Big banks’ asset growth returns to pre-pandemic level in second quarter

By Abigail Marie P. Yraola, Researcher

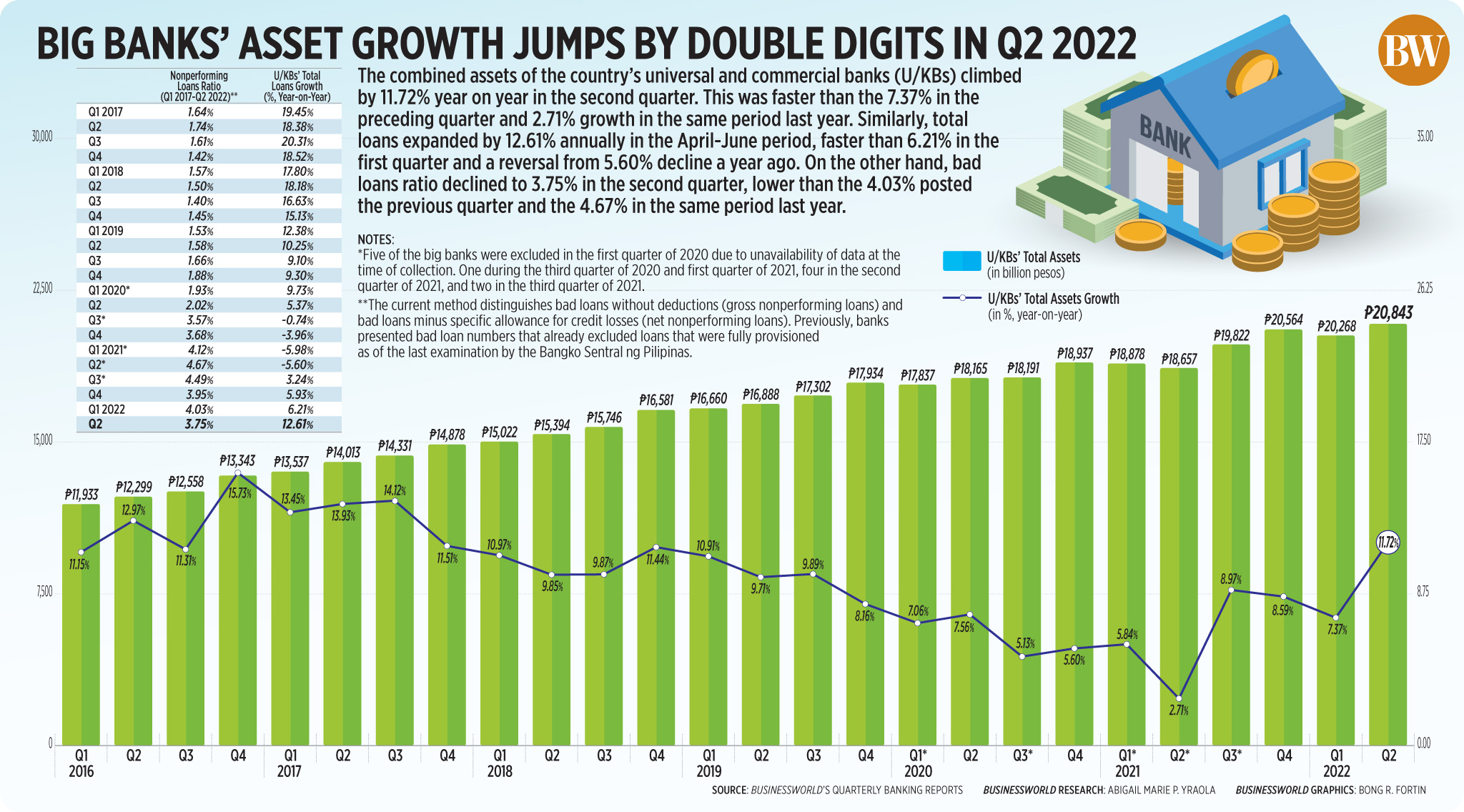

THE COMBINED ASSETS of the Philippines’ largest banks grew by double digits annually in the second quarter, a pace not seen since before the pandemic, due to an increase in total loans.

