Fiscal policy at the frontline: responding to the Iran war shock

The fiscal response to the Iran war shock is not conceptually complex but it is politically and institutionally difficult. The escalation of hostilities, particularly threats to the Strait of Hormuz, is driving energy price volatility at a time when global public finances are already under severe strain. As the International Monetary Fund (IMF) warns, governments are confronting these shocks “at a moment when public finances are already stretched by long-term pressures.”

The policy challenge is clear: protect the vulnerable without destroying fiscal sustainability. Anything less risks compounding today’s crisis with tomorrow’s instability.

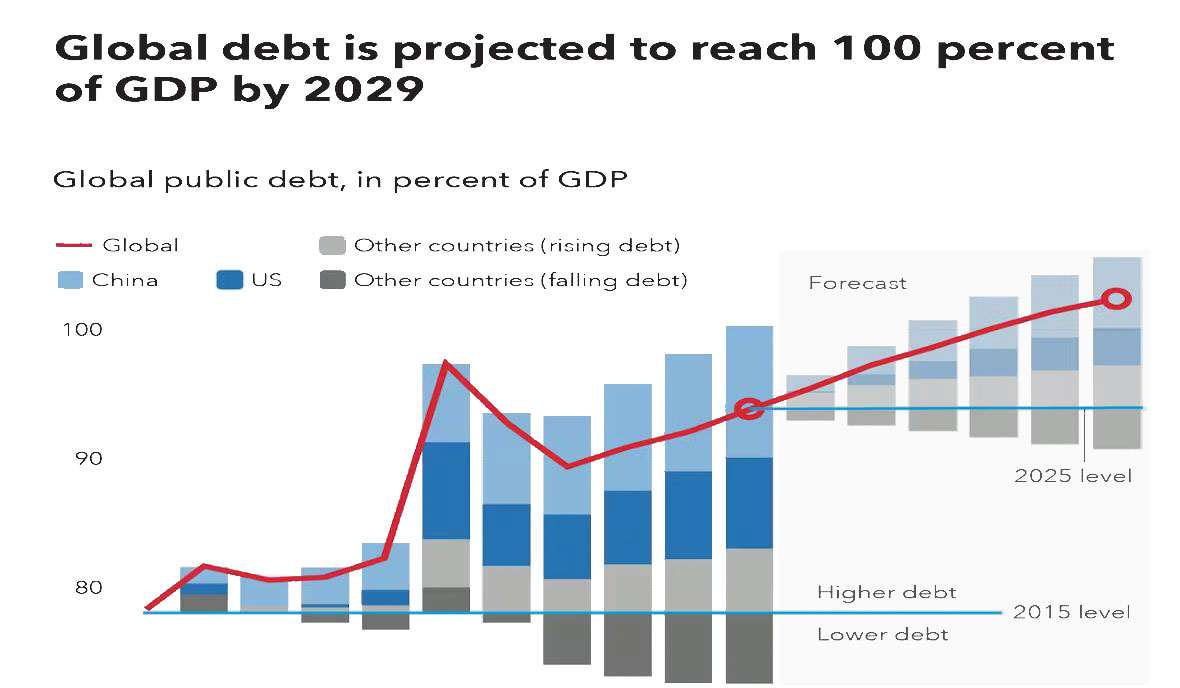

A WORLD WITH NO FISCAL CUSHION

The global starting point is weak. Fiscal deficits hover around 5% of GDP, while public debt is nearing 100% of GDP. Interest payments at 3% of GDP alone are consuming an increasing share of national income. Many economies are still scarred from the pandemic, leaving governments with limited room to respond.

This is not a normal starting point. Governments are entering this crisis with very little buffer, if at all.

This matters because the Iran war shock is not a one-off disturbance. In a severe scenario where oil prices double and financial conditions tighten, debt vulnerabilities could surge, particularly in emerging markets. In short, there is no fiscal buffer to waste, no room for indiscriminate fiscal expansion. Every peso spent must be justified, targeted, and temporary.

