SINGAPORE — Singapore’s high court has convicted two people over what authorities consider to be the largest market manipulation case in the city-state, a joint statement by the Singapore police and Monetary Authority of Singapore said on Thursday.

For almost a decade, Singapore authorities have been investigating suspected trading irregularities tied to a so-called penny-stock crash in late 2013 that wiped out around S$8 billion ($5.78 billion) from the value of three companies within the space of a few days.

Quah Su-Ling and Malaysian John Soh Chee Wen were the masterminds behind an elaborate scheme to artificially inflate the value of shares of Blumont Group Ltd. (Blumont), Asiasons Capital Ltd. (Asiasons) and LionGold Corp. Ltd. (LionGold), the statement said.

The pair were found guilty on more than a hundred offenses each, including market manipulation and cheating, it said.

The scandal, which saw those stocks surge multiple times in the months before they slumped, battered investor confidence and led to a series of reforms to the city-state’s stock trading rules.

During investigations, Singapore authorities raided more than 50 locations and interviewed over 70 individuals, examining evidence consisting of more than two million emails, 500,000 trade orders, and thousands of telephone records and financial statements, the joint statement said.

Soh and Quah, who could not be reached for comment, will be sentenced at a later date.

A lawyer representing Soh did not immediately respond to a request for comment. Quah was not represented in court, according to media reports. — Reuters

Philippine motorcycle enthusiast John Aldwin Bagabagon rode easier than many other local motorcyclists and drivers this year as domestic fuel prices surged to record levels.

Mr. Bagabagon, 35, and his family are among 200,000 consumers turning to a homegrown app to secure credits for bulk fuel supplies at low prices, saving about 50% on their gasoline purchases over the past four months.

“I save a lot especially now that gasoline prices are rising weekly,” Mr. Bagabagon said.

The app PriceLOCQ allows users to stock up on fuel at a set price by converting purchases to digital credits that are later redeemed at Seaoil Philippines gas stations.

Mark Yu, who launched the PriceLOCQ app in 2020 and whose family owns independent fuel company Seaoil, says use of the app has “skyrocketed” since prices started rising this year, especially after Russia’s invasion of Ukraine disrupted global oil markets.

Gasoline sales via the app in a single day in mid-March hit 2 million liters, matching volumes for the entire month of February as consumers scrambled to get ahead of price spikes.

Half of PriceLOCQ’s clients are new customers of Seaoil, which has around 6% of the retail fuel market, said Mr. Yu, who is also the chief financial officer of Seaoil.

PriceLOCQ is the only app of its kind in the region, Mr. Yu said. Mr. Yu’s personal venture, LOCQ, is behind it, and partners with hedging firms to offset the risks amid volatile prices.

The Philippines imports more than 90% of its annual fuel requirements. Pump prices in capital city Manila, an urban sprawl home to 13 million people, have risen by 30% for gasoline and 66% for diesel this year, government data shows. Gasoline hit a record of 81.85 pesos ($1.56) per liter in mid-March 2022.

Early adopters of PriceLOCQ were able in 2020 to purchase up to 600 liters (158.5 gallons) of gasoline and diesel products for future refueling at around 20 pesos per liter. Prices now are around 79 pesos per liter.

While locking in prices in a rising market is enticing, consumers are advised not to hoard gasoline and buy according to their needs, said Bernard Flores, a Manila-based financial consultant for Pru Life UK.

Authorities have also warned customers to understand the underlying risks of using the app, including the non-transferability of the credits and the danger of buying bulk fuel and seeing prices fall.

“It’s like the stock market where you find the desired price you prefer and you lock in on it. Whatever happens, whether the prices go up or down, you are locked in,” Mr. Flores said.

Many motorists remained undeterred, though, especially those on the roads as part of their job.

“If this app didn’t exist, we would have a difficult time because … we use gasoline every day,” delivery worker Johnrey Omolon said.

“It’s a huge help. We get to prepare (for changes) every time gasoline prices increase.” —Reuters

THE eve of Philippine presidential elections could be a good window to plow money into the nation’s equities. In the six months following a presidential election, the Philippine Stock Exchange Index has given world-beating returns in four of the last five times there were polls to elect a new leader.

