Should you take chances in buying a dream home?

By Bernadette Therese M. Gadon, Researcher

ARE FILIPINOS still willing to take a chance to buy their dream home amid an economic slowdown and high inflation?

Concerns have eased as real estate demand shows no signs of slowing. Analysts noted that it is still every Filipino’s dream is to have their own homes.

To recall, the Philippines’ economic output eased for three straight quarters at 4.3% as of the second quarter as effects of the central bank’s interest rate hikes slowed consumption.

The Bangko Sentral ng Pilipinas (BSP) kept interest rates steady at 6.25% for the fourth straight meeting on Sept. 21.

Inflation picked up in August to 5.3% year on year amid higher prices of food and transport commodities. This ended the six-month easing streak since the 8.7% peak in January.

ING Bank N.V. Manila Senior Economist Nicholas Antonio T. Mapa said that the Filipinos’ experience of forced stay-at-home during the pandemic “sparked heightened interest” in real estate.

“This may have generated increased demand for more space for dwellings and/or alternative living arrangements in the event that we need to lockdown again in the future,” he said in an e-mail interview.

Analysts also attributed the demand in real estate to better labor conditions in the Philippines.

Labor Force Survey (LFS) data from the Philippine Statistics Authority (PSA) showed unemployment rate at 4.8% in July, lower than the 5.2% logged in the same month a year ago.

“The economic reopening helped bolster job creation, which is notable in the current trend we’re seeing in the labor market. With access to jobs, this helped households generate cash flow, which will make credit more accessible if households need or [is] interested in acquiring real estate,” Mr. Mapa said.

In a phone call interview, Joey Roi Bondoc, associate director of Research at Colliers Philippines, said that more employed Filipinos present a “very good backdrop” for the residential sector and investing in your home is still practical despite sky-high interest rates.

“Because in the Philippines, we don’t really have a lot of investment options and properties is one of those that over the past few years has really shown resiliency in terms of capital appreciation potential, or as a source of recurring income,” Mr. Bondoc said.

He also noted that condominium units in Metro Manila have seen a recovery in the primary market, and a rebound in the secondary market, evidence of robust demand this year.

“We are projecting a 2-3% increase in rental prices every year, that’s from 2023 up to 2025. But the problem is that’s still slow because at the height of the pandemic in 2020 to 2021, rents and prices corrected via combined 12-19%.”

Likewise, outside of the capital region, Mr. Bondoc sees sustained demand for house and lot or lots only, showing recovery in the market.

BDO Unibank, Inc.’s (BDO) Senior Vice-President and Consumer Banking Group Home Loan Business Head Angelita C. Manulat said via e-mail that historically, real estate is “one of the most stable long-term investments,” and that they expect a boost in the value of both residential and commercial properties.

