The 11.8% gross domestic product (GDP) growth in the second quarter (Q2) 2021 was celebrated with fanfare by the government and the ruling political party as “proof” that they are doing the right thing in guiding the economy out of prolonged recession. But this is not a good way to look at it.

One, there is the base effect. The GDP contraction in Q2 2020 was so deep, -17%, that any mild increase this year can lead to high percentage increase.

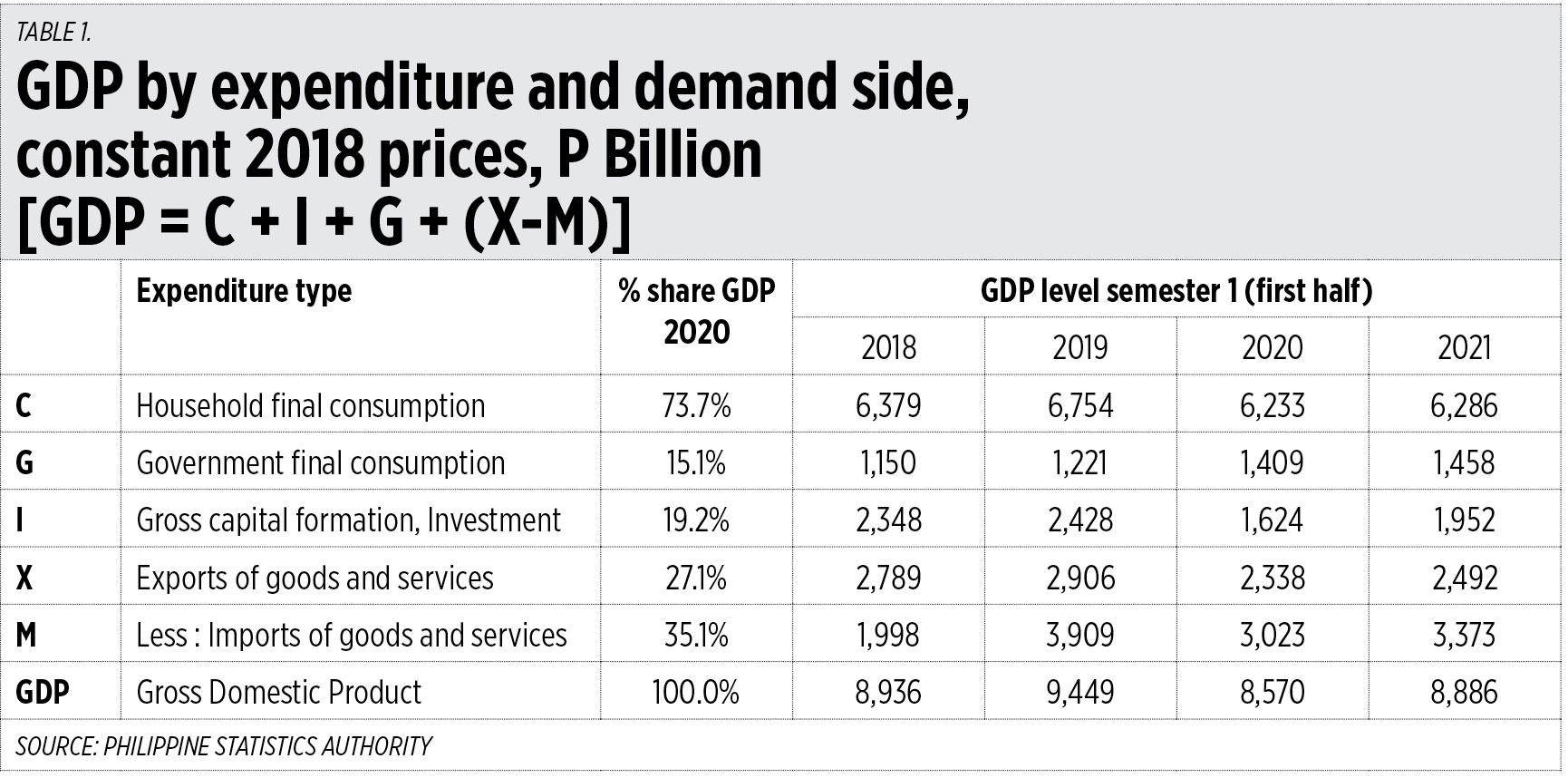

Two, the actual GDP level at 2018 constant prices: Q2 2018, P4.72 trillion; Q2 2019, P4.99 trillion; Q2 2020, P4.14 trillion; Q2 2021, P4.63 trillion. So, the actual flow of goods and services in Q2 2021 is even lower than Q2 2018.

Three, the GDP level by semester 1: first semester 2021’s P8.886 trillion is even lower than first semester 2018’s P8.936 trillion. And household consumption, which comprises 74% of total GDP, and investments, which make up 19% of GDP, suffered deep contractions in value (see Table 1).

On June 30, it was reported in BusinessWorld that, “ERC alters basis for triggering price caps to 72-hour average” or from five to only three days. As regular readers of this column notice, price controls, price caps, price dictatorships, are among the policies that turn me off. Goods and services available at varying prices and qualities are ideal for customers, very pro-consumer. Cheap but not available goods are anti-consumer.

The Energy Regulatory Commission (ERC) is misguided in keeping low the secondary price cap so that new peaking plants will hardly be built. They also added regional secondary caps of high voltage direct current (HVDC).