The Philippine Stock Exchange Index was up 3.4% six months after Rodrigo R. Duterte won in 2016, almost double the MSCI World’s rise in the same period. The gauge was up 38% at the six-month point after the 2010 vote and 17% after the 2004 election, about twice the global gauge’s gain in the same periods. A drop after the 1998 vote — in the aftermath of the Asian financial crisis and the election of B-movie actor Joseph E. Estrada as president — was the only time the Philippine index lagged its MSCI peer comprising both developed and emerging markets.

This upside bias could hold this year particularly if the election on Monday is free of irregularities and the new president names a credible economic team that fosters investors’ confidence, says Gerard Abad, chief investment officer at AB Capital & Investment Corp., adding stocks historically also gain in the year after the elections.

Ferdinand “Bongbong” R. Marcos, Jr., leads in most polls, with Vice President Maria Leonor “Leni” G. Robredo considered by many analysts as the only other candidate who can pull out a victory.

Investors expect some near-term headwinds. A polarized political environment would be a distraction for the country’s new chief, who must deal with surging inflation, rising interest rates and fallout from the war in Ukraine.

“There is strong distrust on both camps that could create a volatile political landscape and rattle the market,” says Jonathan Ravelas, chief market strategist at BDO Unibank Inc., who expects the benchmark to drop to about 6,500 in the near term.

Mr. Abad said he raised the cash proportion of his portfolio to about 17% from 5% in the run up to the election, noting that “stocks correct when politics get ugly.” But more cash will also make it easier to pick up shares on the cheap if the results fuel exaggerated selloffs. He’s currently favoring mining firms because of higher metal prices and also likes the defensive properties of the energy and telecom sectors.

“While a big part of the correction is due to threats of higher inflation, weaker peso and higher interest rates, the election is adding to the market weakness,” Mr. Abad says. “The next president is getting a tougher economy and a harder fiscal position than what Duterte inherited.”

Mr. Abad says investors may be lured back by economic reopening plays. His year-end target for the stocks benchmark is 7,800–7,900 — or as much as 15% higher from the current level. Potential fallout from the election is one of the reasons he lowered his 8,000–8,200 original target.

Political uncertainty has prompted some businesses to put decisions on hold. Metro Pacific Investments Corp., for instance, is yet to give its earnings guidance as the election will affect ventures such as toll roads, power projects and water distribution. Meanwhile, foreign investors have withdrawn net $274 million from Philippine equities this year. — Bloomberg

PARIS — Winning next month’s legislative election may be a long shot for France’s new hard-left alliance, but the fact President Emmanuel Macron now faces two eurosceptic opposition blocs should cause concern among France’s European Union partners.

The French left this week united under the leadership of a eurosceptic party that wants to “disobey” EU rules and “destabilize the Brussels machine”, departing for the first time from the pro-EU stance of previous left-wing coalitions.

This reflects a new state of play in French politics with the Socialist Party, long the dominant force on the left and a driver of European integration, now reduced to a subordinate role in an alliance forged by hard-left firebrand Jean-Luc Melenchon.

The Socialists garnered a meager 1.75% of the vote in April’s presidential election, while Mr. Melenchon, a fiery orator who leads the France Insoumise (France Unbowed) party, won 22%, almost pipping far-right leader Marine Le Pen to the run-off against Mr. Macron.

A poll published this week by Harris Interactive shows the left-wing alliance neck-and-neck with Mr. Macron’s party and allies with 33% of the popular vote. However, France’s two-round voting system means, according to the pollster, that it would still likely translate in a majority of seats for the president.

HEIR TO ‘NON’

Mr. Melenchon is the heir to France’s victorious “non” campaign that rejected ratification of a European Constitution in a 2005 referendum, deeply dividing the left.

Breaking away from the pro-EU Socialists in 2008, Mr. Melenchon founded a party that in 2017 did not rule out taking France out of the EU if the bloc refused to let it roll out its big-spending, protectionist platform.

The new alliance, which also includes Greens and Communists and will fight under the banner “Social And Ecological People’s Union,” says it wants to stay within the EU and does not want to abandon the euro.

However, some of its policies would certainly put France on a collision course with Brussels.