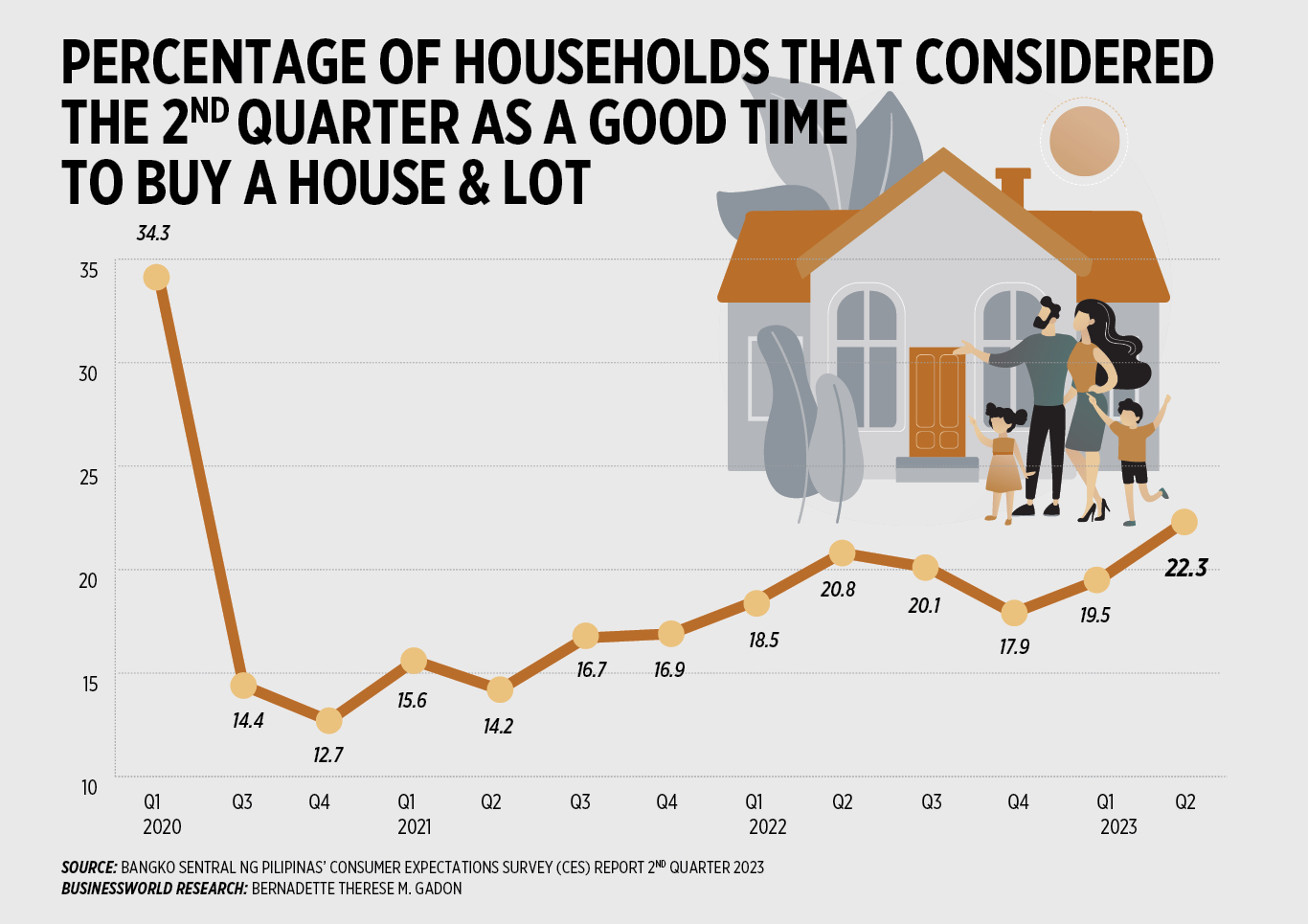

According to the BSP’s latest Consumer Expectations Survey (CES), the percentage of households that consider the second quarter as a suitable time to buy a house and lot went up to 22.3% from 19.5% in the first quarter. This was the highest share in 11 quarters or since the 34.3% recorded in the first quarter of 2020.

