently awaiting his NT$50,000 payout. — Bloomberg

FILIPINO chess players reaped honors for the country as Michael Concio, Jr. and the Philippine Para Team standouts Jasper Rom, Menandro Redor and Cheryl Angot all emerged triumphant in separate tournaments.

Mr. Concio, 17, ruled the Hanoi International Master (IM) Tournament in Vietnam after finishing unbeaten with seven points on five wins and four draws while Messrs. Rom, Redor and Ms. Angot topped their respective divisions in the Asian Online Championships for People with Disabilities over the weekend.

Backed by Dasmariñas congressman Pidi Barzaga, Mr. Concio needed just a ninth and final-round draw with Indonesian Aditya Bagus Arfan to claim the win and the 121.2 FIDE rating points that went with it.

In the concurrent Grandmaster Tournament also in Hanoi, another Filipino IM Daniel Quizon finished fourth with five points and also gained rating points.

Thanks to their efforts, the 17-year-old Mr. Concio zoomed to a 2,380 live rating while the 18-year-old Mr. Quizon to 2,420.

For Mr. Rom, he reigned supreme in the Physically Impaired Open division by ending up with 4.5 points in five rounds while Mr. Redor was a cut above the rest in the Visually Impaired Open category also with 4.5 points.

Ms. Angot, for her part, shocked heavy favorite WIM Irina Ostry of Kyrgyzstan in the last round to strike gold in the Physically Impaired women section likewise with 4.5 points.

Mr. Mendoza smashed Indian R.P. Kanishri to deliver the country’s only silver with 3.5 points.

“These are all for country and flag,” said national para team coach James Infiesto, who thanked the PSC, Philippine Paralympic Committee and the NCFP for their support.