It wants to cut the retirement age to 60 from 62, raise the minimum wage by about 100 euros a month, nationalize the former French electricity and gas monopolies EDF and ENGIE and stop complying with EU budget limits and competition rules.

In the document sealing their alliance, the Socialists said that the concept of “disobedience” to EU rules reflected the “different history” between them and Mr. Melenchon’s party, and that they preferred to say they could “temporarily contravene” EU legislation.

But they add their joint goal is to “put an end to the EU’s free-market and productivist course” and that it could be done by creating “tension” with Brussels.

EUROSCEPTICS ON BOTH SIDES

When asked how they would manage to make Brussels swallow the pill, members of Mr. Melenchon’s party said the sheer size of France’s economy within the bloc meant the EU would have no choice but to agree — unlike the situation faced by the Greek government of hard-left Prime Minister Alexis Tsipras that lost a stand-off with the EU during the debt crisis.

“France is influential in Europe. It’s 18% of the European economy. It’s not the situation of the Greece of Tsipras that negotiated with 2% of the European economy,” Adrien Quatennens, a senior member of Melenchon’s party, told Franceinfo radio.

The new electoral pact still needs final approval from the Socialist Party’s national committee at a meeting on Thursday evening.

Even if it fails to win power in the June 12-19 parliamentary election, the new alignment on the left and the fact Mr. Macron is constitutionally barred from running for a third mandate in 2027 and has no obvious successor, increases the prospect of one of the two eurosceptic blocs winning power in the future.

“In the long term it’s part of a process in which French politics is splitting in three: a pro-European center and blocs of the nationalist right and nationalist left — raising question about how long the center can hold,” Mujtaba Rahman of the Eurasia Group think-thank told Reuters. — Michel Rose/Reuters

Cities continue to shape the way we live our lives — from shifting to greener lifestyles choices to reducing overall carbon emissions to help save the planet. The successful shift to greener cityscapes begin with the construction of green buildings, providing smart innovations that work with the environment and promote the well-being of the people who use these spaces on a daily basis.

According to a study made by the US Green Building Council, green buildings can reduce carbon emissions by around 40% on average, water consumption by around 30% and waste generation by around 70%. Beyond the environmental benefits, green buildings also help meet social needs by enhancing spaces, protecting human health, empowering differently-abled members of the community to take active participation and ensuring access to basic services at reasonable rates. Economic benefits can be felt as well with green buildings commanding higher rent potentials, encouraging ‘greenovation’ and promoting cultural and recreational activities without harming the environment.

Committed to making every day living better, SM Prime has taken the lead in incorporating sustainability and resiliency in its designs, making each component work together as a fully-integrated city of the future.

“Constructing greener buildings provides holistic solutions not only reducing emissions but also promoting social well-being,” shares Hans T. Sy, SM Prime Holdings Chairman of the Executive Committee. “We see this in our developments which drives us to build greener and even retrofit our existing malls to meet green standards.”

Among SM’s developments, a number boast of receiving LEED Gold certification while others are in the process of certification such as the SM Baguio expansion, SM North EDSA BPO offices, SM Megamall Mega Tower and SM Retail Corporation, to name a few.

SM Aura

The iconic SM Aura at the Bonifacio Global City is a mixed-use development that incorporates retail, trade halls and a Grade A office tower. The LEED Gold Certified mall promotes resource efficiency, green mobility and green landscapes.

SM Aura Bicycle Racks

Green Mobility. Cycling is encouraged with accessible bicycle storage, cyclists’ shower rooms and convenient access to safe lanes to public transit.

SM Aura Premier Park

Green Landscapes. The SM Aura Premier Park covers over 55% of the building, uses recycled water and provides enough room for plants to grow while protecting the building and people from heat.

SM Aura LEED GOLD Certification

Resource Efficiency. SM Aura uses 16% less than conventional buildings through a high-performance building envelope that reduces solar heat while allowing sufficient sunlight. Through low flow water sensor and metering faucets, it also reduces 1/3rd of its potable water use. Only low emitting materials were used as paint, adhesive sealants and floor materials.

Conrad Manila

Known as a lifestyle center, Conrad Manila is LEED Gold Certified. The hotel is designed with a dramatically-formed angular structure that houses a stylish 347-room hotel, spa and function space while S Maison is home to a swathe of smaller, more bespoke outlets for brands.

