State of the world, state of the nation

This paper will expand my hypothesis that I mentioned last week — that Europe and North America will deindustrialize in the short- to medium-term and many companies there will migrate to Asia. The Philippines should prepare for this.

DEGROWTH AND BLACKOUT ECONOMICS

I encountered for the first time the concept of Degrowth economics from these articles:

1. “Climate Change Modeling of ‘Degrowth’ Scenarios — Reduction in GDP, Energy and Material Use” by University of Sydney, scitechdaily.com, May 11, 2021;

2. “1.5°C degrowth scenarios suggest the need for new mitigation pathways” by Lorenz T. Keyßer and Manfred Lenzen, nature.com, May 11, 2021;

3. “Degrowth: Universities Push Permanent Poverty as the Solution to Climate Change” by Eric Worrall, wattsupwiththat.com, May 13, 2021.

To argue for reduced production of material goods and services to “save the planet” is irresponsible and insane, and the idea comes from the academe.

Then when there were frequent yellow-red alerts in the Philippines in May-June 2021, and electricity prices in Europe started rising due to less windy and more cloudy condition and thin reserves in July 2021 onwards, I started writing about “Blackout economics” in this column in BusinessWorld: “Ten indicators of blackout economics” (June 14, 2021), “Blackout economics, COP26 and Negros’ power prices” (Nov. 15, 2021), “Europe’s blackout economics and the Philippines’ path to brownouts” (Dec. 27, 2021).