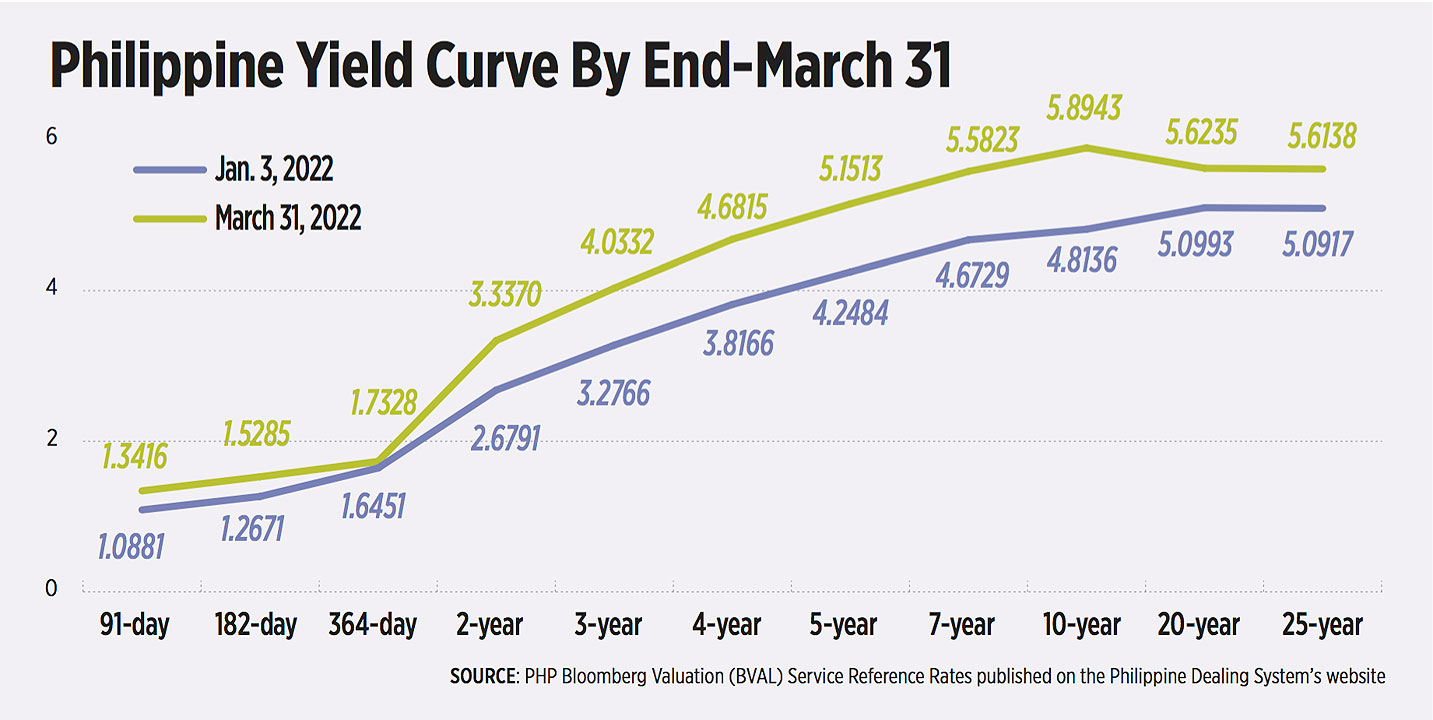

FINANCIAL MARKETS could experience another volatility in the near term as major central banks turned hawkish amid inflationary pressures due to the ongoing Russia-Ukraine war, analysts said.

In the first three months of the year, the Philippine Stock Exchange index (PSEi) averaged 7,230.08, up by 0.3% quarter on quarter from the 7,208.37 seen in the fourth quarter of last year, data from the local bourse showed. Annually, the benchmark PSEi went up 5% from the 6,882.77 average in the first quarter a year ago.

On an end-period basis, the PSEi was 1.1% higher in the first quarter at 7,203.47 versus the preceding quarter.