Bicycle racks at the Conrad Manila

Luxury Means Green Mobility. Boasting of high-end luxury experience, Conrad Manila remains environment-friendly by providing preferred parking slots for low emitting fuel-efficient vehicles, car-sharing vehicles and special parking spaces and facilities for cyclists.

Eco-Friendly Materials. Locally manufactured and recycled materials and products were used whenever possible with more than 80% of the project’s construction waste recycled. Filtration systems maintain a minimum efficiency rating of 90% to eliminate airborne particulates.

Conrad Manila LEED Gold Certification

Resource Efficiency. Conrad Manila is designed to reduce energy around 12% less than American energy standards. Its water heating system recovers heat from the chiller condensers to produce hot water while its ventilation system recovers the coolness from the exhaust air, returning that into the building. The hotel is outfitted with occupancy sensors, tinted with low emissivity insulated glass to keep heat and noise out.

Going beyond the LEED Certification, SM Engineering and Design Development, the mall’s design and construction arm has implemented these sustainable design strategies on the following projects:

SM Baguio Sky Garden

SM Baguio brings outdoor and indoor as one space optimizing natural lighting and ventilation with the Sky Garden. It has a green roof system as well as a provision for an underground water reservoir for storage and reuse of rainwater with a capacity of 4,389 cubic meters.

SM Seaside Cebu

SM Seaside Cebu mall goers can enjoy an extensive green area, center courtyard and roof garden. Constructed with low glass and utilizes EchoStop for noise management, the building is designed to maximize natural light and ventilation.

SM Lanang Sky Garden

SM Lanang Premier showcases lush greens, a roof garden and green pavers that encourage filtration and allow stormwater back to the underground soil. It is equipped with a rain water catchment system and a water reservoir with a 546-cubic meter capacity based on 425mm per hour rainfall intensity. It also has a materials recovery facility which receives, segregates and prepares recyclable materials for marketing to end-user manufacturers.

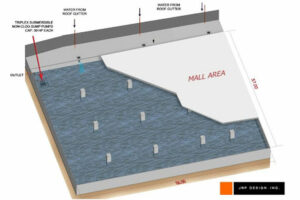

SM Masinag Holding Tank

SM City Masinag helps communities avoid flood waters through its 15,033-cubic-meter water catchment facility. It is designed with green screens to promote vertical plant growth and is constructed with Clerestory windows as a source of natural light.

SM North EDSA is one of the pioneers of the use of solar panels. It is also the first to have the Sky Garden and elevated parks.

The Mall of Asia

SM Mall of Asia is uniquely designed with a seawall to avert any damage from potential storm surges or seal level rise. Built on reclaimed land, it used an excavation method providing a greater degree of protection against liquefaction and seismic events. It is also elevated above the required building levels and is equipped with wave return and drainage channel to prevent flooding due to storm surges and high waves.

SM Marikina sits on 246 stilts and is built 20 meters beyond the compliance for safety zone. At 20.5 meters above natural ground level, it serves as a first responder and a place of refuge for the residents of Marikina during times of calamities.

SM Marikina on stilts

Today, real estate investors, both for business and personal use, have grown to prefer spaces that support sustainability agendas of the growing population. Pursuing green building standards support the public’s aspiration for more sustainable communities that are designed for environmental and social well-being. SM Prime believes that it is important for developers to work with communities on addressing climate change and achieving shared aspirations — a greener, more sustainable cityscape for all to enjoy.

“Creating a more sustainable way of life requires a sustainable backdrop that supports the shift. At SM Prime, our passion is to create one that is sustainable and resilient for the life we want for today and the future,” Mr. Sy said.

Spotlight is BusinessWorld’s sponsored section that allows advertisers to amplify their brand and connect with BusinessWorld’s audience by enabling them to publish their stories directly on the BusinessWorld Web site. For more information, send an email to online@bworldonline.com.

Users of Xbox Cloud Gaming will now be able to play Fortnitefor free on devices powered by Google-owned Android and Apple’s iOS thanks to a partnership between Microsoft Corp. and Epic Games, the companies said on Thursday.

The hit battle-royal videogame has been out of the reach of mobile users since Apple Inc. and Google removed it from their app stores in 2020 over a tussle about in-app payment guidelines.

