When the Middle East burns, the Filipino nanay feels the heat

(Part 2)

At ASA Philippines, I have the privilege — and the responsibility — of knowing our close to 2.5 million clients not as data points, but as people. They are market vendors in Divisoria up at 3 a.m. to secure their stall and whose weekly profit margins can evaporate with a single price spike in cooking oil. They are sari-sari store owners in Tacloban, Leyte who absorb the price volatility that big retailers pass down the chain while they provide the access to more affordable goods their neighbors need on a day-to-day basis. They are food vendors in Polangui, Albay, buy-and-sell traders in Iligan City, and small dressmakers in Malolos, Bulacan — all operating micro-enterprises where income and expenditure are measured not monthly, but daily.

Their households are equally precarious. Their husbands are often farmers for whom rising fertilizer and fuel costs directly erode already thin margins, or fisherfolk for whom a single tank of diesel can determine whether going out to sea is profitable at all. Some are formal-sector employees in retail, food service, or small manufacturing — sectors that historically shed workers quickly when consumer spending contracts. Their children may still be going to school using jeepneys or tricycles, where every peso increase in fuel is additional pressure to the household’s thin wallet.

Many of these families rely on a microenterprise for daily income and a regular monthly income from a relative working in the Middle East or in Manila for financial stability. When both come under pressure simultaneously — the microenterprise squeezed by inflation and the monthly income contribution disrupted by retrenchments resulting from business closures caused by inflation pressures — the ability of households to build financial buffers becomes even more challenging.

What does the data tell us?