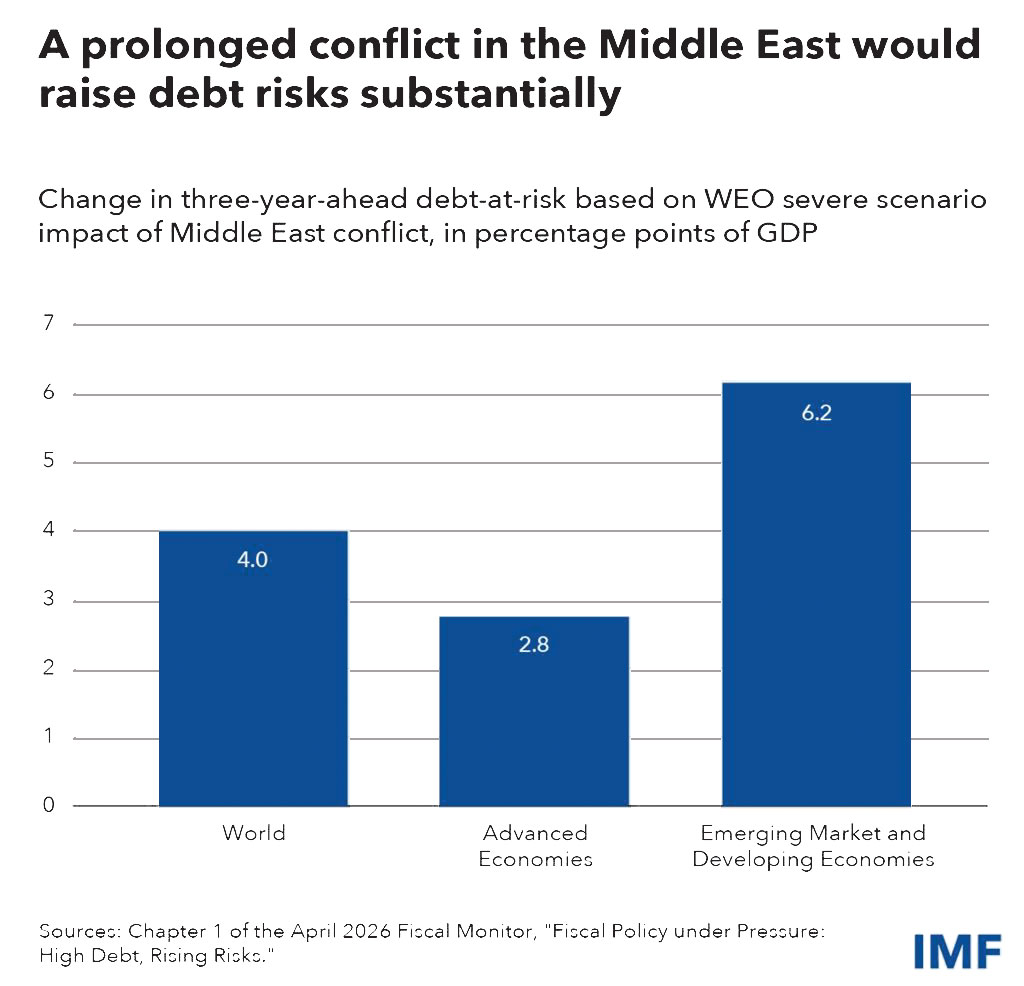

WHEN THERE IS POLICY COMPLACENCY

There is also the danger of policy complacency. In a severe scenario where oil prices surge and financial conditions tighten, the IMF estimates that debt-at-risk could exceed 120% of GDP, especially in emerging markets.

This is the risk channel policymakers often underestimate: what begins as an energy shock can quickly become a debt sustainability crisis. Short-term fiscal support must be paired with a credible medium-term consolidation strategy, or markets will impose discipline abruptly and painfully.

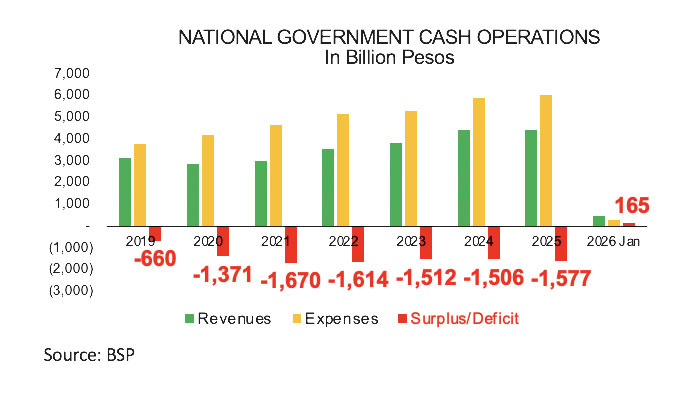

THE PHILIPPINES: HIGH EXPOSURE, LIMITED SPACE

The Philippines enters this crisis with constrained fiscal space:

• Fiscal deficits have averaged over P1.5 trillion in recent years

• Public debt has risen to about 63% of GDP

• Interest payments now exceed 3% of GDP

• Structural spending needs on infrastructure, poverty reduction, education, and health remain large.

Compared with ASEAN peers, the country’s fiscal position is among the weakest. Even as consolidation has begun, the margin for policy error is thin. The country faces a classic squeeze. Its high spending needs are to be accommodated within a weak fiscal space, and rising financing costs.

WHAT FISCAL DISCIPLINE SHOULD MEAN NOW

Fiscal discipline today cannot mean blunt austerity. As the IMF stressed, the more relevant definition is strategic: protect stability today without compromising tomorrow.

This implies three non-negotiables:

1. Targeted and time-bound support. Support for households and firms is justified — but only if tightly focused on those most exposed and least able to cope. In the Philippines, pandemic-era safety nets, without the corruption and incompetence, can be reactivated, but they must not become permanent entitlements.