The Microsoft partnership would allow users including PC gamers to stream Fortniteon internet browsers on their devices just like Netflix irrespective of the hardware specifications.

The move is likely to help Microsoft attract more casual gamers as the software giant doubles down on efforts to bolster its presence in the videogaming market and take on rival Sony Corp. The company earlier this year unveiled a $68.7 billion takeover of Call of Duty maker Activision Blizzard .

Fortniteis the first free-to-play title to join the Xbox Cloud Gaming service. “It’s an important step to add a Free-to-Play title to the cloud gaming catalog as we continue our cloud journey,” Microsoft said in a blog post.

Since launching in 2020, more than 10 million people around the world have streamed games through Xbox Cloud Gaming. The service is available in 26 markets, including the United States.

Microsoft, as well as Epic Games and scores of other firms, have criticized Apple’s store practices, which require developers to pay commissions of up to 30% for purchases made in the store.

The Fortnitecreator has also been involved in a legal battle with Apple, but it largely lost a trial last year over whether Apple’s payment rules for apps were anticompetitive.

That decision found Apple had suitable reasons to force some app makers to use its payment system and take commissions of 15% to 30% on their sales. — Reuters

Almost three times as many people have died as a result of coronavirus disease 2019 (COVID-19) as official data show, according to a new World Health Organization (WHO) report, the most comprehensive look at the true global toll of the pandemic so far.

There were 14.9 million excess deaths associated with COVID-19 by the end of 2021, the UN body said on Thursday.

The official count of deaths directly attributable to COVID-19 and reported to WHO in that period, from January 2020 to the end of December 2021, is slightly more than 5.4 million.

The WHO’s excess mortality figures reflect people who died of COVID-19 as well as those who died as an indirect result of the outbreak, including people who could not access healthcare for other conditions when systems were overwhelmed during huge waves of infection.

It also accounts for deaths averted during the pandemic, for example because of the lower risk of traffic accidents during lockdowns.

But the numbers are also far higher than the official tally because of deaths that were missed in countries without adequate reporting. Even pre-pandemic, around six in 10 deaths around the world were not registered, WHO said.

The WHO report said that almost half of the deaths that until now had not been counted were in India. The report suggests that 4.7 million people died there as a result of the pandemic, mainly during a huge surge in May and June 2021.

The Indian government, however, puts its death toll for the January 2020–December 2021 period far lower: about 480,000.

WHO said it had not yet fully examined new data provided this week by India, which has pushed back against the WHO estimates and issued its own mortality figures for all causes of death in 2020 on Tuesday. WHO said it may add a disclaimer to the report highlighting the ongoing conversation with India.

In a statement issued after the numbers were published, the Indian government said WHO had released the report “without adequately addressing India’s concerns” over what it called “questionable” methods.

The WHO panel, made up of international experts who have been working on the data for months, used a combination of national and local information, as well as statistical models, to estimate totals where the data is incomplete — a methodology that India has criticized.

However, other independent assessments have also put the death toll in India far higher than the official government tally, including a report published in Science which suggested 3 million people may have died of COVID in the country.

Other models have also reached similar conclusions about the global death toll being far higher than the recorded statistics. For comparison, around 50 million people are thought to have died in the 1918 Spanish Flu pandemic, and 36 million have died of HIV since the epidemic began in the 1980s.

Samira Asma, WHO assistant director general for data, analytics and delivery for impact, who co-led the calculation process, said data was the “lifeblood of public health” needed to assess and learn from what happened during the pandemic.

She called for more support for countries to improve reporting. “Too much is unknown,” she told reporters in a press briefing. — Jennifer Rigby/Reuters