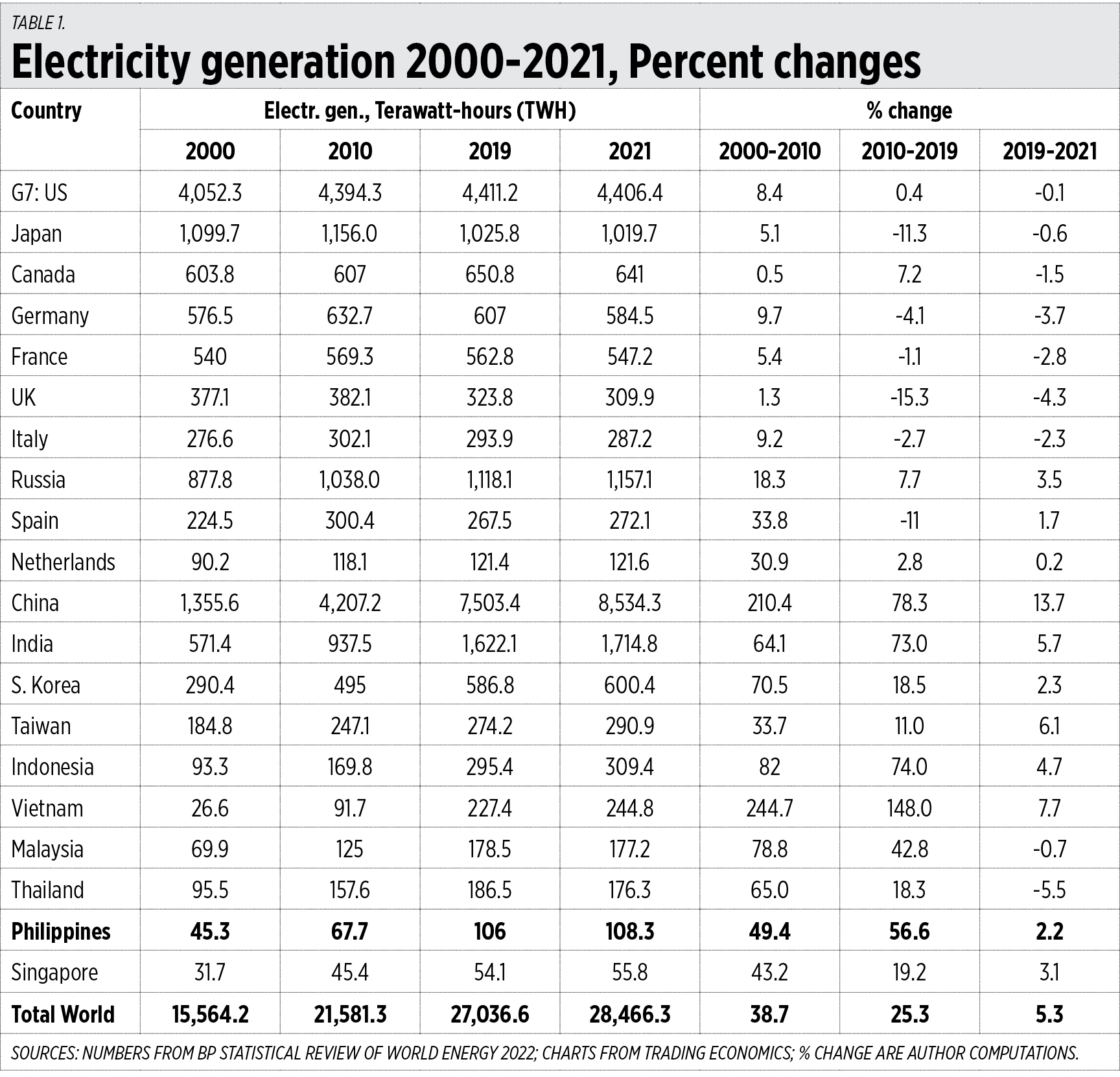

EUROPE DECLINING POWER GENERATION

Energy is development. Insufficient and unstable energy supply means slow and unsustained growth, higher power and consumer prices. Meanwhile, a high and stable electricity supply means there is a high capacity for power-intensive manufacturing, malls, residential and office condos and villages, hospitals, etc. to keep humming and producing various goods and services 24/7.

The Group of Seven (G7) industrialized countries of the world are in the forefront of “decarbonization” and “net zero” campaigns to fight “man-made” climate change. They do not believe that there is natural and cyclical climate change. The last two decades showed a drastic reduction in power generation of G7, also in two other big European countries with a GDP size of at least $1 trillion, Spain and Netherlands.

East and South Asia, excluding Japan, just paid lip-service to “decarbonization” and went on to make huge increases in power generation, based mainly on fossil fuels, especially China, India, Vietnam, and Indonesia. Russia took the East Asian path, though at a slower pace. Overall global power generation saw continued growth in energy production (Table 1).

The G7 and other European countries have a sustained belief in climate and energy alarmism. This will lead them to a path of deindustrialization.

STATE OF THE WORLD IN INFLATION AND GROWTH

Industrialized countries by default have low inflation because their technological advancement means they can mass produce many things, and have efficient storage and transportation logistics for a huge volume of goods 24/7. Thus, the average inflation rate from 1990-2010 were: Italy 3.1%, the UK 2.7%, the US 2.6%, Canada 2.1%, Germany 2%, France 1.8%, and Japan 0.4%.

Insufficient power generation and expensive electricity relative to their high industrial and commercial demand contributed to 37- to 49-years of high inflation in G7 countries except Japan. They have had anemic GDP growth over the past two decades, with 2.3% average growth already considered “very high.”

In contrast, East and South Asians that pursued high power generation would consider average growth of 3.3% as “very low” because their growth would range from 4-10% (Table 2).

