Philippine business confidence weakest in over 25 years in March

BUSINESS CONFIDENCE fell to its weakest in more than 25 years in March as firms turned pessimistic on expectations that higher fuel costs from the Middle East conflict would curb consumer spending, a central bank survey showed.

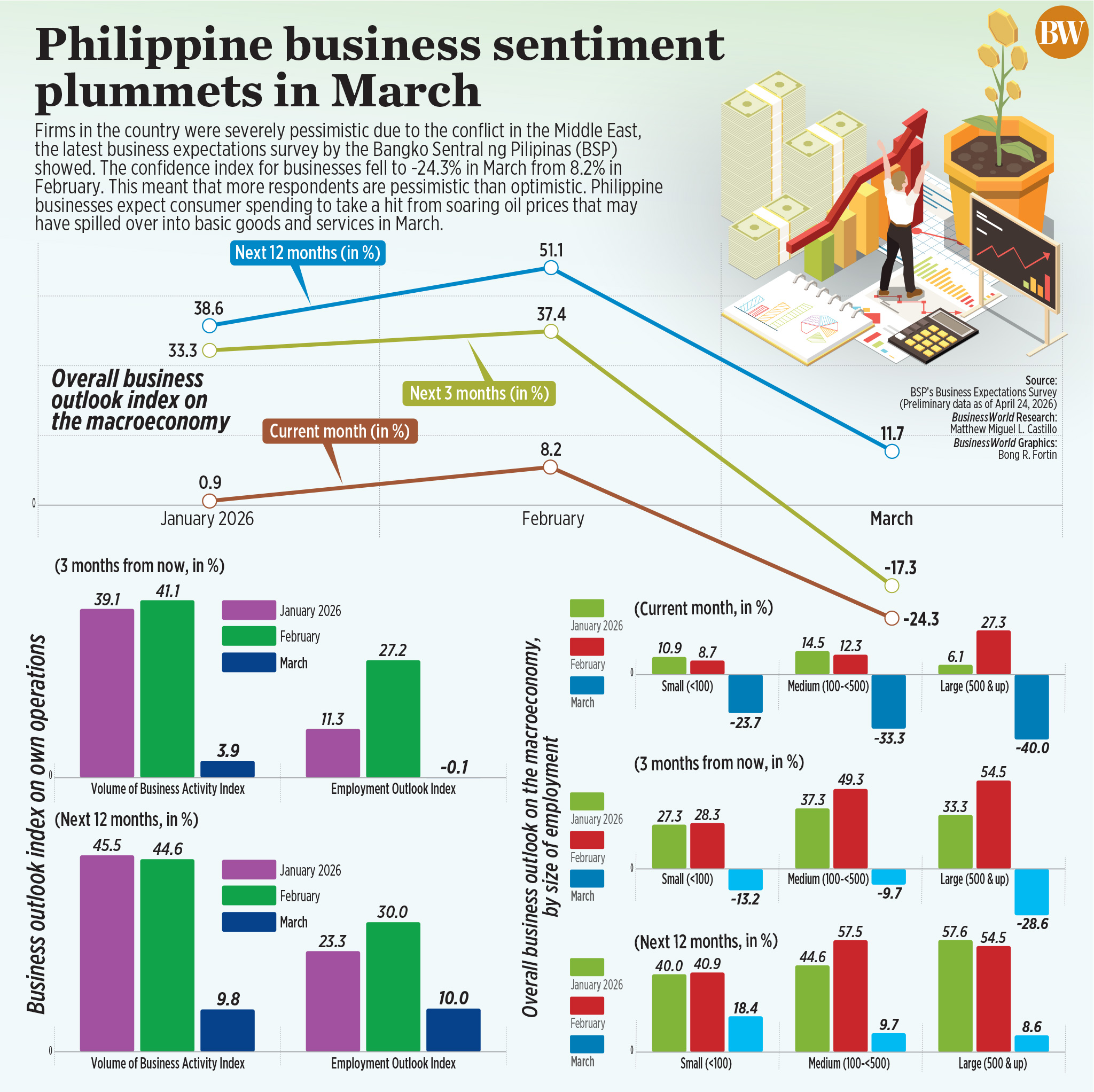

Results of the Bangko Sentral ng Pilipinas’ (BSP) monthly business expectations survey (BES) showed the current-month confidence index (CI) plunged to -24.3% from 8.2% in February.