The latest edition of BusinessWorld’s Quarterly Banking Report showed the total assets of the 45 universal and commercial banks (U/KBs) in the country jumped by 11.7% year on year to P20.84 trillion in the April to June period.

This was higher than the P20.27 trillion seen in the first quarter of 2022 and the P18.66 trillion recorded in same period in 2021.

The latest asset growth was the fastest in 19 quarters or since the 14.1% growth in the third quarter of 2017.

The big banks’ combined loans, which account for bulk of their total assets, rose by 12.6% year on year to P10.39 trillion in the second quarter, faster than the 6.2% growth seen in the preceding quarter.

This was a turnaround from the 5.6% year-on-year decline in April-June period last year.

The latest reading marked the quickest loan expansion in 14 quarters, or since the 15.1.% recorded in the last quarter of 2018.

The median return on equity (RoE), which is an indicator of profitability, rose to 5.56% in the second quarter, higher than the 3.96% in the first quarter and the 2.77% RoE in the same period a year ago.

The RoE, or the ratio of net profit to average capital, measures the amount that shareholders make on their investments in a company.

Meanwhile, bad loans, also known as nonperforming loans (NPLs), reached P356.75 billion in the second quarter, lower by 9.6% from P394.63 billion in the first quarter and down by 8.3% from P389.16 billion in the same period a year ago.

This brought the NPL ratio — the share of soured loans to the total loan portfolio — to 3.75% in the April to June period, improving from 4.03% in the preceding quarter and from 4.67% in the second quarter of 2021.

Loans are considered to be nonperforming if any principal and/or interest are left unpaid for more than 90 days from the contractual due date or accrued interests for more than 90 days have been capitalized, refinanced, or delayed by agreement.

The U/KBs’ nonperforming asset (NPA) ratio — the NPLs and foreclosed properties in proportion to total assets — stood at 1.17%, lower than the previous quarter’s 1.31% and the 1.46% in the second quarter last year.

Relative to total assets, foreclosed real and other properties stood at 0.28%, inching up from 0.26% in the preceding quarter and the second quarter of 2021.

Total loan loss reserves stood at P366.14 billion during the April to June period, higher than the previous quarter’s P363.56 billion and P338.54 billion a year ago.

The big banks’ median capital adequacy ratio — the lenders’ ability to absorb losses from risk-weighted assets — eased to 20.91%. This was lower than 21.73% in the first quarter and 22.34% in the second quarter of 2021.

Still, the ratio remained well above the regulatory minimum of 10% set by the Bangko Sentral ng Pilipinas as well as the international minimum standard of 8%.

BDO Unibank, Inc. remained the largest bank in terms of total assets with P3.75 trillion in the second quarter. It was followed by Land Bank of the Philippines (LANDBANK) with P2.82 trillion, and Metropolitan Bank & Trust Co. (Metrobank) with P2.71 trillion.

The merger of the United Coconut Planters Bank and LANDBANK became effective on March 1.

BDO also led the banks with P2.37 trillion worth of loans issued, followed by Bank of the Philippine Islands (BPI) with P1.55 trillion and Metrobank with P1.25 trillion.

In terms of deposits, BDO also ranked first with P2.96 trillion, followed by LANDBANK with P2.47 trillion and Metrobank with P2.06 trillion.

Among banks with assets of at least P100 billion, Rizal Commercial Banking Corp. recorded the fastest year-on-year growth with 22.47%. This was followed by UnionBank of the Philippines (19.25%), and China Banking Corp. (19.18%).

Meanwhile, Bank of Commerce was the most aggressive lender in the second quarter with an annual increase of 47.41%, followed by LANDBANK’s 29.10% and The Hongkong & Shanghai Banking Corp. Ltd.’s 26.66%.

BusinessWorld Research has been tracking the financial performance of the country’s biggest banks on a quarterly basis since the late 1980s using banks’ published statements of condition.