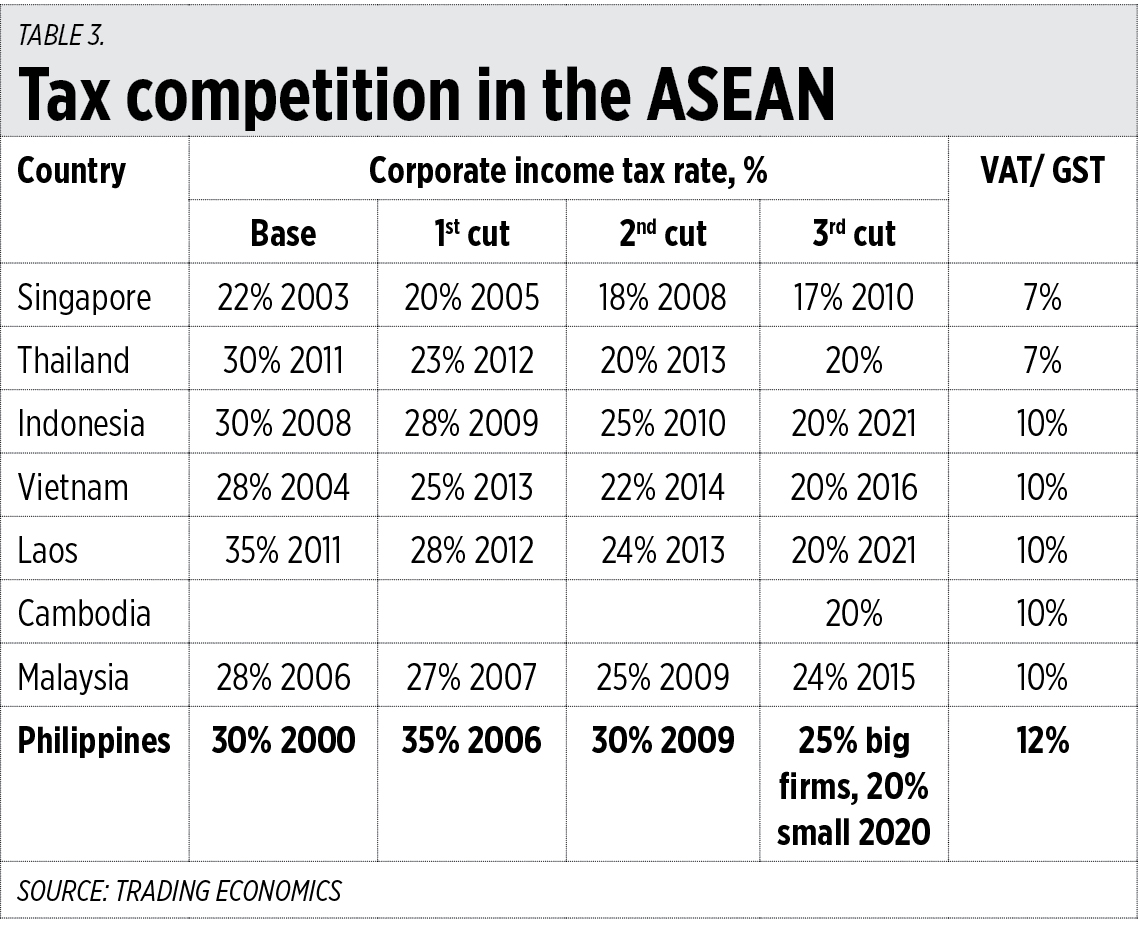

STATE OF THE NATION IN TAX COMPETITIVENESS

My view is that North America and Europe will further deteriorate economically, and are likely to experience “stagflation” or stagnant/low growth with high inflation. So, many companies there will start migrating to Asia where growth is fast, where consumers are in the billions, and where energy policies are not held fully hostage by climate alarmism.

The Philippines should continue down the path of lower tax rates and a broader tax base that can lead to stable and high revenues. The Corporate Recovery and Tax Incentives for Enterprises (CREATE) Act of 2021 (RA 11534) has reduced the corporate income tax rate from 30% to 25% for big corporations and 20% for small and medium enterprises (SMEs) with net taxable income of P5 million or lower, and total assets of P100 million or lower excluding land. This was a good move by the Duterte administration.

The next challenge would be to reduce the value-added tax (VAT) from 12% to around 10% and reduce the number of exempted sectors to have a broader tax base. We have the highest VAT or gross sales tax (GST) rate in the ASEAN and this is not good for us (Table 3).

The current strategy of Finance Secretary Benjamin Diokno of further broadening the tax base is good — I support it. Then there is the improvement in tax administration via digitalization and the taxation of many online transactions to be at par with taxation in malls, shops, and groceries. But no amount of raising revenues will be sufficient to reduce our huge public debt, outstanding and guaranteed debt — only P8.2 trillion in 2019, P12.2 trillion in 2021, and P12.9 trillion in May 2022 — unless there is corresponding fiscal discipline and cuts in expenditures or subsidies. This column will discuss more fiscal policies in future articles.

To summarize, the state of the world is there is generally more economic sanity but it is the rich, industrialized, and influential countries like G7 that lead in economic and energy irrationality. The Philippines should prepare for companies migrating from the west. The government’s economic team, local business, labor, and even civil society sectors should prepare for this.

Bienvenido S. Oplas, Jr. is the president of Minimal Government Thinkers.