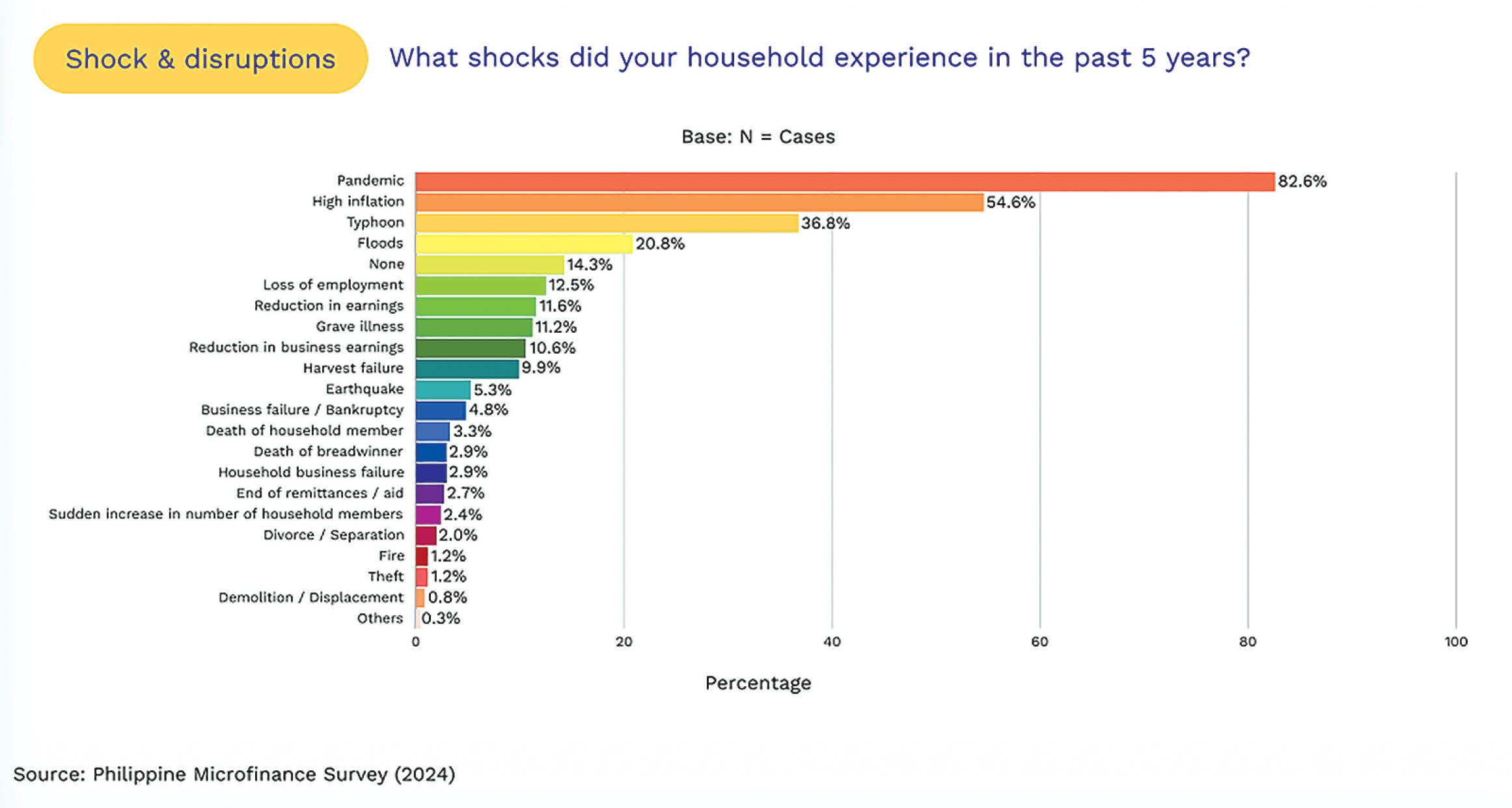

In 2024, the Philippine Microfinance Survey (PMS), a nationally representative study of 1,900 households conducted by Dr. JC Punongbayan, provided the most granular picture we have of these households’ shock experience and coping behavior.

In the survey, the respondents were asked to identify the top three shocks that negatively affected the household in the past five years. The top two shocks identified were the pandemic (82%) and inflation (54%). Both the pandemic and inflation are lingering and widespread shocks and, when combined, made recovery timelines difficult to predict.

The problem with prolonged recovery timelines is the factor of future shocks that could set back gradual gains. There have been several cases where families who are barely bouncing back from the pandemic are pulled further back by the destructive impact of post-pandemic typhoons (the third shock identified by 37%) that enter their areas. This is not a hypothetical risk. This is what our clients have already lived through once. And it is coming again.

The level of household resiliency and its ability to bounce back is dependent on its ability to generate cash and savings that can provide the cushion for unexpected shocks. And if shocks are coming one after the other, the question is whether or not the households have established enough income sources and savings to help them cope with the coming inflation shock due to the ongoing conflict in the Middle East.

HOUSEHOLD INCOME PROFILE AND SOURCES

Based on the preliminary results of the 2023 Family Income and Expenditure Survey (FIES) released by the Philippine Statistics Authority (PSA) in July 2024, the income of low-income families range from an average of P14,000 to P28,000/month.

Imagine when this income is undermined by retrenchments and high prices. Nanay (mother) clients have expressed that a little over 50% of their household budgets are allocated to food alone. In the latter part of 2025, it was reported that the Philippine government officially raised the daily food threshold to P85 per person from its original declaration of P64. This is approximately P12,800 per month for a family of five.

The 2024 PMS survey showed that around 6% of households residing in the country have no member in the family working and earning; 43% have one member of the family working and earning; another 38% have two members of the family.

The survey also asked the level of remittances coming from external sources of each household cluster. Of the 6% of households with no one in the family working, 72% of them receive remittances. For the 43% of families who have one family member working, around 19% are recipients of remittances while 38% of those with two members of the family working, around 7% receive remittances. This data shows that the fewer the local income sources, the higher the dependence on remittances.

While we do not have exact data on where the remittances come from, I am assuming that a significant amount comes from the Middle East, as based on recent data, around a little over a million or more than half (52%-56%) of the Philippines’ total land-based migrant workforce are located in the Middle East.

