Global energy Trumpflation and the rising budget deficit

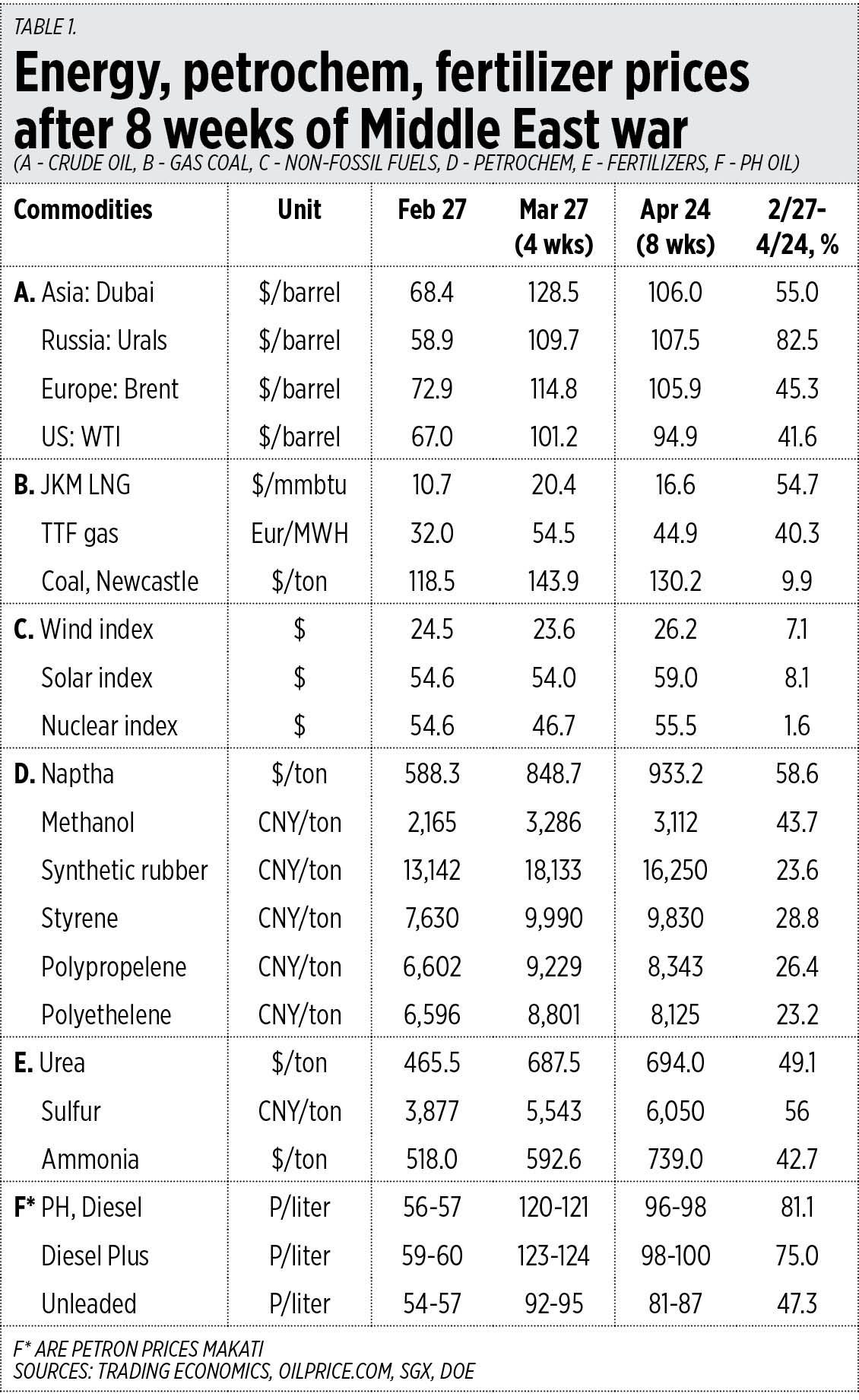

It has been two months now since the US and Israel attacked Iran on Feb. 28. So I reviewed the prices of energy and related products since the Middle East crisis started and here are the trends.

1. Crude oil prices peaked in late March then pulled back slightly, though they mostly stayed above $100 a barrel. The world is suffering from “Trumpflation” as a result of US President Donald Trump’s irresponsible and prolonged attacks on Iran and Iran’s counterattacks and choking of the Hormuz Strait.

2. The Japan Korea Marker (JKM) LNG prices are 55% higher than they were before the war but the price of coal has increased by only 10%. Indonesia and Australia, the main sources of coal in the Asia-Pacific region, are far from the conflict area.

3. Non-fossil fuels remain generally as “non-alternatives” to hydrocarbons.

4. The prices of naptha — the main feedstock for various petrochemical products — and fertilizer inputs remain high, which explains point No. 3, since solar, wind, biomass, and nuclear power cannot produce petrochem products.

5. The local pump prices have reflected price changes in global crude oil (see Table 1).

The Philippines’ inflation rate increased year on year from 1.8% in March 2025 to 4.1% in March 2026. Among the major drivers of the inflation increase this year are Transport, prices of which increased 9.9%, and Electricity, Gas and Other Fuels that increased 7.2%.

What this shows is that our local power generation companies (gencos), especially those with coal plants that contribute 57-60% of total electricity production, were able to rein in the rise in electricity prices. Among these gencos which use considerable coal power are Aboitiz Power, Meralco PowerGen (MGEN), and SMC.