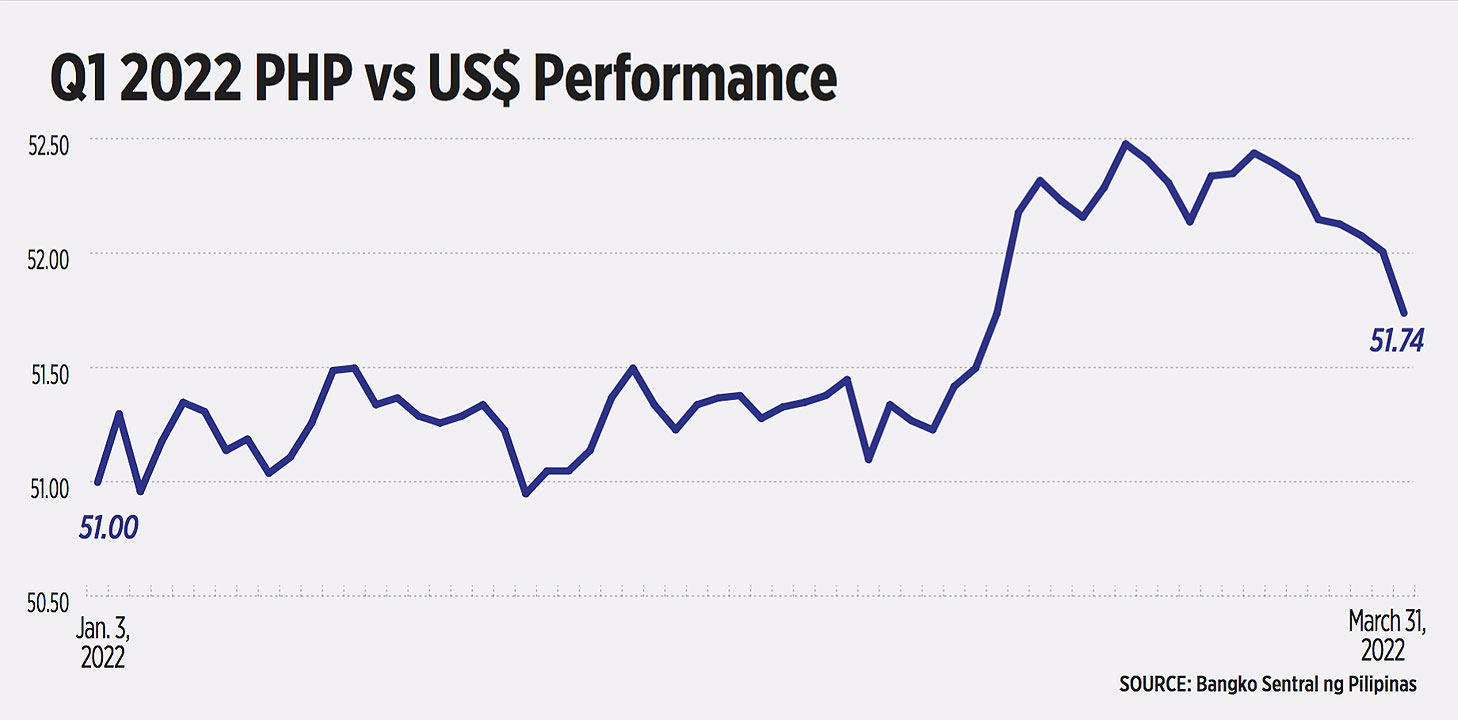

Meanwhile, Bangko ng Sentral ng Pilipinas (BSP) data showed the peso depreciated to P51.96 against the dollar as of end-March from P48.466:$1 last year.

Demand for government bonds remained strong during the period. Treasury bill (T-bill) auctions conducted in the first quarter saw total subscription for the quarter amounting to around P614.2 billion, which is around 4.1 times the P148-billion aggregate offered amount. This oversubscription amount of P466.2 billion, however, was lower than the P311.6 billion in the previous quarter.

Demand for Treasury bonds (T-bonds) were likewise robust with a total subscription amount of P519.4 billion, almost twice more than the offered amount of P225.9 billion.

At the secondary bond market, domestic yields were higher by a range of 90.94 basis points (bps) for the seven-year T-bond to the 108.07 bps for the 10-year paper compared with end-December 2021 levels.

Yields rose across the board on a quarter-on-quarter basis. In the first quarter, rates were higher by an average of 62.01 bps during the reference period, according to the PHP Bloomberg Valuation Service Reference Rates published on the Philippine Dealing System’s website.

The Philippines welcomed the first quarter with the resumption of strict Alert Level 3 in various parts of the country to contain the Omicron-driven surge. It was subsequently relaxed to Alert Level 2 in February then to a more lenient Alert Level 1 starting March.

However, as the economy slowly gains ground from the lockdowns, Russia’s invasion of Ukraine started in on Feb. 24. With Russia being the world’s second largest producer of crude oil, news of the war sent global oil prices — and other commodities — to multi-year highs.

Inflationary pressures brought by the war triggered various economies, including the Philippines, to start hiking record-low borrowing costs in order to quell fast-rising inflation.

