Lenders’ Q1 asset growth quickest in 3 quarters

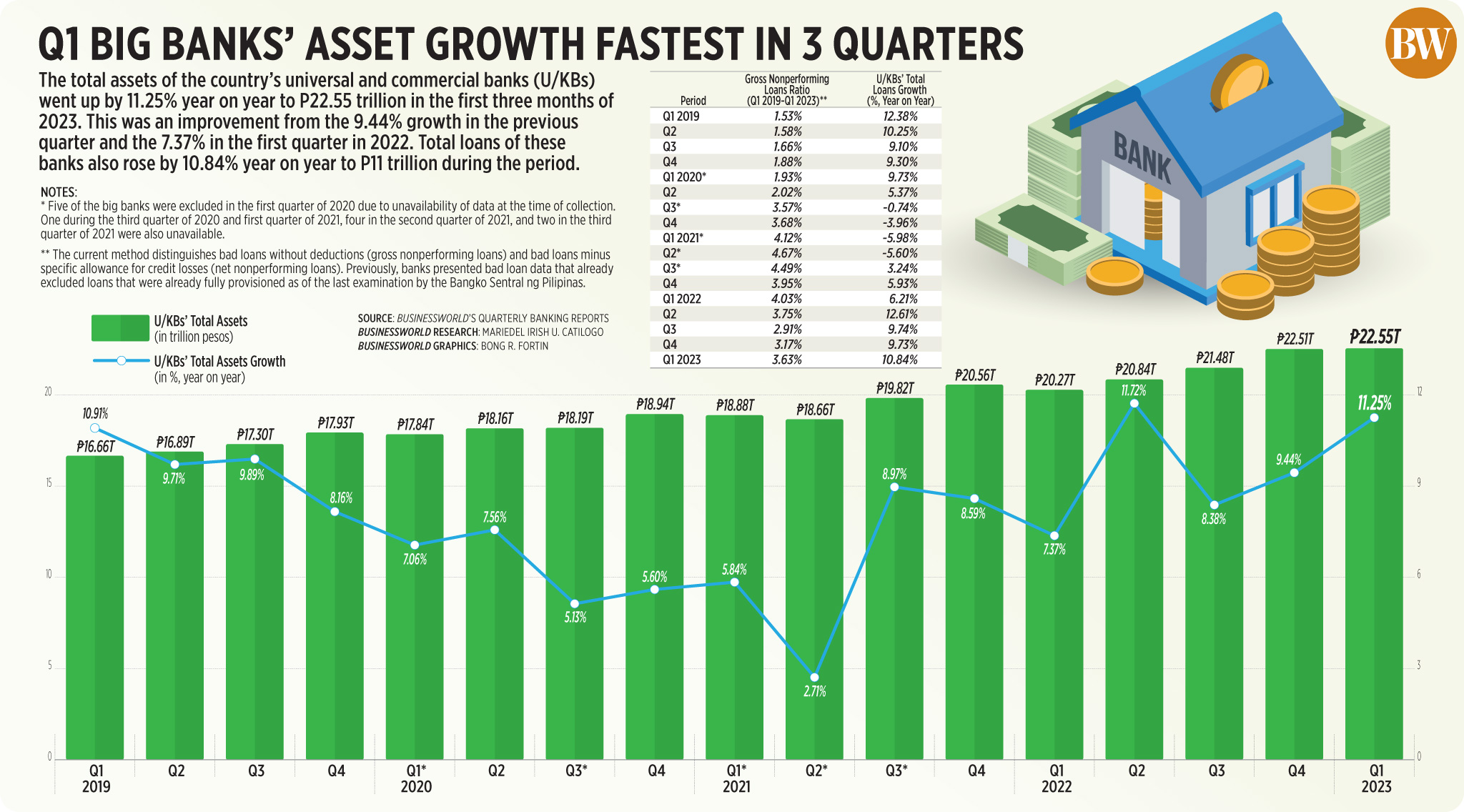

THE COMBINED ASSETS of the Philippines’ largest banks climbed by 11.25% in the first quarter, the fastest growth in three quarters.

BusinessWorld’s latest quarterly banking report showed the combined assets of 45 universal and commercial banks (U/KBs) jumped to P22.55 trillion in the January-to-March period from P20.27 trillion in the same period a year ago,

The 11.25% asset growth is faster than the 9.44% expansion seen in the fourth quarter of 2022.

This was also the quickest pace in three quarters or since the 11.72% increase seen in the second quarter last year.

Big banks’ aggregate loans went up by 10.84% to P11 trillion during the first three months of 2023. This marked the seventh quarter of loan growth, and the fastest expansion since the 12.61% logged in the second quarter of 2022.

The nonperforming loans (NPL) ratio, or the bad loans as a portion of the total loan portfolio, reached 3.63% in the January-to-March period. This was higher than the NPL ratio of 3.17% in the fourth quarter but lower than 4.03% recorded in the first three months last year.

The U/KBs’ nonperforming asset (NPA) ratio — the share of NPLs and foreclosed properties to total assets — inched up to 1% in the first three months of 2023, from 0.99% in the previous quarter. However, this was still lower than the 1.31% in the first quarter of 2022.

Foreclosed real and other properties as a share of the U/KBs’ total assets stood at 0.27%, slightly lower than the 0.28% in the preceding quarter but higher than the 0.26% in the same period last year.

Total loan loss reserves expanded by 7.68% annually to P391.47 billion during the period.

Big banks’ median capital adequacy ratio (CAR) — or the ability to absorb losses from risk-weighted assets — stood at 19.73%. This was higher than 17.97% in the fourth quarter but lower than the 21.73% in the same quarter in 2022.

The banks’ CAR remained above the required minimum 10% set by the Bangko Sentral ng Pilipinas as well as the international minimum standard of 8% under the Basel III framework.

Its return on equity (RoE) stood at 8.79% in the January-to-March period, higher than 6.36% in the previous quarter and 3.96% in the first quarter of 2022.

RoE is the ratio that measures the amount that shareholders make on every peso they invest in a firm, calculated by dividing the net profit to average capital.

BDO Unibank, Inc. (BDO) remained the biggest bank in terms of assets with P4.01 trillion, followed by Land Bank of the Philippines (LANDBANK) with P3.13 trillion, and Metropolitan Bank & Trust Co. (Metrobank) with P2.94 trillion.

In terms of deposits, the Sy-led BDO had the most deposits with P3.22 trillion, followed by LANDBANK with P2.79 trillion, and Metrobank with P2.26 trillion.

In the first quarter, BDO issued P2.5 trillion worth of loans, followed by the Bank of the Philippine Islands and Metrobank with P1.65 trillion and P1.35 trillion, respectively.

Among banks with assets of at least P100 billion, China Banking Corp. posted the fastest year-on-year growth of 31.72%. This was followed by Union Bank of the Philippines (UnionBank) and Rizal Commercial Banking Corp. with 30.30% and 24.85%, respectively.

UnionBank posted the fastest loan growth in the first quarter at 43.79%, followed by The Hongkong and Shanghai Banking Corp. with 39.83%, and Bank of Commerce with 25.97%.

BusinessWorld Research has been tracking the financial performance of the country’s large banks on a quarterly basis since the late 1980s using banks’ published statements. — Mariedel Irish U. Catilogo