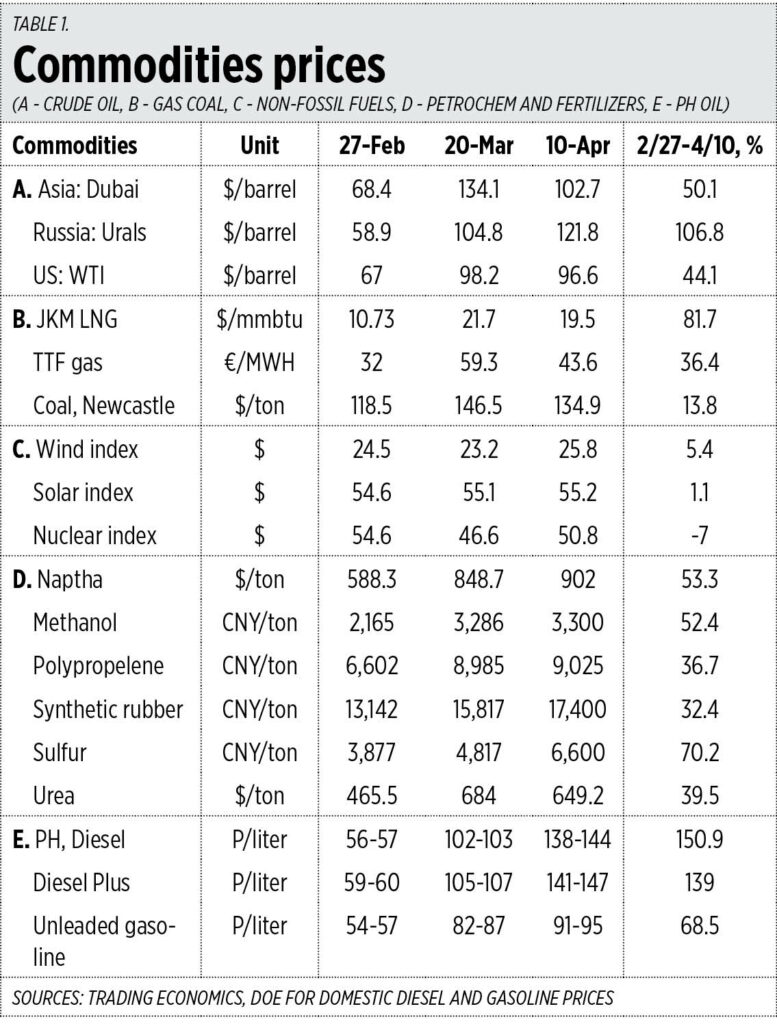

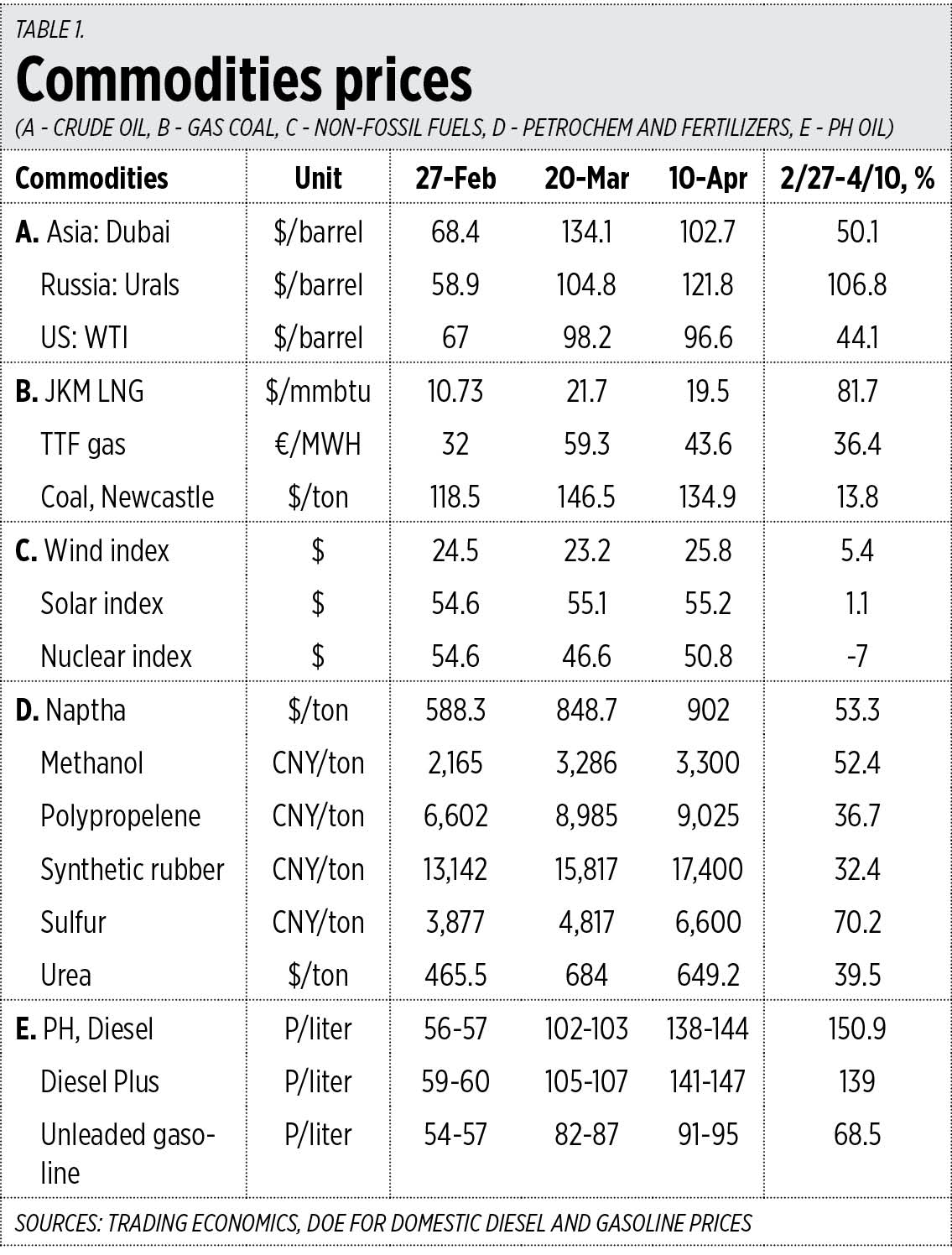

Here is an update of my weekly monitoring of “Trumpflation” because of the US and Israel’s irresponsible and prolonged war on Iran. The Strait of Hormuz was open until Feb. 27, the day before the US-Israel attacks. Let us look at some notable numbers, after six weeks of war, from Feb. 27 to April 10.

1. The price of Dubai crude is up by 50%, WTI or US oil is also up by 44%, meaning even the US is experiencing a tight oil supply. The biggest increase is Russia’s Urals oil which is up by 107%. Petron Philippines was forced to buy oil from Russia to help stabilize domestic oil supply.

2. The prices of imported liquefied natural gas (LNG) also jumped, with the Japan Korea Marker (JKM) up by 82%. Our big LNG power plants in Batangas, owned by LNGPH, will reflect these higher prices but the good news is that our LNG imports from the Gulf are small.

I chanced upon LNGPH President Yari Miralao, he said that “Only 7% of LNGPH’s cargoes since mid-2023 come from the Middle East. The remaining 93% are sourced from other regions. We remain vigilant in managing our supply portfolio and ensuring that fuel for our plants are secured in a timely, reliable, and predictable manner.”

3. Coal prices have increased by only 14%. Even many greenie Europeans are firing up their remaining coal plants and shedding plans of their early decommissioning.

4. The non-fossil fuels solar-wind index is up by only 1% and 5%, they are not attractive for many energy investors. The nuclear index even contracted by 7%.

5. The prices of industrial petrochem and fertilizer products remain high. Methanol is up by 52%, naptha by 53%, sulfur 70%, and urea 40%. Sulfur, phosphate, ammonia, and urea are important components of fertilizer production. Solar and wind power sources cannot produce naptha, methanol, sulfur, etc., only crude oil and natural gas can.

6. Our domestic diesel prices have jumped up by 151% while gasoline prices have increased by 68% (see Table 1). The reasons why the increases in domestic oil prices are higher than global crude oil prices include: a.) the Peso/$ depreciation, b.) higher shipping fees including insurance, and, c.) low or non-optimized local diesel storage facilities, among others.

Last week the Independent Electricity Market Operator of the Philippines (IEMOP) released the market operations at the Wholesale Electricity Spot Market (WESM) for March, to be reflected in the April electricity billing.

Power demand in March was 509 megawatts (MW) more than in February, while supply in March was 79 MW less than in February. The lower reserve margins led to the higher WESM price of P4.31 per kilowatt-hour (kWh) in March from P3.50/kWh in February.