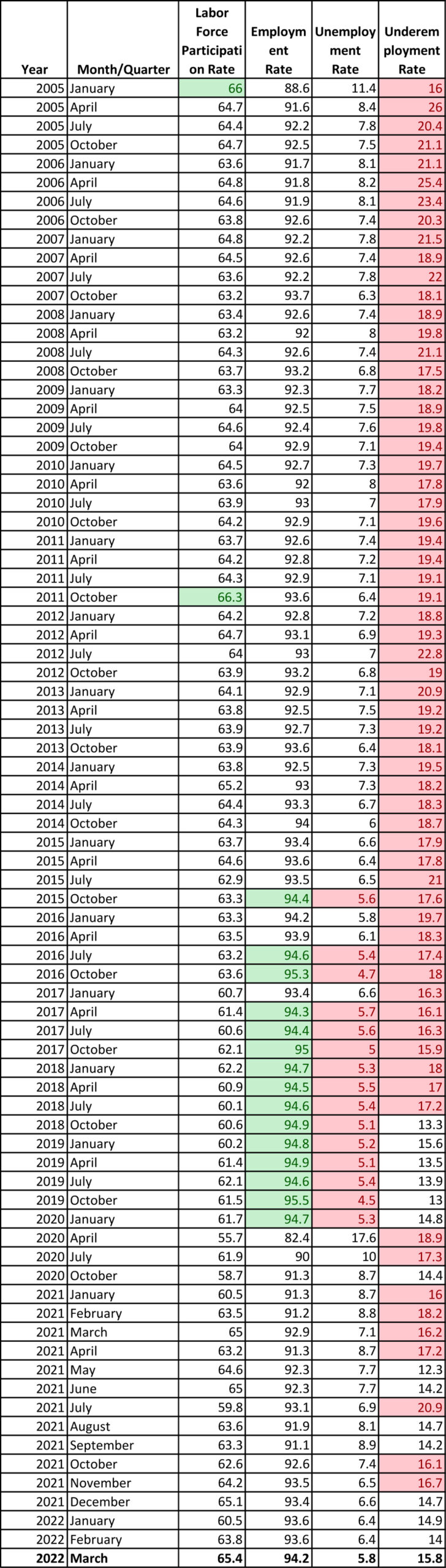

The country’s unemployment rate in March slowed to its lowest since the start of the pandemic, but job quality worsened to four-month high, the Philippine Statistics Authority (PSA) reported on Friday.

Preliminary results of the agency’s March round of the Labor Force Survey (LFS) showed the unemployment rate eased to 5.8% from 6.4% in February. However, it was also lower than the jobless rate of 7.1% a year ago.

The number of the unemployed Filipinos was reduced by 251,000 to 2.875 million in March from 3.126 million in February. This was lower by 566,000 from 3.441 million a year ago.

March’s jobless rate was the lowest since the 5.3% in January 2020, at the start of the coronavirus pandemic.

However, the quality of jobs slightly worsened in March. The underemployment rate — the share of those already working, but still looking for more work or longer working hours to total employed population — rose to 15.8% that month, an increase from 14% the previous month, but still lower than the 16.2% in the same period last year.

This translated to 7.422 million Filipinos looking for an additional job or longer working hours, an increase of 1.040 million from February’s 6.382 million and higher by 86,000 from 7.335 million a year ago.

Underemployment rate in March was the highest in four months or since the 16.7% recorded in November lasty year.

Meanwhile, the size of the labor force in March continued to pick up month on month by 1.244 million to 49.850 million. It was larger by 1.078 million from a year ago’s 48.772 million.

This translated to a labor force participation rate (LFPR) — the proportion of the total labor in the working-age population of 15 years old and over — of 65.4% in March, higher than the previous month’s 63.8% and last year’s 65%.

It was the highest LFPR since the 66.3% in October 2011.

The employment rate — the share of the employed to the total working force — was 94.2% in March, an increase from 93.6% in the previous month and 92.9% in March 2021.

This was equivalent to approximately 46.975 million employed Filipinos, higher by 1.495 million from 45.480 million in February. About 1.643 million Filipinos became employed from last year’s 45.332 million.

The PSA started reporting monthly jobs data in 2021. Prior to that, the agency published employment figures on a quarterly (January, April, July, and October) basis.

The March round of LFS was conducted from March 8 to 28. — M. I. U. Catilogo

THE COUNTRY’S trade-in-goods deficit widened to three-month high in March as merchandise import growth continued to outpace the growth in exports, the Philippine Statistics Authority (PSA) reported this morning.

Preliminary PSA data showed the value of merchandise exports grew by 5.9% to $7.171 billion in March, easing from 15.8% growth in February and 33.4% in March last year.