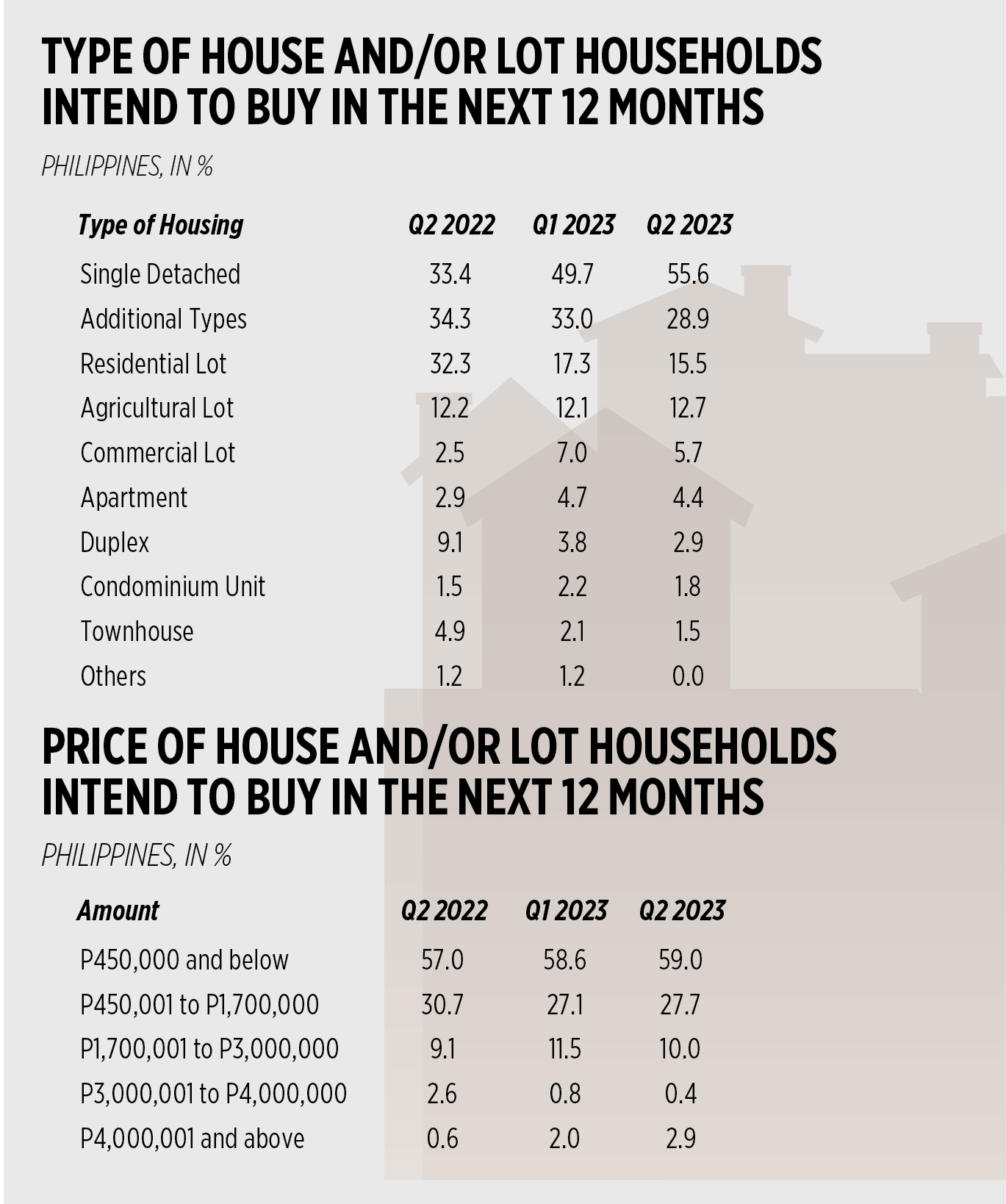

Considerations to buy a house and lot in the next 12 months rose slightly to 4.7% in the second quarter from 4.6% in the previous quarter.

By type of housing, single detached houses are still majorly considered to buy in the next 12 months by Filipinos at 55.6%, with more than half of the households consider buying a house within P450,000 and below.

In an e-mail interview, the BSP said that the universal and commercial banks (U/KBs) and thrift banks’ (TBs) real estate exposure (REE), composed of real estate loans (RELs) expanded by 5% year on year to P3 trillion as of end-March.

RELs went up by 4.6% to P2.57 trillion as of end-March, slower than the 7.3% growth in end-March last year.

Commercial real estate loans (CRELs), which is almost two-thirds of total RELs, increased by 4.6% to P1.62 trillion, slower than the 6.9% in the same period a year ago.

However, residential RELs (RRELs), which hold 36.9% share of the total, slowed by 4.6% to P950.1 billion from 8% in end-March 2022.

On the other hand, nonperforming REL ratio eased to 4.1% as of end-March 2023, lower than 4.2% in the fourth quarter last year, and 5% from the same quarter a year ago.

“The continuous growth in both CRELs and RRELs reinforces the upbeat outlook of industry experts that the property market is on its path to recovery,” the BSP said.

As of first quarter this year, residential real estate price index (RREPI) showed overall house prices picked up by 10.2% from 5.7% in the same quarter a year ago.

Single detached houses grew by 17%, a turnaround from 2.3% drop in first quarter 2022.

In a separate e-mail, Pag-IBIG Fund Deputy Chief Executive Officer for Home Lending Operations Benjamin R. Felix, Jr. said that according to their latest data, the Philippines’ housing backlog stands at 6.5 million housing units, backing the demand for housing despite trying times.

Pag-IBIG supplied stimulus packages such as special rates on its home loans, and P10 billion financing for qualified developers to address these backlogs.

“We believe that the demand for housing will always be present, as part of our culture as Filipinos is to dream of owning a home for ourselves and our families,” Mr. Felix said.

LAYING THE FOUNDATION

To entice Filipinos to finally take that step to buy their own house, Colliers’ Mr. Bondoc said that developers offer bundle promos that includes either a parking space for condominium units, or appliances for housing units, and implement various payment schemes such as extended down payments to cater to diverse Filipinos.

“The problem with banks is they have not really reduced their mortgage rates, so what we have seen is more aggressive partnerships between banks and the developers,” he said, adding that with the policy rate not declining, banks are tied at this point and could not reduce mortgage rates.

Since 2018, the BSP put in place the Uniform Loan and Mortgage Agreement and its Supplemental Terms and Conditions Templates for Real Estate Mortgages which makes comparison in different lending institutions easier for borrowers.

