The clock is ticking: The office of the future is here

By Claro Cordero, Jr., Cushman & Wakefield

ASIDE FROM the current and impending global economic challenges seeping through the local economy, attracting employees back to the office remains one of the top concerns faced by corporates and employers. The imperative to protect workers’ health during the COVID-19 pandemic has shifted working practices and caused workers and businesses to reconsider how often to use their offices, how to use the office differently in the future, and how much office space they will require.

Using real-time data captured from Cushman & Wakefield’s bespoke workplace strategy tool, Experience per Square Foot TM, the rising trend towards greater workplace flexibility is expected to take further shape in the post-pandemic period.

Interestingly, the evolution of the role of the office was underway even prior to the pandemic. Agile and flexible working has gained popularity due to recent technological advancements. Telecommuting or remote work for jobs requiring minimal client-facing interaction was encouraged to enhance overall employee well-being and talent retention while lowering cost and improving productivity.

POST-PANDEMIC OFFICE SPACE DEMAND

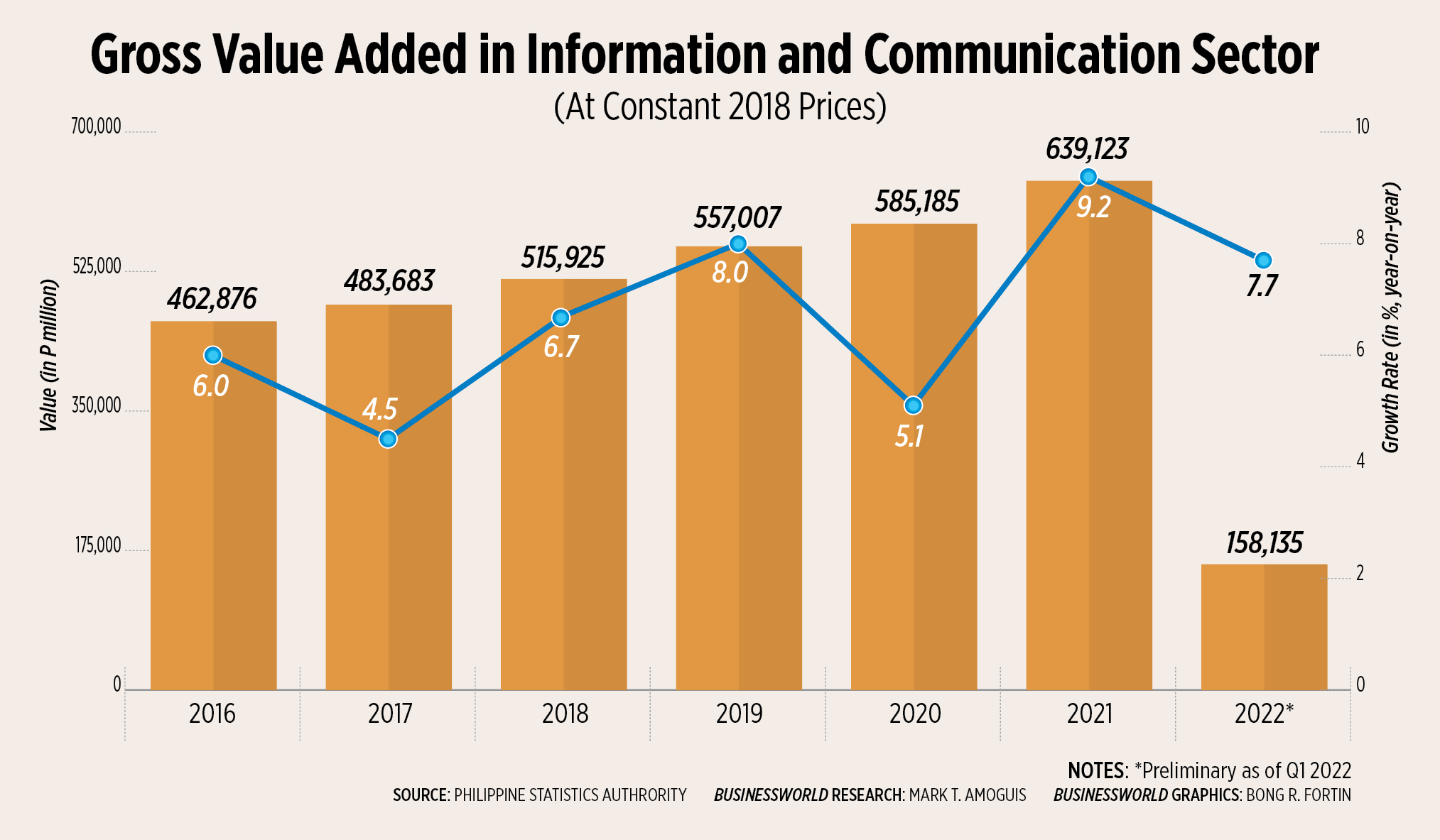

The long-term outlook for the major demand drivers of office space remains favorable, especially in the Asia-Pacific region. In its recent study, “Asia Pacific Office of the Future Revisited,” Cushman & Wakefield estimated over 23 million office-using jobs (which represent approximately 76% of all total global jobs) will be available in the Asia-Pacific over the 2020-2030 period. This employment growth is estimated to translate to about 100 million square meters (sq.m.) of office space. In the Philippines, total employment in office-using jobs is expected to grow by more than 2.4 million, equating to more than 8.3 million sq.m. in office space demand — which is equivalent to a more than 70% increase in the current stock of office space in the country.