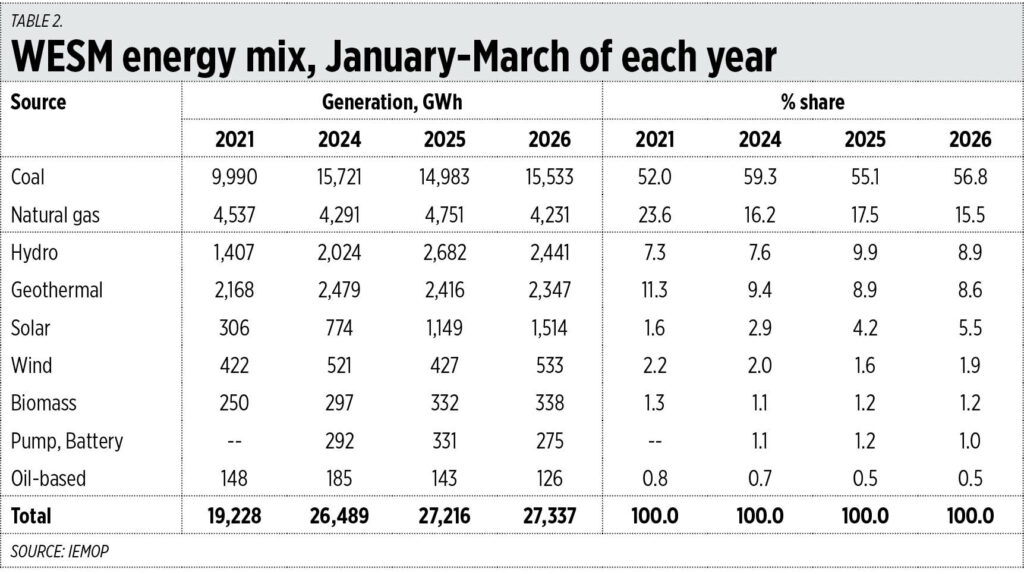

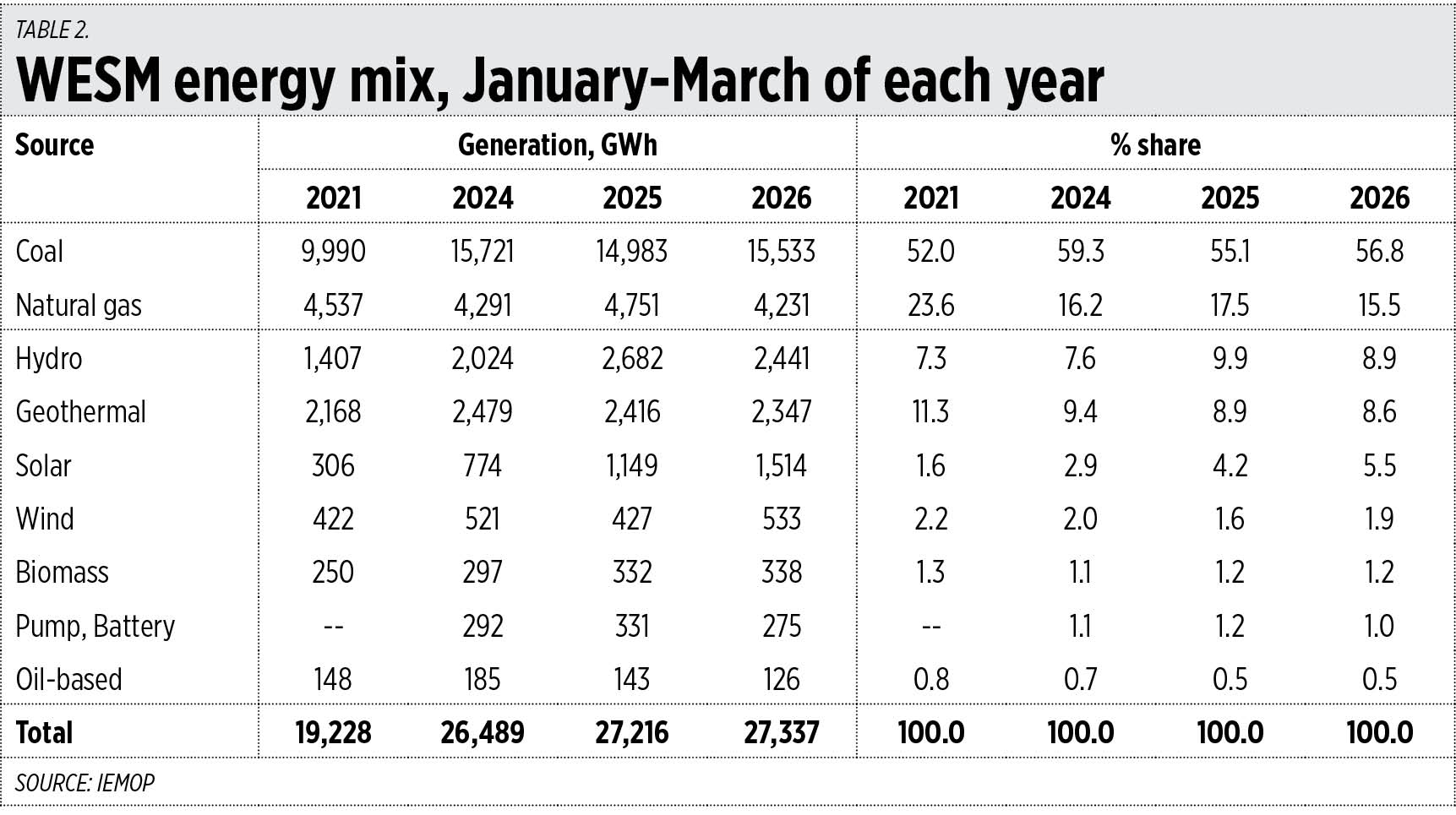

I checked the generation mix in the first quarter (January to March), then looked at data from 2021 onwards. Here is some of the evolution in our electricity sourcing.

1. For fossil fuels, the share of coal increased from 52% in 2021 to 59% in 2024, and decreased a little to 57% in 2026. The share of natural gas has been consistently declining, from 24% in 2021 to 15.5% in 2026.

2. For conventional and stable renewable energy sources, hydro power’s share has increased marginally from 7% in 2021 to 9% in 2026. Geothermal has seen a declining share, from 11% in 2021 to 9% in 2026.

3. For variable and unstable renewable energy sources, the share of solar has been rising, from 1.6% in 2021 to 5.5% in 2026, while wind’s share has marginally declined, from 2.2% in 2021 to 2% in 2026. Biomass’ share is flat at 1.2% (see Table 2).

Despite the constant demonization of coal by climate alarmists, coal is the most reliable and most affordable electricity source to avoid blackouts. By installed capacity, coal is only 40% of the total, but in actual electricity generation coal is 57% of the total.

The dirtiest energy for lighting is candles not coal. We need more coal, not less.

On hydro, I remember my tour last month of the Ambuklao hydro plant in Benguet, owned by SN-Aboitiz Power (SNAP), when I was toured by Ambuklao plant manager Hollis Fernandez. This was a day after PEPIF 2026 in Baguio. I was really amazed at how SNAP has significantly expanded Ambuklao’s capacity. It started out producing 75 MW of electricity when it was commissioned in 1956, then stopped operations in 1991 after the big earthquake. SNAP took over in 2007, rehabilitated and modernized it, and got 112.5 MW of power from it. Getting 37.5 MW more power while using the same reservoir and dam is a huge engineering innovation by SNAP.

As of this writing, the day before publication, WTI oil is $104.5/barrel, another jump from last Friday’s closing of $96.6/barrel. This comes after the US-Iran negotiation in Pakistan collapsed, meaning prolonged conflict and more Trumpflation.

One measure that the Department of Energy can explore is to raise our diesel storage by optimizing any underutilized storage facilities of private oil and LNG companies in the country.

I chatted briefly with Arnel Santos, the current COO of Meralco PowerGen (MGEN) Thermal and a former Shell executive for 25 years (starting in Shell Philippines, then moving to Shell Singapore, Malaysia, and Canada). He told me that “The Philippines does have significant storage, most of it sits within commercial terminals that are continuously used for operations… available working tank space for incremental volumes for specific products like diesel and in specific locations… Since we are in crisis all available storage should be leveraged. This is no different from suspending WESM and going on admin pricing.”

I hope that Energy Secretary Sharon Garin will consider this proposal, that the Energy department or the Philippine National Oil Co. rent those underutilized tanks at negotiated rates.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an internationa fellow of the Tholos Foundation.

minimalgovernment@gmail.com

,-Japanese-actor-and-screenwriter-Jûzô-Itami")

")