PROTECTING THE CLIENT, PROTECTING THE PORTFOLIO

As nanays and their families anticipate the coming shockwaves, microfinance institutions now face a dual imperative: protecting the households they serve while managing their financial health that makes that protection possible.

A prolonged oil-driven inflation shock will arrive gradually, first as rising PAR (Portfolio-at-Risk) numbers in market-adjacent branches, then in transport-dependent communities, then more broadly as consumer spending contracts across the entire ecosystem.

As such, microfinance institutions (MFIs) must closely monitor these indicators: on the macro side: Department of Energy (DoE) pump price adjustments, LPG price trends, Philippine Statistics Authority (PSA) consumer price indices disaggregated for the bottom 30% of households, the inflation outlook, and OFW deployment and repatriation data from the Department of Migrant Workers. On the portfolio side, they should monitor PAR trends segmented by geography and livelihood type, restructuring requests, emergency loan demand, and any unusual patterns in savings withdrawals — which can signal household stress before defaults materialize.

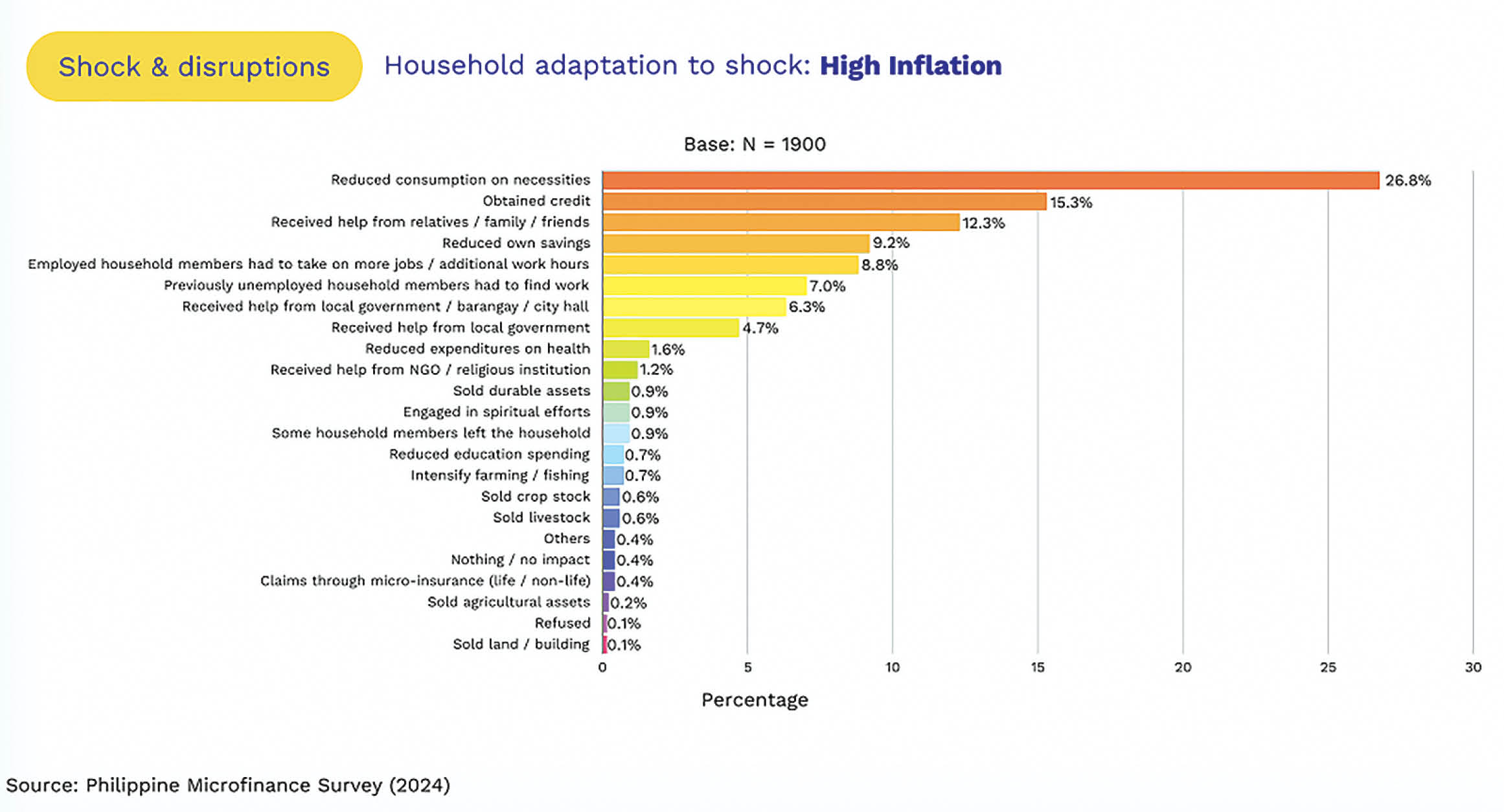

But MFIs must also act. The PMS also reveals how households respond when inflation strikes. Reducing consumption of necessities, not luxuries, was the most common coping strategy. The second most common strategy was borrowing. When households borrowed to cope with inflation, MFIs emerged as the second most cited credit source, behind family and relatives. MFIs stand between a family and a moneylender when government programs are delayed, remittances are interrupted, and savings have been depleted.

The PMS regression analysis shows that flexible repayment options and access to emergency loans are the MFI interventions most strongly and significantly associated with improved household consumption stability and economic resilience, which make the most measurable difference when families are under pressure. The analysis also suggests that MFIs that develop restructuring protocols, emergency credit windows, and empower managers on the ground to respond to early-warning signs will be the institutions that can best protect both their clients and their portfolios.

However, the PMS also underscores the importance of operational discipline and cautions against “evergreening” — restructuring loans without verifying genuine repayment capacity. The challenge is real: when a client’s business is under pressure and her family is hungry, the compassionate instinct is to give more credit. The responsible instinct is to ensure that credit actually serves her recovery. This is the razor’s edge that MFI leadership must walk in the months ahead.