The ERC reasoned out that despite the low secondary price cap, there are still thousands of megawatts (MW) of committed and indicative power plantscoming in. But the ERC is silent about the fact that even in lockdown 2021 there were still red-yellow alerts, and even an actually rotating blackout last June 1. Meaning that supply capacity is thin and inadequate.

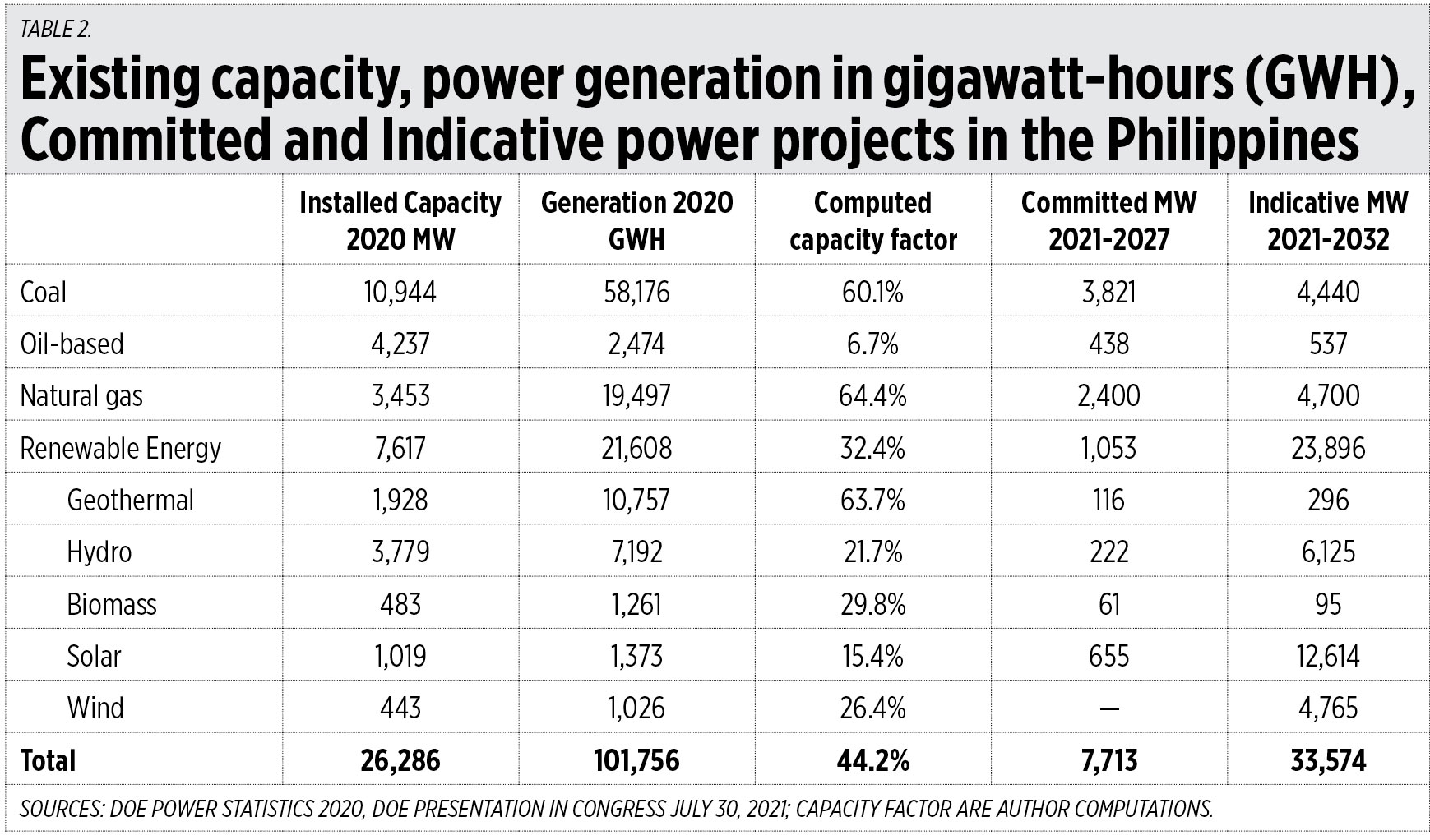

Ensuring long-term sustainability of growth in the country needs ample energy supply (see Table 2).

The good thing among the committed projects until 2027 is that coal will still play a dominant role as it is cheap and easily available. Natural gas comes next in the form of imported liquefied natural gas (LNG) and it is also good, provided that no favoritism be given to it like the mandatory off-take provision of Malampaya gas.

For the indicative projects, while there are 4,449 MW from coal and 4,700 MW from natural gas, the bulk of the increase will really come from solar, hydro, and wind.

And that is where big problems will show up someday. Intermittent and unstable energy that will require non-cheap batteries aspiring to be the dominant energy source in the country will push up electricity generation prices, and push transmission prices up as the grid system operator must get more ancillary services.

Market-based power supply-demand has been distorted by various agendas. But some provisions like the Retail Competition and Open Access under the Electric Power Industry Reform Act (better known as EPIRA) RA 9136, and Green Energy Option Program under Renewable Energy law RA 9513 also drive this high demand for the intermittent. So long as people will walk the talk, and pay higher without seeking subsidies from the rest of electricity consumers, this will be fine.

Bienvenido S. Oplas, Jr. is the Director for Communication and Corporate Affairs, Alas Oplas & Co. CPAs