Follow us on Spotify BusinessWorld B-Side

The Maharlika Investment Fund (MIF) is plagued by problems including bad timing, unfulfilled requirements, and governance red flags, according to economist and Action for Economic Reform convener Filomeno S. Sta. Ana III. “Right now, there’s a lot of volatility, so even if we have some level of comfort with our foreign exchange reserves, we must still build our reserves,” he tells BusinessWorld report Brontë H. Lacsamana in this B-Side episode.

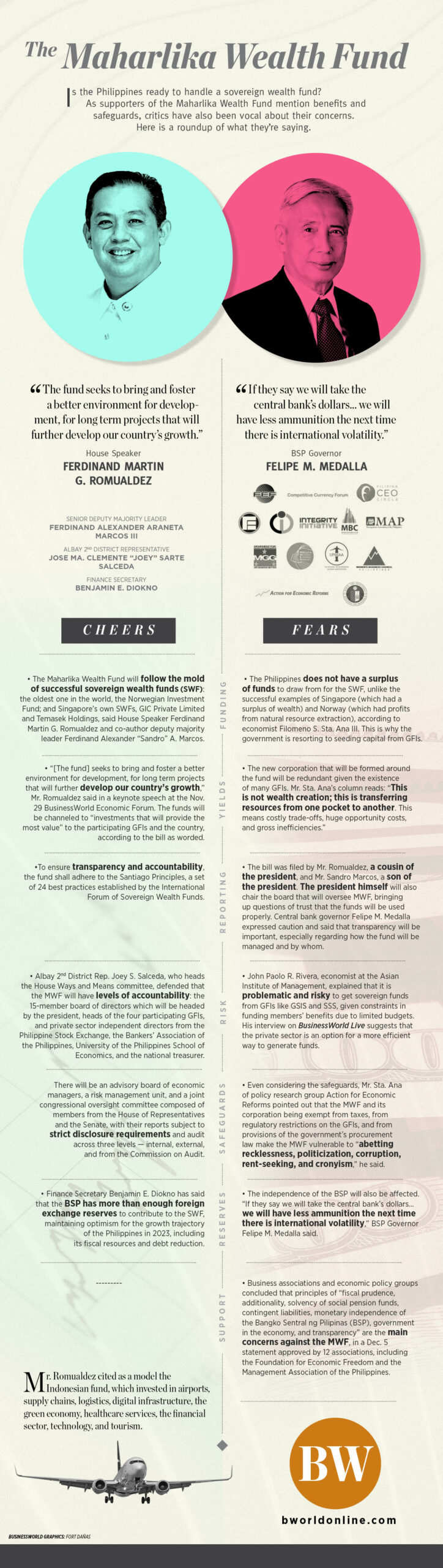

TAKEAWAYS

The Philippines doesn’t have surplus funds needed for a sovereign wealth fund.

Although the two major pension funds, the Government Service Insurance System (GSIS) and the Social Security System (SSS), have been withdrawn as sources of seed money for the MIF, the central problem of the fund remains.

“For a sovereign wealth fund (SWF) to exist, an essential feature is that the sovereign or the country has a huge surplus or an excess, resulting from mineral resources, booming extractive industries, or strong export performance,” Mr. Sta. Ana explained.

“The question is, does the Philippines have excess? The answer is no,” he said.

Despite the country’s foreign exchange reserves being relatively comfortable at the moment, the level is still insignificant compared to countries with bigger reserves.

There are other tools that can be used to increase financing.

Since legislation has since been altered to remove GSIS and SSS as sources for funding, Bangko Sentral ng Pilipinas (BSP) has been designated as the main source.

Mr. Sta. Ana said that the MIF merely transfers resources from one pocket to another: “The problem is, these are institutions that don’t have excess either. They might have surpluses but these are intended for other purposes.”

BSP’s reserves must be built because of the volatility in the present environment. Meanwhile, its profits are already being translated into dividends for the national government, with or without the BSP’s explicit participation.

Optimizing existing government corporations’ ability to grow money, following a fiscal consolidation program, and borrowing can be alternatives for pooling funds, he said.

Bad provisions for regulatory oversight open up issues of trust and corruption.

Because the bill was formatted with bad provisions, specifically exempting the Maharlika corporation from being under the oversight of the body that deals with government-owned corporations, problems of trust and corruption have been created.

The government’s past mistakes when it comes to transparency also give rise to feelings of mistrust regarding the MIF.

“We just cannot avoid being suspicious. It is understandable for people to think that something is going to happen … that this is going to be a vehicle for another Pharmally, but a Pharmally that is much, much bigger,” said Mr. Sta. Ana.

Recorded remotely on Dec. 5, 2022. Produced by Joseph Emmanuel L. Garcia and Sam L. Marcelo.