AS A FOLLOW UP to my piece on October 2023 about the negative impact of the equity investment into the Maharlika Investment Corp. (MIC) on the capital ratios of Land Bank of the Philippines (LBP) and the Development Bank of the Philippines (DBP), my “Introspective” piece on Jan. 6 this year showed that after one year, the DBP remained slightly below the 10% regulatory minimum for Common Equity Tier 1 (CET1) through 2023, while the LBP’s numbers were already above minimum and significantly improved during 2023.

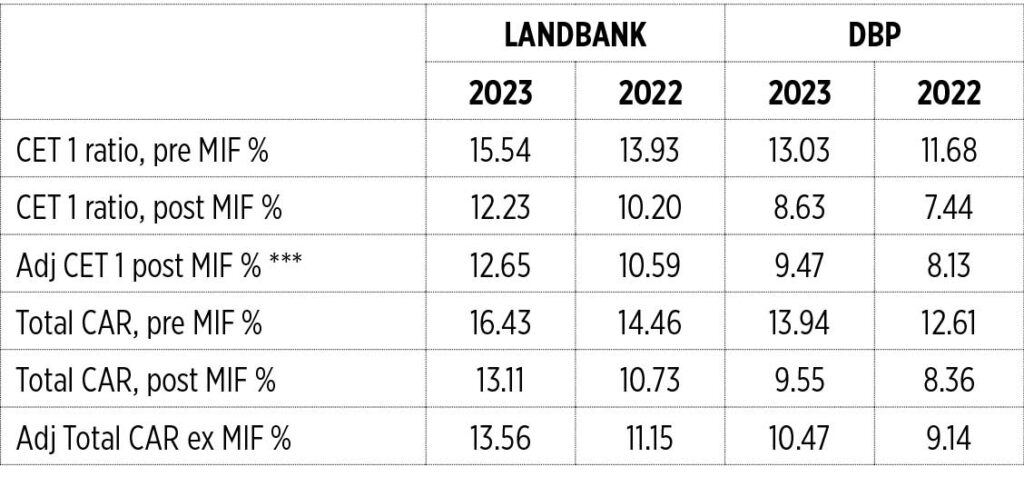

This writer has come upon new information that shows that the LANDBANK and DBP capital ratios are actually better than earlier computed. BSP Circular No. 781 series of 2013 (Part II, Item 9) — also published as Annex 59 of the Manual of Regulations for Banks (MORB) of 2021 — provides that “Any asset deducted from qualifying capital in computing the numerator of the risk-based capital ratio shall not be included in the risk-weighted assets in computing the denominator of the ratio.” Credit to LANDBANK President Lynette Ortiz and her Controllership group for pointing out Circular 781.

Based on the accompanying table, the DBP’s adjusted CET1 ratio by end 2023 was at 9.47%. If the DBP just records the same income for 2024 as it earned in 2023 (no profit growth) and its Risk weighted assets (RWA) grows minimally instead of contracting again, my estimate of its adjusted CET1 ratio of 10.35% will have met the 10% regulatory minimum. Hence, DBP President Michael de Jesus was correct in saying that “DBP… will meet the minimum capital ratios based on the results of 2024.”

In contrast, the Department of Finance (DoF) statement citing healthy Capital Adequacy Ratio (total CAR) for LBP at 16.42% and DBP at 14.78% as of November 2024 (https://tinyurl.com/2csrrx6o) is misleading on two counts — first, it refers only to the total CAR not CET1, and, second, the number does not account for capital deduction from the Maharlika Investment Fund (MIF) equity investment. The correct number is the CET1 adjusted for MIF equity.

RECAPITALIZATION OR IPO

This writer called out the recent IMF call for the immediate recapitalization of both government financial institutions (GFIs) so they could exit regulatory relief as half-wrong and one year late. Based on the updated/adjusted figures, the IMF was wholly wrong, since even the DBP would already be compliant by the end of 2024.

At the start of his term as Secretary of Finance, Secretary Ralph Recto announced the possibility of an initial public offering (IPO) for LBP and DBP to bolster their capital ratios. (“IPO seen to strengthen Land Bank, DBP,” Philippine Daily Inquirer, Feb. 23, 2024). This followed his announcement of the scrapping of the merger of LANDBANK and the DBP as proposed by his predecessor, Ben Diokno.

Bills were filed in Congress to amend the GFIs respective charters — Senate Bill 2804 (Senators Mark Villar and Francis Escudero) and House Bills 10720 (Rep. Bernadette Escudero) and 10817 (Rep. Wowo Fortes) for the DBP, and Senate Bill 2760 for LBP (Senator Escudero).

This piece discusses whether the proposed amendments to the charters of the LBP (RA 3844, as amended) and the DBP (RA 8523 amended by EO 81) are supportive of their recapitalization, and whether it can lead to a successful IPO.

The critical factors are the increase in authorized capital, the building blocks in governance structures necessary for a successful public listing, and whether market conditions are favorable for such a public listing.