The near-term outlook on net office space absorption in the Philippines will still be lower than the estimated average in the last 15 years. The expansionary demand in the medium term, however, will come from the continued growth of the outsourcing and information technology and business processing management (IT-BPM) companies. Beginning in the fourth quarter of 2021, net absorption in the Metro Manila market has recovered after breaching negative levels for five previous consecutive quarters.

EMPHASIS ON URBAN DOMINANCE

Unlike the trend towards urban decentralization in mature markets in the US and parts of Europe, rural-to-urban migration flow is still the predominant pattern in the Philippines. Major cities will continue to be the economic centers and attract talent. From a real estate strategic plan perspective, maintaining a solid presence in the commercial business districts (CBDs) and urban centers with modern facilities will be crucial to entice employees to return to the office. On the other hand, some industries, such as the IT-BPM industry, will thrive in a “hub-and-spoke” strategy, where maintaining operations in second-and third-tier cities and locations will ensure a steady flow of available qualified workforce.

THE EMERGENCE OF THE ‘PHYGITAL’ WORKFORCE

Generation Z (born 1997-2012) currently accounts for around 330 million or roughly 25% of the entire Asia-Pacific (APAC) population, but only approximately 13% of the working-age population (20-64 yrs.). By 2030, Gen Z will grow to around one billion and will comprise more than 30% of the working-age population in APAC. Being digital natives, Generation Z is looking at the seamless integration between the physical (which includes bonding with their team and growing their network) and digital (remote working experience) — or “phygital” — spheres in their workplace. The growing influence of this generation in instilling up-to-date policies and technology attracting and retaining the working population will determine the success of companies in retaining top-notch talent across the various workforce classes.

THE ROLE OF TECHNOLOGY IN WORKPLACE TRANSFORMATION

The central role of technology is crucial in instilling a paradigm shift on how the workforce view the workplace transformation amidst the rise of COVID-induced flexible working practices. Technology needs to be leveraged to enable the change in workplace strategy and as a platform to measure the impact of that change. In conjunction with this change is the alignment towards the corporate goals of Diversity, Equity, and Inclusion (DEI) and Environmental, Social, and Governance (ESG). Both DEI and ESG can help in understanding the demand of the workforce and in evolving the workplace strategy.

NO ‘ONE-SIZE-FITS-ALL’ STRATEGY

The various workforce segments will have different responses to their current work experience, as well as different needs. However, while the future of workplace is still evolving, the underlying change should begin with how both corporates and employees view the office space. Both occupiers and employees should treat the workplace as a focal point to inspire and be inspired to strengthen employee engagement. The challenge of enticing the workforce to return to the office rests on an optimal work environment for employees where productivity, satisfaction, and well-being are equally prioritized with the organization’s goal towards enriching culture and enhanced profitability.

CREATE INSPIRING WORKPLACES THAT DRAW PEOPLE BACK

Global corporate occupiers have started to implement ground-breaking workplace models to entice their employees back to the physical office space. Employees long for a diverse and inclusive environment and workspace that they can showcase to clients. The future of the workplace for each organization should undergo thoughtful occupancy planning to apply innovative workplace strategies and people-centric change programs that must have buy-in from all the relevant stakeholders.

To this end, we can expect a significant flight to quality among corporate occupiers, with state-of-the-art buildings featuring smart technology considered attractive by employees. Moreover, office spaces with flexible floor plans are preferred, to accommodate increased allocation for collaboration areas and well-being facilities (including nursing rooms, prayer rooms, and vending machines that dispense healthy snacks, among others). Workplace technology applications such as seamless booking of desks and meeting rooms, face recognition program for easier access, automatic doors and smart toilet systems will all contribute to efficient facility management of the transformed workplace.

The transformation of the workplace should be focused on the people, not just the place, to ensure that it translates to high levels of employee engagement. As the COVID-19 pandemic has underscored, attracting, and retaining the right talent should be given the same attention as occupancy costs in drafting the corporate occupier’s future workplace strategy.

Claro Cordero, Jr. is director and head of research, Consulting & Advisory Services at Cushman & Wakefield.

By Arjay L. Balinbin,

By Arjay L. Balinbin,