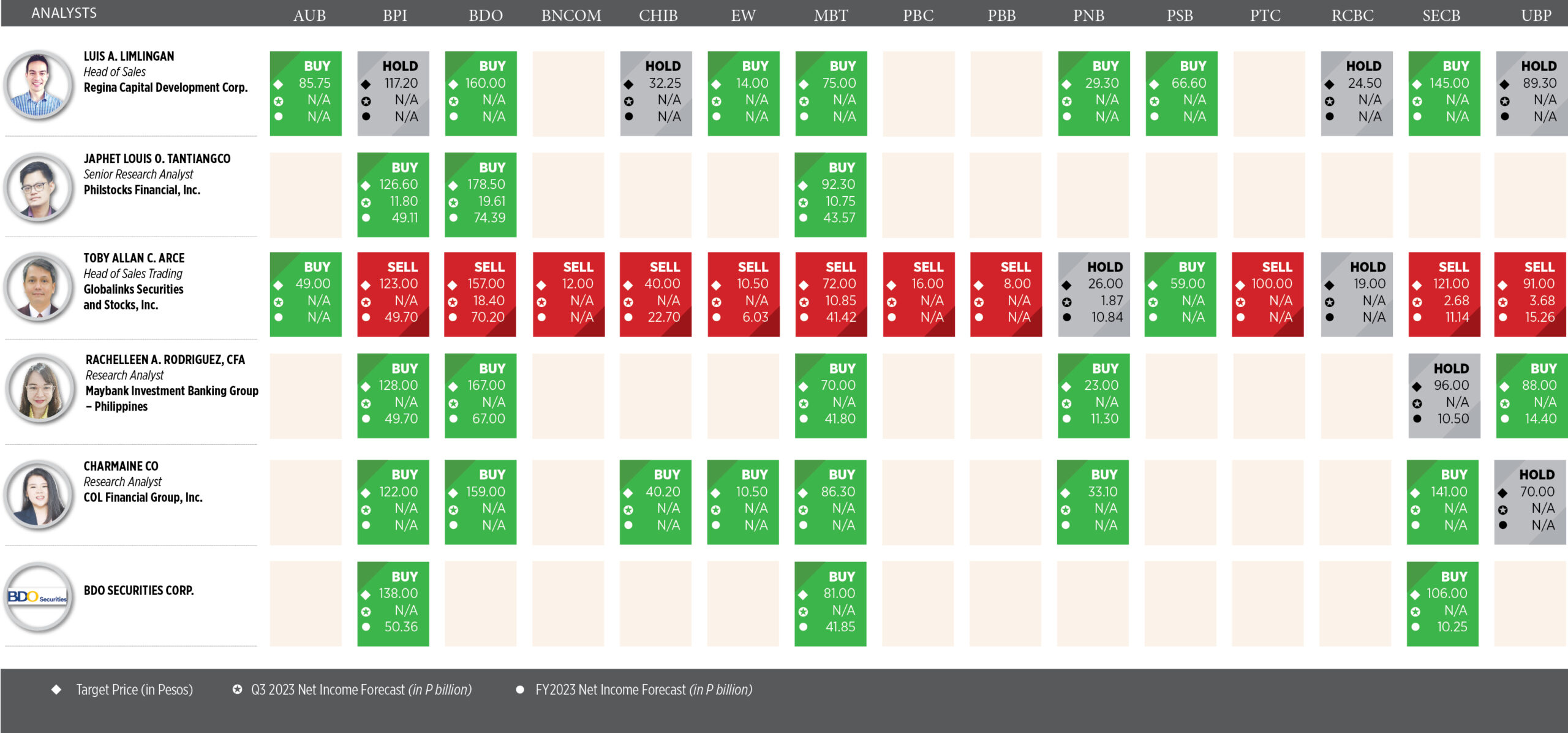

Analysts remain bullish on banks

By Lourdes O. Pilar, Researcher

THE listed banks are seen to improve further for the rest of the year, bolstered by high interest rates that could pad their margins, even as their share prices disappointed in the second quarter, analysts said.

Analysts noted the better performance of banks in the second quarter due to higher earnings driven by strong bank lending coupled with interest rates.

The Philippine Stock Exchange index lost 0.5% on a quarter-on-quarter basis, slower than the 1% decline posted in the first quarter and last year’s 5.1%.

Meanwhile, the financials subindex, which included the banks, eased 2% quarter on quarter at the end of the April-June period versus the 10.1% growth recorded in the first quarter. This was lower than the 28.1% recorded at the end of last year’s second quarter.

Most of the banks’ stock performance fell in the second quarter except Asia United Bank (AUB, up 9.8%), BDO Unibank, Inc. (BDO, up 7.2%), Philippine Bank of Communications (PBCOM, up 6.3%), and Bank of the Philippine Islands (BPI, up 6.1%).

Leading the decliners were Philippine Business Bank (PBB, down 23.1% quarter on quarter), Bank of Commerce (BNCOM, down 14.5%), and Union Bank of the Philippines (UBP, down 11.9%).