INCREASE IN AUTHORIZED CAPITAL

To pay for the additional paid-in capital called for by proposed charter amendments, the National Government has to infuse a total of P66.5 billion in paid-in capital to both GFIs, broken down as follows:

1. LBP, P50 billion. The proposed increase in authorized capital from P200 billion to P1 trillion (Section 6, SB 2670), means an increase of P800 billion. Under the Revised Corporation Code (RCC), 25% or P200 billion of this increase in authorized capital has to be subscribed. And 25% of the incremental subscription is P50 billion. This amount is exactly the P50 billion taken out of LBP for investment in Maharlika.

2. DBP, P16.562 billion. Authorized capital from P35 billion — of which P32 billion currently paid up — to P300 billion, or an increase of P265 billion (Section 7, SB 2804 and HB 10720, HB10817). Incremental subscription of 25% amounts to P66.25 billion; the corresponding additional paid up 25% of subscribed is P16.5625 billion. This additional paid-in capital of P16.562 is less than the P25 billion transferred to Maharlika.

The idea of the National Government having to recapitalize LBP and DBP to the tune of P66.5 billion raises a most basic question — why did they have to take out the capital from both GFIs in the first place?

How will the National Government infuse the additional paid in capital?

Option 1. Infuse cash. Very unlikely, given fiscal constraints such that DoF even had to resort to “sweeping” the so-called “excess funds” from various GOCCs — including PhilHealth and Philippine Deposit Insurance Corp.

Option 2. Extended “Dividend relief.” Most likely, both GFIs will be exempted from RA 7656 requiring them to declare 50% of their net income as dividends, until their capital build up meets the target amount. At current rates, this could take two to three years for the LBP and three to four years for the DBP. This “dividend relief” is completely separate from “regulatory relief” from minimum capital ratios, which is no longer an issue by end 2024 for DBP and was never an issue for LBP.

BUYING SHARES

Will the investing public be allowed to buy LBP and DBP shares? Yes.

Their original charters provide that only the National Government can own their shares. The proposed amendments now allow them to issue common and preferred shares (DBP Section 6, item k; for LBP Section 3 item n). The National Government will retain majority ownership of 70% while Government-Owned and -Controlled Corporations (GOCCs) can buy non-voting preferred shares of both GFIs.

THE MISSING INGREDIENTS

The following are missing in the proposed charter amendments:

1. No provision for an independent external auditor aside from the Commission on Audit (CoA). This is an important governance element if the goal is to attract local and foreign investors and strategic partners. This provision for a third-party independent external auditor (on top of the CoA audit) was incorporated in the House version and RA 11954 creating the Maharlika Investment Fund. (Thank you, Congressman Joey Salceda for adopting this suggested amendment to the bill.)

2. No clear provision for the timely filing of audited financial statements (AFS) with the local stock exchange. A third-party external auditor would improve this timeline significantly towards global standards. The best practice under the ASEAN Corporate Governance Scorecard (ACGS) is to file the audited financial statement (FS) within 90 calendar days from end of the calendar year — March 1 or Feb. 29 (for leap years). In contrast, the CoA-audited FS 2023 for the DBP became available only in June 2024 while that of the LBP in September 2024 (October 2023 for the 2022 AFS). This late filing/disclosure would be unacceptable to private investors, as it would mean a very late annual stockholders’ meetings.

3. No provision for an annual stockholders’ meetings (ASM), at which the management and the board of directors report to the shareholders — with new stockholders (local and foreign, institutional and retail) — the results of the prior year and secure stockholders’ ratification for the acts of the board and management. The declaration of dividends is announced at the ASM, following an approved dividend declaration policy. The appointment of the third-party external auditor is also approved by the stockholders upon recommendation of the board and its audit committee.

This is what Foundation for Economic Freedom President Calixto “Toti” Chikiamco meant in his statement supporting the announced IPO that “apart from strengthening their balance sheets, being publicly listed will help in bank governance as the boards and managements must answer not only to the government but also to private investors.”

Even if all the building blocks for an IPO are in place, will the shares of the LBP and the DBP be attractive to investors? The short answer is NOT AT THE PRESENT TIME.

1. Investors expect an IPO company to have a track record of consistent and solid returns which underpins their expectations of dividends and stock price appreciation. Both GFIs need several years to establish this track record. They also need to get past the historical narrative of having to request for regulatory relief and dividend relief, and having been receptacles for “behest” loans in the past.

2. Market conditions not favorable. As of the end of December 2023. only three banks listed in the Philippine Stock Exchange have share prices above book value — Banco de Oro, Bank of the Philippine Islands, and China Banking Corp.(disclosure: this writer was head of investor relations for China Bank for 27.5 years until retirement three years ago). The rest of the listed banks are trading below book despite delivering return on equity of 15-16% in the previous few years.

In conclusion: the proposed charter amendments are steps in the right direction, but a few crucial elements are still missing. Once enacted, the revised charters (hopefully revised to fill in the “missing ingredients”) will be a good foundation for a successful IPO. The increase in paid-in capital has to happen first, which will boost their capacity to perform at a higher trajectory. Thereafter, a good track record and favorable market conditions augur well for a successful IPO.

Alexander C. Escucha is president of the Institute for Development and Econometric Analysis, Inc. (IDEA), and chairman of the UP Visayas Foundation, Inc. He is a fellow of the Foundation for Economic Freedom and a past president of the Philippine Economic Society. He is an international resource director of The Asian Banker (Singapore).

alex.escucha@gmail.com