Vision 2030: How can the Philippines boost growth and competitiveness?

By Jomarc Angelo M. Corpuz, Special Features and Content Writer

The Philippine economy has found its footing once again after experiencing sudden lows caused by the coronavirus disease 2019 (COVID-19) pandemic. After marking the country’s steepest annual gross domestic product (GDP) decline of 9.5% in 2020, the country has recovered and expanded consistently, posting GDP growth rates above 5.5% in each of the last four years.

However, experts suggest that the next five years leading up to 2030 may become even more critical for the Philippines to secure its place as a globally competitive economy. Amidst talks about the country becoming a high-income economy, the focus now shifts to the administration and its policy makers, along with their strategies to steer clear of the so-called middle-income trap plaguing nations unable to transition around the world.

Access to capital, policy reforms, workforce preparedness, and other ways to accelerate the Philippines’ growth and avoid pitfalls were discussed for the fourth panel discussion at the BusinessWorld Economic Forum on May 22 at the Grand Hyatt Manila.

Discussing “Vision 2030: Accelerating The Nation’s Competitiveness Toward Economic Success,” experts for the final panel discussion included Management Association of the Philippines (MAP) President Alfredo S. Panlilio, BDO Capital President Eduardo V. Francisco, and Philippine Chamber of Commerce and Industry (PCCI) Secretary-General Ruben J. Pascual, with Cignal TV News Anchor Dr. Danie Laurel as moderator.

For his opening statement, Mr. Panlilio spoke about the critical hurdles the Philippines must overcome to fulfill its “Vision 2030,” a term he used to describe a future where every Filipino enjoys a life that’s secure, comfortable, and full of opportunity.

Among the challenges he pointed out were the lack of innovation-driven growth, which he said is key to global competitiveness as nnovation empowers businesses and startups as well as encourages productivity. Mr. Panlilio also mentioned the lack of investments in human capital, which can be done by equipping Filipinos with future-ready skills and improving educational systems. Equally important, he advocated for the fostering of a robust digital infrastructure to boost the efficiency and accessibility of services across all sectors.

“Let us build upon our strengths and create a thriving economy that is sustainable, inclusive, and resilient. Together, we can unlock the full potential of our nation for the benefit of the Filipino people,” he said.

Similarly, Mr. Francisco echoed Mr. Panlilio’s statement on the need for improvement in the country’s human capital, stating that the standards of graduates in colleges have gone down due to automatic passing grades. Other topics the BDO Capital executive discussed in his opening statement include the need to simplify bureaucratic processes in starting businesses and building infrastructures, as well as the projects in several sectors that BDO Capital has been conducting in partnership with the government.

“We should already be moving in the faster lane, but we still can’t get ourselves into the fourth gear or the fifth gear. We’re still on first and second; and hopefully, we can do something [right] there to help businesses and the economy,” Mr. Francisco said.

Mr. Pascual, for his part, noted the problems that each government, since the Arroyo administration, missed and what Ferdinand R. Marcos, Jr. continues to miss during his term as president.

The first of these is poverty and income inequality. The PCCI official noted that despite campaign promises aimed at addressing the issue, the Philippines is still plagued with infrastructure deficiencies, financing gaps, and bureaucratic delays.

Fiscal irresponsibility is another problem, Mr. Pascual mentioned, pointing out that unchecked government spending and inefficient allocation of resources. He also mentioned the failure of improving agriculture, noting issues with shortages of rice and high prices of goods.

The neglect of human capital development, he continued, is reflected by a big skills mismatch compared to what industries actually need. Mr. Pascual also noted the decline of industries in the manufacturing sector and the loss of opportunities to neighboring countries.