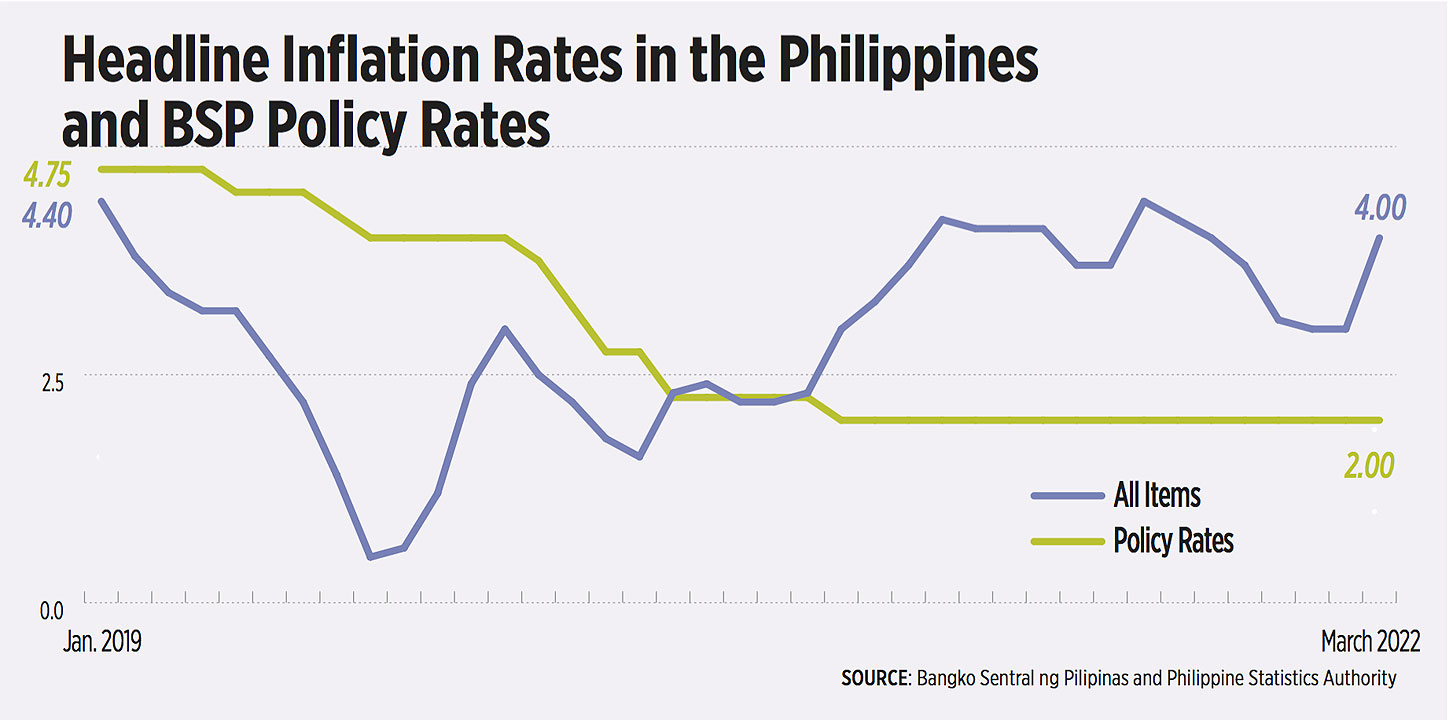

Despite these, the country’s economic output firmed up by market-beating 8.3% in the first quarter. For the first time since 2018, the BSP decided to hike benchmark interest rates by 25 bps in May to control above-target domestic inflation. It signaled another rate increase by June.

Consumer price index peaked to a 40-month high of 4.9% year on year in April from a 4% print in March, latest data from the Philippine Statistics Authority (PSA) showed.

WHAT INDICATORS TO WATCH OUT FOR Despite the ongoing economic effects of the Russia-Ukraine conflict, analysts advise investors to remain cautious of the US Federal Reserve’s upcoming rate hikes amid global and local inflationary pressures in the months ahead.

“Russia-Ukraine conflict still highly uncertain: Risk that it could drag on. Possible turning point if it suddenly ends, but this is still highly speculative,” Rizal Commercial Banking Corp. Chief Economist Michael L. Ricafort said in an e-mail interview.

University of Asia and the Pacific Chief Senior Economist Cid L. Terosa said as the Russia-Ukraine war drags on, it will continue to exert upward pressure of prices and interest rates.

“Higher inflation will negatively affect the equities market since it could lower sales and profits of firms. Higher interest rates could negatively affect the equities market since it is more attractive to deposit money in banks or purchase fixed-income securities,” Mr. Terosa said in an e-mail.

“Conversely, higher interest rates can lead to higher demand for fixed-income securities because investors can purchase fixed-income securities with higher interest rates,” he added.

UnionBank of the Philippines, Inc. Chief Economist Ruben Carlo O. Asuncion said investors should also anticipate the US Fed’s rate tightening implications.

“The 10-year US treasury rate will provide a picture of the ripple effects of a more hawkish US Fed. As such, investors should expect US/offshore rates to exert influence on local bond yields,” he said in an e-mail.

“Oil prices may also bloat the trade deficit and further challenge the local currency, which is already assumed to be impacted by the sustained lockdowns in China. Aside from these, inflation expectations should need to be watched carefully moving forward,” Mr. Asuncion said.

At the domestic front, ING Bank NV Manila Senior Economist Nicholas Antonio T. Mapa said the market should keep an eye out for inflation, fiscal position, and economic growth.

“Looking at global markets, we may need to monitor developments surrounding the direction of monetary policy (US Fed, European Central Bank, Bank of England, etc.), and global growth, most notably the state of China’s economy,” Mr. Mapa said in an e-mail.

RATE HIKE IMPLICATIONS The central bank’s decision to hike rates will help support the peso, Mr. Mapa said, “but this is not a hard and fast rule.”

“We remember well that in 2018, BSP resorted to an aggressive 175 bps rate hike cycle that did very little to shield the currency. Higher inflation and rising interest rates tend to slow down economic growth, especially ones that rely heavily on consumption for much of its activity,” Mr. Mapa said.

Meanwhile, the US Fed’s aggressive rate hike for the year could dampen the Philippines’ financial market growth.

“The Federal Reserve rate hike will most probably slow down the recovery and growth of Philippine financial markets in Q2 2022 and for the rest of the year. The BSP, however, has taken an important measure to stem the outflow of funds by raising policy rates,” Mr. Terosa said.