A negative CI shows that more respondents are pessimistic than optimistic.

The March CI was the weakest in more than 25 years or since the -32.6% recorded in the fourth quarter of 2001.

“Firms attributed their pessimism in March 2026 to the ongoing Middle East conflict, which had led to a sharp increase in domestic pump prices. Businesses consequently expect consumer spending to slow, as higher fuel costs are seen to feed into the prices of other basic goods and services,” the BSP said.

The business outlook for the second quarter also turned pessimistic, while firms grew less optimistic for the rest of the year.

According to the survey, the three-month ahead CI declined to -17.3% from 37.4% previously. On the other hand, the year-ahead CI slid to 11.7% from 51.1%.

“Respondents’ outlook for both periods weakened on expectations that the adverse economic impact of the ongoing Middle East conflict may persist,” the BSP said.

Iran effectively closed the Strait of Hormuz after the US-Israeli war with Iran began on Feb. 28. This disrupted global energy markets, sending crude prices soaring and impacting import-reliant economies such as the Philippines.

The BSP survey showed firms expect tighter cash position and credit access, as the financial condition index turned more negative to -24.9% in March from -15.2% in February. The credit access index also turned negative to -7.1% from 4% in the previous month.

Financial condition refers to a firm’s general cash position considering the level of cash and other cash items and repayment terms on loans, while credit access refers to the environment external to the firm, such as the availability of credit in the banking system and other financial institutions.

Meanwhile, businesses in the industry and construction sectors reported higher average capacity utilization at 73.1% in March from 67.2% in February.

Firms in the electricity, gas, and water subsector also saw an uptick in activity at the start of the summer season.

“Businesses cited stiff domestic competition, insufficient demand, and high interest rates as major constraints to their business activities. They also cited the impact of oil price hikes, stemming from the ongoing Middle East conflict, as an emerging business constraint due to higher production cost,” the BSP said.

The survey also showed firms’ employment outlook indices turned negative to -0.1% for June from 27.2% previously. For the year ahead, the hiring outlook fell to 10% from 30% previously.

However, businesses still see room for expansion as the share of industry firms with expansion plans for June and the next 12 months increased.

“Despite prevailing uncertainties, some companies indicated that they would proceed with their expansion plans, as these were already in the pipeline even before the Middle East conflict started,” the BSP said.

Firms also expect the peso to depreciate in the second quarter and over the next 12 months. Respondents anticipated the local unit to average P59.60 in June, and P60 over the next 12 months.

On Friday, the local unit closed at P60.70 against the dollar, weakening by 22 centavos from its P60.48 finish on Thursday, Bankers Association of the Philippines data showed.

Businesses also expect peso borrowing rates to increase moving forward, while business inflation expectations rose.

More businesses expected inflation to average 2.8% in March, and anticipate inflation to average 3.1% in June and 3.3% in the next 12 months.

In March, headline inflation rose to a near two-year high of 4.1%.

The central bank now expects inflation to average 6.3% this year and 4.3% next year, both above its 4% ceiling, before returning to its tolerance range in 2028.

The BSP’s March BES covered 515 firms and was conducted from March 5 to 31.

Q1 CONSUMER CONFIDENCE

Meanwhile, consumer confidence improved in the first quarter, “reflecting conditions prior to the onset of the Middle East conflict,” the BSP said.

The BSP said the first quarter consumer expectation survey was conducted from Jan. 22 to Feb. 5, before the US-Israeli war on Iran started.

The survey showed that the current-quarter CI turned less negative to -15.8% in the first quarter, from -22.2% in the fourth quarter of 2025. This means there was a bigger drop in the share of pessimistic respondents than in the share of optimistic respondents.

“Respondents were less pessimistic in Q1 2026 as they expect: higher earnings, stable jobs, new income sources, and more family members joining the workforce,” it said.

For the quarter ahead, the CI slipped to 1.8% from 3.6% previously. For the year ahead, the CI also dropped to 9.6% in the first quarter from 11.8% previously.

“The less upbeat outlook of consumers for both periods reflected concerns over graft and corruption in the government, higher inflation, and ineffective government policies and programs,” the BSP said.

Consumer confidence also improved across different income groups.

For the April-to-June period, the outlook was still pessimistic among the low-income group but softened among the middle-income and high-income groups.

However, the outlook for the next 12 months became less optimistic among the low-income and middle-income groups. — Aaron Michael C. Sy