BoP deficit widens to $2.3B in Sept.

THE PHILIPPINES posted its largest monthly balance of payments (BoP) deficit in four years in September, the Bangko Sentral ng Pilipinas (BSP) said on Wednesday.

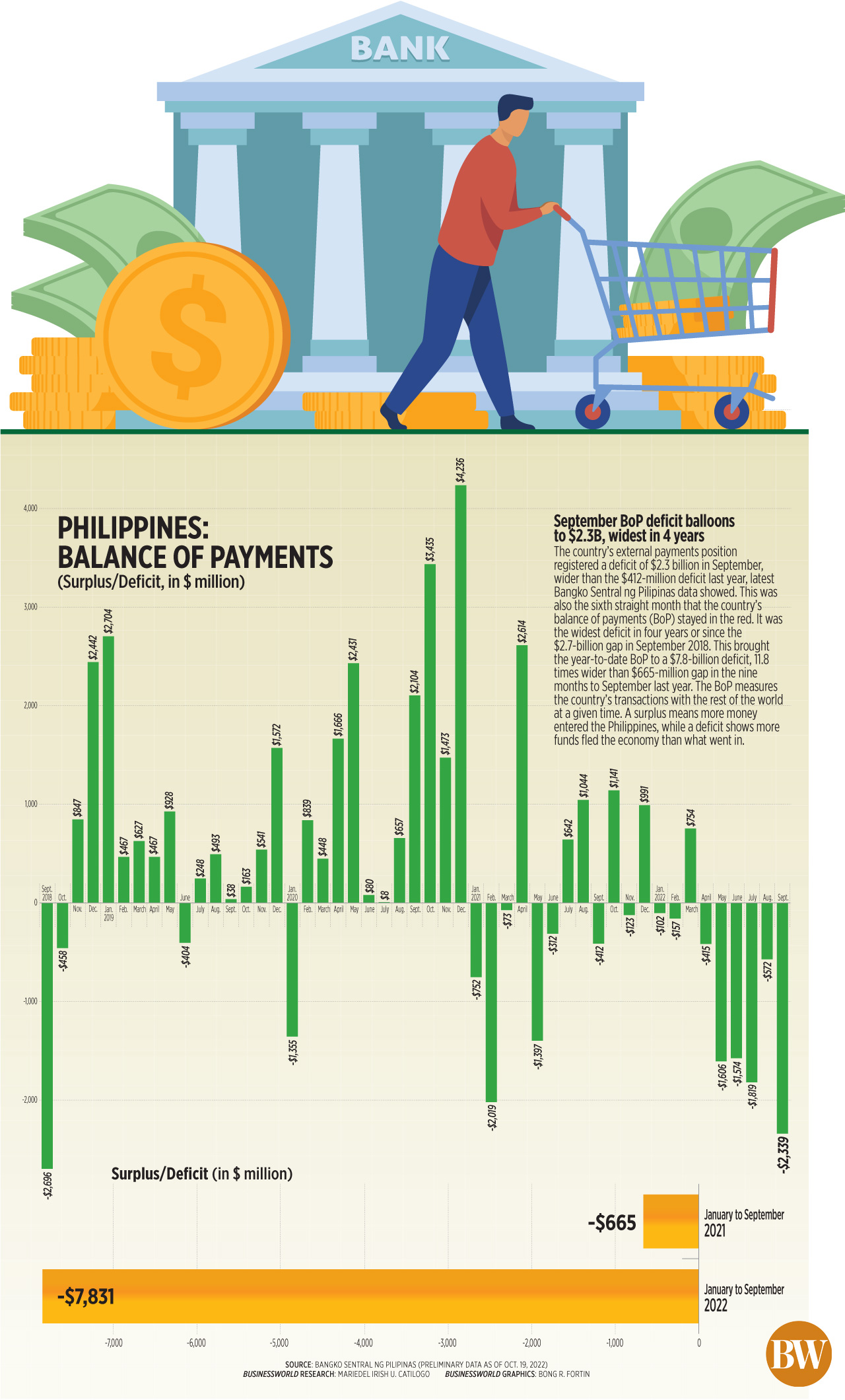

Data from the central bank showed the BoP — which is the summary of the country’s economic transactions with the rest of the world within a given period — was at a deficit of $2.3 billion in September. This is significantly wider than the $412-million gap a year ago and the $572-million gap in August.

This was the sixth straight month that the country’s BoP position was in the red. It was also the widest deficit since the $2.696 billion in September 2018.

“The BoP deficit in September 2022 reflected outflows arising mainly from the BSP’s net foreign exchange operations and the National Government’s payments of its foreign currency debt obligations,” the central bank said in a statement.

“The BoP deficit in September 2022 reflected outflows arising mainly from the BSP’s net foreign exchange operations and the National Government’s payments of its foreign currency debt obligations,” the central bank said in a statement.

In the nine months ending in September, the BoP deficit widened to $7.83 billion from $665-million deficit in the same period in 2021.

“This was to be expected as the country now runs a sizeable trade deficit,” ING Bank N.V. Manila Senior Economist Nicholas Antonio T. Mapa said in an e-mail.

“Based on preliminary data, this cumulative BoP deficit reflected the widening trade in goods deficit as goods imports continued to surpass goods exports on the back of the persistent surge in international commodity prices and resumption in domestic economic activities,” the central bank said.

The Philippines’ merchandise trade deficit hit a record $6.003 billion in August as imports continued to surge. Year to date, the trade balance ballooned to a $41.811-billion gap, wider than the $24.77-billion trade deficit in the comparable eight months last year.

“Dollar outflows (BoP) deficit suggest pressure on the peso in the near term but the silver lining is that the BSP has a sizable stash of foreign currency reserves,” Mr. Mapa said.

At its end-September position, the BoP reflected a final gross international reserve (GIR) level of $93 billion, 4.5% lower than the $97.4 billion as of end-August.

“The latest GIR level represents a more than adequate external liquidity buffer equivalent to 7.4 months’ worth of imports of goods and payments of services and primary income,” the BSP said.

The GIR can also cover up to 6.6 times the country’s short-term external debt based on original maturity and four times based on residual maturity.

An ample level of foreign exchange buffers safeguards an economy from market volatility and is an assurance of the country’s capability to pay debts in the event of an economic downturn.

“For the coming months, lower global crude oil prices near nine-month lows or since the latter part of January 2022… would help ease the trade deficit from record levels as seen in recent months amid risks of recession in the US,” Rizal Commercial Banking Corp. Chief Economist Michael L. Ricafort said in a Viber message.

“Continued growth in OFW (overseas Filipino worker) remittances and BPO (business process outsourcing) revenues, especially in (the fourth quarter) would also help offset/make up for the wider trade deficits seen in recent months,” he said.

Mr. Ricafort noted growth in structural dollar inflows such as remittances from overseas Filipinos, BPO revenues, foreign direct investments, foreign tourism receipts and others would add to the country’s BoP and the GIR.

However, surging inflation could still widen the trade deficit in the coming months, he said.

Inflation rose to 6.9% year on year in September, exceeding the central bank’s 2-4% target band for six straight months. The average inflation rate for the year so far is at 5.1%.

The BSP expects the country’s BoP position to end the year at an $8.4-billion deficit equivalent to -2% of gross domestic product amid weaker global demand.

In 2021, the Philippines posted a BoP surplus of $1.345 billion. — Keisha B. Ta-asan