In addition, to aid in making these dreams come true, financial institutions have offers to make housing financially easier.

Ms. Manulat said that BDO made measures to make housing loan with them better such as providing flexible payment terms of up to 25 years for ease of payment of monthly amortizations and a built-in mortgage redemption insurance and fire insurance, payable in 12 equal monthly payments at 0%.

Additionally, BDO has light payment options, affordable cash out, and fast and easy processing for its clients.

“We take to heart our mandate to provide our members with affordable home financing. That is why Pag-IBIG Fund’s interest rates on its home loans remain low, despite the relatively high interest rates prevalent in the home mortgage industry,” Mr. Felix said.

Pag-IBIG has adapted a lower interest of 6.25% per annum under a three-year repricing period from 6.375%. Interest rate cuts have also been implemented on the five, 10-, 15-, 20-, 25-, and 30-year repricing periods to 6.5% (from 6.625%), 7.125% (from 7.375%), 7.75% (from 8%), 8.5% (from 8.625%), 9.125% (from 9.375%), and 9.75% (from 10%), respectively.

Furthermore, only Pag-IBIG offers the longest repayment term of up to 30 years, compared with the maximum 20-year loan period offered by most home mortgage entities.

“With our fiscal standing strong, we have been able to effectively fund the high demand for our home loans without the need to borrow from the market. As a result, we are able to keep our rates low,” he added.

To protect borrowers from getting buried in interests, Pag-IBIG offers interest rebates for loans paid in full before its original term, as well as adding penalties only on unpaid dues to keep missed payments affordable for members.

“Another feature that is almost always overlooked is the low insurance premiums on the Mortgage Redemption Insurance (MRI) and Fire and Allied Perils Insurance of our home loans at P0.225 for every P1,000, [which] means a P1-million loan will have a monthly insurance premium of only P225, about a quarter of the insurance fees that other financial entities charge for their loans,” Mr. Felix said.

With Pag-IBIG’s mandate to invest at least 70% of its investible funds in housing, the agency is currently on the lookout for socialized housing units to address the housing needs of minimum-wage earners and to spread housing development across all regions in the Philippines.

“This is why we continuously collaborate and create policies in consultation with housing developers, local government units, and other organizations to accelerate housing development under sustainable communities to provide homeownership opportunities for all our members, particularly in the socialized housing segment,” Mr. Felix said.

OUTLOOK

For the rest of the year, analysts are expecting the demand and recovery trend to continue for real estate despite headwinds.

“One headwind really is the interest rate. If it will remain high, then it might clip the recovery of the residential market,” Mr. Bondoc said.

It’s important to monitor interest rate policies because once the BSP cuts its policy rate, it will signal the reduction in mortgage rates, enticing more Filipinos to acquire residential units.

The effects of global economic crisis should also be monitored, Mr. Bondoc noted, as it will affect the inflow of remittances and deployment of overseas Filipino workers (OFWs).

BDO’s Ms. Manulat cautioned the sector on the impacts of natural calamities as well as it could affect pricing of properties in general.

The central bank said to keep in mind of government policies and legislation, such as tax incentives, deductions, and subsidies that could either boost or hinder demand for real estate.

Most importantly, analysts remain vigilant of the country’s economic performance in the coming months.

With the slower growth seen in the second quarter, worries of the Philippines not achieving its growth forecast of within the 6-7% range this year might dim demand in housing and could potentially spill over in 2024.

However, Pag-IBIG’s Mr. Felix is optimistic on real estate growth as overall outlook remains vibrant and institutions are ready to support housing needs.

“This is primarily due to the increase in economic activity brought about by the lifting of public health emergency, the increasing appreciation of young professionals in the value of real estate, and the demand to be driven by the 4PH Program (Pambasang Pabahay para sa Pilipino Program),” he said.

He also added that Pag-IBIG’s programs to stimulate the housing industry is a way to promote economic growth as it provides support to many industries and Filipino workers that could also empower them to secure home financing.

“And while we own more than a third of the share of the total home mortgages in the country, we need the active and strong participation of financial entities and banks to address the home financing needs of Filipinos,” Mr. Felix said.

“Overall, I think what’s positive in the market is owning a residential unit is aspirational for a lot of Filipino households. While you see prices still increasing, Filipinos will definitely find a way to own a piece of property, to own their dream home, whether it’s a condominium unit or a house and lot unit outside of the Metro Manila,” Mr. Bondoc said.