2. Reallocation before borrowing. For fiscally constrained countries like the Philippines, new spending should come primarily from reprioritization, not additional debt. This requires politically difficult choices of either cutting or delaying low-impact programs in favor of crisis response. Congress should have learned its lesson by now to avoid flood-control scandals that only plunder public resources without any payback.

3. Credible commitment to consolidation. Any short-term expansion must be paired with a clear medium-term consolidation path, or risk triggering higher borrowing costs and weakening investor confidence. When business trust is lost, business activities are curtailed, economic growth loses its momentum and joblessness ensues.

THE FUEL SUBSIDY DILEMMA

Fuel subsidies are the most contentious instrument — and for good reason. As the IMF warns, broad subsidies are:

• Costly

• Poorly targeted

• Difficult to withdraw

• Distortive to consumption behavior

Yet in the Philippine context, a blanket rejection is unrealistic. The collateral harm is just too immense.

Without intervention:

• Transport fares will spike

• Inflation will broaden through higher logistics costs

• Real wages will erode

• Growth will weaken

• Social pressures will intensify

The real policy choice, therefore, is not whether to intervene, but how.

This means we need to adopt narrow, temporary, and well-targeted transport subsidies focused on public utility vehicles and vulnerable commuters while avoiding economy-wide price suppression.

THE HIDDEN COSTS OF INACTION

Failing to act or acting poorly carries its own fiscal risks:

• Higher social protection spending from economic distress

• Lower tax revenues due to weakened activity

• Reduced productivity as mobility declines

• Market distortions in transport and logistics sectors

In other words, poorly designed austerity can be as costly as poorly designed subsidies.

GOVERNANCE: THE BINDING CONSTRAINT

All policy prescriptions collapse without credible governance.

In the Philippines, persistent concerns about corruption and inefficiency highlighted by controversies such as flood control spending and impeachable malversation of public funds undermine the feasibility of expenditure reallocation. Without reforms:

• Fiscal space will continue to leak

• Public trust will erode

• Necessary adjustments will be politically blocked

Fiscal policy is only as strong as the institutions that implement it. Fiscal space is not just about higher revenue, it is also about trust.

WHAT MUST BE DONE NOW

A credible fiscal response to the Iran war shock requires a shift from reactive spending to strategic policy design, one that is rules-based:

1. Institutionalize targeting mechanisms. Build robust systems to identify and deliver support to vulnerable sectors quickly and accurately. Use of financial technology and automation will prevent leakages, especially at the barangay level in the Philippines.

2. Enforce spending discipline. Audit and reallocate low-impact or corruption-prone expenditures toward crisis priorities. Our state auditors should remain independent, shielded from politics and partisanship.

3. Strengthen transparency and communication. Clearly explain policy trade-offs to the public to sustain support for difficult decisions. Public ownership of public policy is essential to successful reforms and social change.

4. Adopt flexible fiscal rules. Incorporate escape clauses that allow countercyclical intervention during shocks without abandoning long-term discipline. Fiscal consolidation should lead to better fiscal outcomes and growth paths.

5. Mobilize domestic revenue. Rationalize tax incentives and broaden the base to finance necessary interventions sustainably. There should be a space for considering a wealth tax or even monopoly tax with limited economic repercussion.

BEYOND FISCAL POLICY: A WHOLE-OF-GOVERNMENT RESPONSE

The Iran war shock is not a purely fiscal problem. It demands coordination across:

• Energy policy (diversification, renewables)

• Monetary policy (inflation containment)

• Transport regulation (efficiency and competition)

• Social policy (targeted protection)

The current crisis committee created by President Ferdinand Marcos, Jr. is a good start but the civil society expects quicker responses to the many proposals already forwarded. That would cover precisely intersectoral concerns and collaboration and produce more responsive results. Coordination gaps should be tackled at the cluster groups, especially for energy and economics. The challenge is to ensure that there is one single command center for easier coordination and expand the scope for pre-emptive strategy as the crisis quickly unfolds.

Relying on a single tool, whether subsidies or austerity, will fail. As the saying goes, if all you have is a hammer, everything looks like a nail.

THE CHOICE FOR THE PHILIPPINES

The Philippines cannot afford either fiscal recklessness or fiscal paralysis.

The path forward is narrow but clear: targeted support, disciplined spending, stronger governance, and credible long-term consolidation.

Anything less risks turning a temporary external shock into a permanent fiscal crisis.

Diwa C. Guinigundo is the former deputy governor for the Monetary and Economics Sector, the Bangko Sentral ng Pilipinas (BSP). He served the BSP for 41 years. In 2001-2003, he was alternate executive director at the International Monetary Fund in Washington, DC. He is the senior pastor of the Fullness of Christ International Ministries in Mandaluyong.