“This move by the BSP will stabilize the growth and recovery of Philippine financial markets, but the performance of Philippine financial markets in Q2 2022 and the rest of the year won’t be stronger than Q1 2022,” he added.

With the incoming new administration, political and economic stability as well as investor sentiment will most likely figure significantly after the second quarter, Mr. Terosa said.

“The new administration has to induce positive investor sentiment in the first three to six months of its term in order to boost Philippine financial markets for the rest of the year,” he said.

With these in mind, below are the analysts’ outlook for each of the key markets.

FIXED-INCOME Mr. Asuncion: “Bonds are more sensitive to interest rate adjustment with a hike resulting to bond prices falling (because of higher interest rates). The continuing tightening of US financial markets may result to attraction of US bonds over emerging market ones. This can leave markets like PH with lower trading volume and interest from foreign players.”

Mr. Ricafort: “Rising trend in US/global interest rates and bond yields amid the continued Russia-Ukraine war and more aggressive Fed monetary tightening would still be important exogenous factors.

“The local fixed income market would also take cue from the incoming administration’s economic team, which needs to reduce the country’s debt-to-GDP ratio from the 17-year high of 63.5% as of Q1 2022 after the government’s wider budget deficits and more borrowings since the pandemic, through intensified tax collections, tax and other fiscal reform measures, disciplined spending through anti-wastage/anti-leakages/anti-corruption and other good governance measures to improve the country’s fiscal performance and overall debt management over the long term and for the coming generations.”

Mr. Mapa: “Bond markets will continue to see pressure on yields to increase as policy rates (and inflation) exert pressure on borrowing costs to rise.”

Mr. Terosa: “Higher interest rates can lead to higher demand for fixed-income securities because investors can purchase fixed-income securities with higher interest rates.”

EQUITIES Mr. Asuncion: “On the equities side, market upside will be tempered by an environment of higher interest rates here and abroad which is likely to spill over into a restrained macro and earnings outlook… higher interest rates may result for higher demand for emerging market stocks and other equities.”

Mr. Ricafort: “Reflecting relatively elevated inflation could be a drag on stock markets amid higher borrowing/financing costs and the resulting slower economic recovery prospects and even potential risk of recession that could lead to some slowdown in sales, lower earnings, tighter margins, and lower valuation.”

Mr. Terosa: “Higher interest rates, however, will negatively affect the equities market this quarter because an increase in interest rate will make it more attractive to park funds in bank deposits or fixed-income securities.”

FOREIGN EXCHANGE Mr. Asuncion: “Peso weakness as an outcome of May elections is expected — in sync with previous election cycle trends… A more hawkish US Fed actions may result to a weaker PHP and, thus, more exchange rate management moves from the BSP with the strong conviction to maintain the 52.50 level through suspected BSP agent banks. Any rally beyond the said price has been met by strong offers by the BSP through its market conduits.”

Mr. Ricafort: “Election-related catalysts could also partly determine the direction of the exchange rate in view of the honeymoon period for the incoming administration starting the first 100 days and then about six months to one year for any signals and clearer direction on policy priorities including foreign policy, reform measures, and anti-corruption/governance standards (especially adherence of Environmental, Social, and Governance standards that are increasingly encouraged if not even required by global investors and regulators) that would matter on the economy and fiscal performance/debt management.”

Mr. Mapa: “The Fed rate hike may prompt local investors to exit in favor of more attractive returns relative to risk in the developed markets. This in turn will, at least to some extent, exert pressure on BSP to continue its rate hike cycle to maintain attractiveness relative to our risk profile. The exchange rate will likely be impacted, as will bond markets as local interest rates rise. Likely, under depreciation pressure given both current account (trade deficit) and financial account (interest rate differentials) dynamics.”

Mr. Terosa: “If inflation persists, the peso will weaken in Q2 2022. As the peso weakens, upward pressure on inflation is expected. Consequently, the equities market will undergo persistent downward pressures.

“Hence, it appears that both the equities and foreign exchange markets will contend with negative pressures arising from higher interest rates and inflation in Q2 2022. The fixed-income market will most probably perform better than the equities market in Q2 2022.” — Ana Olivia A. Tirona

")

EDGE is a building certi

EDGE is a building certi