CASH AND DEBT

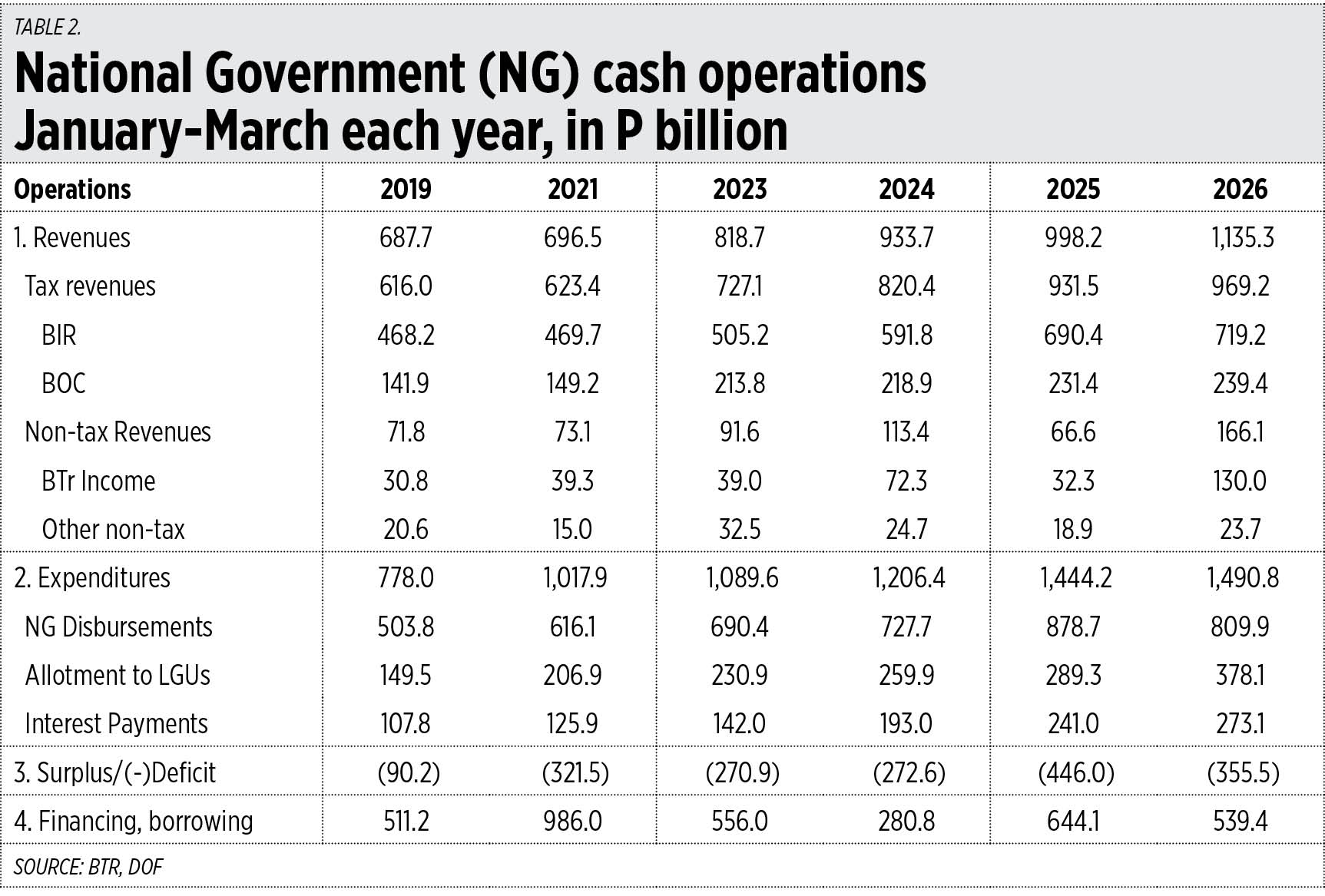

Last week, the Bureau of the Treasury (BTr) released the cash operations report for March 2026. We saw in it that the budget deficit was horrible at P350 billion in March alone as expenditures kicked high. So, I compared the January-March data over recent years and saw that the budget deficit this year of P356 billion is actually lower than last year’s P446 billion.

But given our continuously rising public debt level, our interest payment is high — P273 billion this year or an average of P3 billion/day, from P2.7 billion/day in 2025, P2.1 billion/day in 2024, P1.6 billion/day in 2023, and P1.2 billion/day in 2019 (see Table 2).

With the above data, the government and private sector should consider these short- to long-term measures.

1. Expand and accelerate exploration and development of more fossil fuels, more oil, gas, and coal instead of accelerating the development of wind and solar power. Even the resin, components of fiberglass and other parts of wind and solar power set-ups, are petrochem products.

2. Create new government subsidies and freebies or ayuda for the poor without resorting to more borrowing by cutting or shrinking some old and existing subsidies. Giving higher subsidies without cutting old subsidies means more borrowing that will require higher interest payments today and higher taxes tomorrow.

3. Suspend the excise tax on diesel and gasoline and discontinue cash aid for public transport and other subsidies. Tractors, harvesters, trucks, irrigation pumps, and fishing boats all use diesel so by suspending the excise tax there will be a decline in the cost of farming and fishing, contributing to lower food inflation.

4. Consider cutting or suspending irrigation subsidies made through the National Irrigation Administration’s big budget, instead of bowing to lobbying to give a fertilizer subsidy given the high prices of ammonia, urea, and sulfur, which are important inputs and fertilizer products.

5. On proposals to revive the domestic petrochemical industry through subsidies — the government should not rush towards this “industrial policy” lobby.

On the last point, I briefly chatted with Arnel Santos, a former Shell petrochemical executive and now COO of MGEN Thermal, and he said that “Base petrochemical investments that depend on imported feedstock and export markets remain structurally disadvantaged. Integration across refining and petrochemicals is only viable when it is connected to a system that provides access to feedstock, markets, and capital beyond what is available locally.”

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an internationa fellow of the Tholos Foundation.