A FINAL CALL: THE COLLABORATION IMPERATIVE

Until a more significant conclusion to this conflict is defined, it will be difficult to determine whether this becomes a contained shock or a prolonged regional war.

When COVID-19 arrived, the Filipino people demonstrated a surprising capacity for collective action. MFIs and other financial institutions put a moratorium on millions of loans and refrained from retrenching their workforce when the government declared the lockdowns. Government deployed emergency cash transfers at an unprecedented scale. Communities shared food through community pantries. That collaboration is what we must remember and reactivate with the same urgency.

While the impact of Middle East crisis may not be as immediate and drastic as the lockdown, a protracted crisis will still arrive in the form of higher prices at the palengke (wet market), thinner margins at the sari-sari (sundry) store, missed payments at the weekly center meeting, and the quiet anguish of a family whose purchasing power is suddenly diminished. Similar to the pandemic, the recovery will be long drawn, and we can only wish that there will be no more (or less severe shocks) that will come.

So, we need to keep our eyes focused on the millions of nanays and their families served by our colleagues across the microfinance sector; whose businesses are being squeezed by an inflation shock they cannot control.

But these women are not passive victims. They are resilient, resourceful, and capable of extraordinary adaptation under pressure. What they need from us — from government, MFIs, the private sector, and from civil society — is not pity. It is partnership. It is the assurance that the systems they depend on will not abandon them.

We must continue to be with them to endure the heat brought about by the fire raging in the Middle East war thousands of miles away.

Rafael C. Lopa is the president and CEO of ASA Philippines Foundation (www.asaphil.org), a microfinance NGO serving close to 2.5 million women entrepreneurs across all provinces of the Philippines. He is also the president of RestartME, Inc. (www.restartme.ph), an NGO mandated to work with microfinance institutions in addressing unexpected shocks to the lives and livelihoods of their clients and families. He co-funded the 2024 Philippine Microfinance Survey conducted by WeSolve Foundation.