Meanwhile, aggregate net income of universal and commercial banks went up by 28.9% to P169.92 billion as of end-June from P131.82 billion last year, data from the Bangko Sentral ng Pilipinas (BSP) showed.

Gross total loan portfolio of these big lenders rose by 8.1% to P11.84 trillion as of end-June from P10.96 trillion a year ago.

The big banks’ gross nonperforming loans (NPL) ratio also improved to 3.13% in June from 3.25% in June last year.

The big banks’ net income margin (NIM) — a ratio that measures banks’ efficiency in investing their funds by dividing annualized net interest income to average earning asset — grew to 3.73% in the second quarter from 3.29% NIM recorded in the same period last year.

“The BSP’s action to the United States Federal Reserve’s movement was the primary factor that influenced the banks’ performance,” Regina Capital Development Corp. Head of Sales Luis A. Limlingan said in an e-mail.

“Strong economic growth of the Philippines has helped in buoying the public’s confidence to seek out bank financing, whether it be for business or personal use,” Mr. Limlingan added.

The BSP’s Monetary Board has already kept the policy rates steady for four straight meetings. Target reverse repurchase rate currently stands at 6.25%. Overnight deposit and lending rates are also maintained at 5.75% and 6.75%, respectively.

Meanwhile, the US Fed in September held its interest rates steady between the 5.25% and 5.5% range in its bid to tame inflation while not denting its economic growth.

“Majority of the banks also exhibited higher net income margin (NIM) as of end second quarter of 2023 implying that they were able to make more out of their earning assets. The financial index banks’ average NIM stood at 4.25%, higher than the 3.94% in the same period last year,” Japhet Louis O. Tantiangco, senior research analyst at Philstocks Financial, Inc., said in an e-mail.

Charmaine Co, research analyst at COL Financial Group, Inc., said in a separate e-mail: “The banking sector’s net interest income grew by 24.5% year on year in the second quarter as all banks reported higher lending income. This was mainly due to expansion in the banks’ loan portfolios.”

Rastine Mackie D. Mercado, research director at China Bank Securities Corp., said that the financial results of listed banks were generally strong, as cumulative rate hikes and the full resumption of business and consumer activities underpinned business expansion.

“Year on year, the twin tailwinds from expanding earnings assets and higher NIMs mainly supported lending income growth. Similarly, the uptick in loan volumes, coupled with the full restoration of mobility also supported the year-on-year expansion in fee incomes,” Mr. Mercado said in an e-mail.

BDO Securities Corp. said in an e-mail that growing economic activity, increasing mobility, as well as improving business and household incomes continue to support loan demand.

“We also note that the growth of higher-margin consumer loans (credit cards, auto loans, home loans) continue to outpace that of corporate loans, which help in propping up overall loan yields,” BDO Securities said.

For her part, Rachelleen A. Rodriguez, research analyst at Maybank Investment Banking Group-Philippines, said that the listed banks’ price performance was impacted largely by overall stock liquidity and earnings performance.

BANK STOCK PICKS

Analysts said that investors should pick those banks showing strong income growth, their loan portfolio composition, and their ability to roll with high interest rates.

Philstocks’ Mr. Tantiangco said investors may look for developments first that would bring our economy back to its strong growth momentum.

“Investors are also expected to monitor our bank lending data as well as the upcoming policy decisions of the BSP. With the current economic challenges, investors would want to see if borrowers can still absorb the current interest rate levels so as to keep bank lending growing,” he said.

Mr. Limlingan of Regina Capital said that investors should always consider the loan portfolio composition of the banks they are eyeing to get into position.

“As much as possible, try to filter out those names that are overly exposed to industries that are likely to be remained challenged by a high interest rate environment and how conservative the banks are in extending loans to such industries,” Mr. Limlingan said.

“Investors tend to favor banks with more pricing power as this would eventually lead to NIM preservation, especially since the market is expecting the BSP to start cutting policy rates by 2024. They are also wary of any asset quality concerns; hence, they favor banks with high NPL buffers,” Maybank’s Ms. Rodriguez said.

OUTLOOK

The listed lenders’ performance would be dependent on how effectively they could strike a balance between expanding their loan portfolio and keeping their asset quality in check, Mr. Limlingan said.

Mr. Tantiangco said the banks’ performance in the latter half of the year would be largely dependent on the overall growth of the Philippine economy.

“If the local economy continues to grow slowly, then this may temper our listed banks’ lending operations. On the other hand, if the local economy’s growth re-accelerates, then this is seen to boost bank lending,” he said.

For BDO Securities, it expects the banks’ loan books to move at the same pace of the Philippine economy, margin improvements to continue from the delayed effects of the BSP rate hikes, and the provisioning costs to decline as NPLs stabilize in the near term.

The Philippine banking industry will perform well for the rest of 2023 despite the high interest rate environment which is seen to benefit the NIMs of the lenders, said Toby Allan C. Arce, head of sales trading at Globalinks Securities and Stocks, Inc.

“The Philippine banking sector has strong capital buffers, which will help them withstand any shocks to the economy. However, any upside risk to inflation could dampen economic growth and hurt bank profitability,” said Mr. Arce in an e-mail.