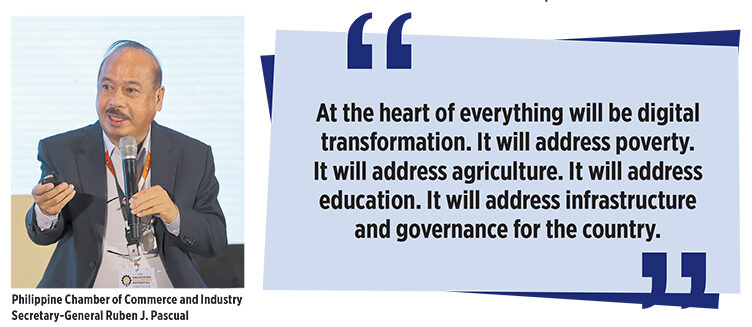

“At the heart of everything will be digital transformation. It will address poverty. It will address agriculture. It will address education. It will address infrastructure and governance for the country,” Mr. Pascual advocated during his speech.

A major point of discussion during the panel discussion is how the Philippines can leverage its demographic dividend to address the talent deficit in its human capital. With a young and growing population, the country has a unique opportunity to build a future-ready workforce — but only if strategic investments are made in education, skills training, and job creation.

PCCI’s Mr. Pascual emphasized the need for the government to improve basic education and begin focusing on science, technology and math, much like replicating or optimizing the Philippine Science High School system. For the private sector, he suggested emulating efforts from neighboring countries that have constantly upskilled their workers and generated workers ready for modern jobs.

Meanwhile, MAP’s Mr. Panlilio spoke about the need to adapt to technology by upskilling workers in the business process outsourcing and manufacturing industry. He also encouraged the use of automation and artificial intelligence to adapt to what the world will need.

“Everything goes back to technology. Technology’s evolution is just so quick, and we need to continue to adapt. It’s even affecting private companies. We’re all in various stages of that spectrum. Some of us are more advanced; some not. These are the things that we should invest more in,” Mr. Panlilio said.

On the other hand, BDO Capital’s Mr. Francisco expressed his dismay at the new graduates colleges are producing, citing his observations of the hiring process in companies where the basic requirements are almost down to having the ability to read and write. He posited that sometimes he just hires people with a basic understanding and intelligence in the hopes of retraining them.

Another concern the panel delved into is the need to improve digital infrastructure and whether the country can truly be considered a “digital hub.” While the Philippines has made strides in digital adoption and boasts a strong online presence through its young, tech-savvy population, the panelist noted that significant challenges remain.

“If you talk about broadband, cables, etc., telcos have done a lot; and even in far-flung areas, you can have internet. The next step to that is digitalizing your systems — computerizing. That is harder because those are not off-the-shelf packages anymore. Maybe large corporations can do that, but the MSMEs (micro, small, and medium enterprises) cannot. So, maybe that’s where we need to focus on,” Mr. Panlilio said.

Conversely, Mr. Francisco revealed the efforts that telco companies are making to improve connectivity in the country, while also acknowledging the financial and competitive challenges they face in expanding digital infrastructure. He noted that despite covering 97% of the country through wireless networks and ongoing investments in data centers, telcos struggle to further invest due to rising costs and limited flexibility in pricing.

“I think there’s a push to make the country a digital hub. But it can’t just be pushed by the private sector. It is a country setting, like what the government did for BPOs (business process outsourcing companies) before. You have to go out there and market the country, and say that we are well-positioned to be one,” Mr. Francisco added.

One of the most frequently raised concerns is how to attract more investors to the country to make Vision 2030 a reality. In this regard, Mr. Pascual reiterated some of the biggest concerns faced by investors who may want to invest in the country.

“Some are really very basic. One is energy; our cost is really too high. Second is the inconsistent economic policies that the past governments have been implementing and that have created insecurities among investors. Third is the way we do business, which is a big question for us,” he said.

Unlocking the Philippines’ potential and paving the path toward becoming a high-income economy by 2030 demands urgent and decisive action. While ambitious, with the right investments in people, infrastructure, technology, and governance, Vision 2030 can become the Philippines’ next great leap forward.