This was the lowest pickup in five months or since the 2% pace in October 2021.

Meanwhile, the country’s merchandise imports rose by 27.7% to $12.175 billion in March. This was slower than the 28.6% posted the previous month but faster than 22.1% a year ago.

This matched January’s pace and the lowest in five months or since the 25.2% growth in October last year.

This brought the trade-in-goods deficit to $5.004 billion in March, almost double the $2.759-billion gap a year ago. It was the widest trade gap since December last year’s $5.273-billion shortfall.

In the first quarter, the trade gap further yawned to a $13.892-billion deficit, wider than the $8.345-billion gap registered in the same period last year.

For the three-month period, exports rose by 9.8% year on year to $19.418 billion, above the 6% growth projected by the Development Budget and Coordination Committee this year.

Meanwhile, imports surpassed the 10% growth projection for 2022 with 28% increase during the first three months of the year to $33.309 billion. — B. T. M. Gadon

Notable of the early accounts of the Standard Chartered Bank’s long history in the Philippines is the note of national hero Dr. Jose Rizal who, while pursuing his advance studies in Paris, instructed his parents to send him money through Chartered Bank of India, Australia and China, former name of Standard Chartered Bank. The letter is taken from the Lopez Museum and Library Collection “One Hundred Letters of Jose Rizal to his Parents, Brothers, Sisters, Relatives,” by Jose Rizal, 1959, published by the Philippine National Historical Society.

More than facilitating transactions and regulating finances, long-standing banks are also witnesses to a nation’s history — from the struggles it faced to the progress it attained.

This can truly be said of Standard Chartered Bank (SCB), which has been supporting the Philippines in nation-building and, in turn, has gained the trust and confidence of the Philippine business community and the government through the years as the oldest international bank in the country. As it marks its 150th anniversary this year, SCB remains committed to be a leading financial institution that supports the Philippine economy — true to its promise of being “Here for good” — while moving forward towards sustainability and inclusivity.

SCB was first established in the country in 1872, taking the opportunities that opened in the nation’s capital, where significant trading business — coming from a number of British and American trading houses — was passing through.

With its first branch located in a modest lower story of a house in Binondo, Manila, then Chartered Bank’s early operations in the Philippines concentrated on financing machinery imports of the booming agricultural industries such as sugar, hemp, coconut, and shortly after copper, pig-iron, anchors, cordage, tobacco, coffee, and rice. The Manila operations, in particular, consisted chiefly of granting of accommodation secured upon export produce, imported merchandise, and promissory notes.

As worldwide demand for Philippine produce grew in the 1890s, the bank granted fixed loans to leading firms against sugar, hemp, copra, tobacco and coffee. It also financed shipments of sugar to China, Canada, and London; copra to Paris; and hemp to New York.

One of those who trusted the bank with his financial needs was the country’s national hero, Dr. Jose P. Rizal, who cited the Chartered Bank as a better choice for sending money in a letter he wrote to his parents in 1886.

“The day before yesterday, I received a draft of $200 which when collected in Francs gave me only 192, so 4% is lost. With more reason than ever, I repeat to you now what I have told you. If you are to send me money, do it by The Chartered Bank of India, Australia and China which is much better. Had you sent me those $200 through that House, they would have given me some 204 or 205 Francs,” the letter read.

The bank’s reputation further strengthened amid the passing of time — from American occupation of the country to World War II — as the bank continued gaining trust from clients like the government and keeping a strong presence in the country despite several historical challenges.

Later on, SCB Philippines brought significant contributions to development in the country as it has widely supported the commercial, industrial, and agricultural sectors and has helped greatly in the growth of some of the country’s exports.

Year 1969 was marked as a historic year when the two banks, The Chartered Bank of India, Australia and China, and The Standard Bank of British South Africa merged into what it is known today, Standard Chartered Bank.

Through the years, the bank has been instrumental in aiding the economic growth and development of the country, and actively progressed with its operations.

At present, SCB Philippines serves corporate and institutional clients, and solidifies its position as the bank of choice for cash management, corporate financing, loan syndication, and custody/securities services, among other services.

Having gained deep knowledge of the country, coupled with a strong global expertise network and pre-eminent cross border capability, SCB stands as a leading international bank in the country recognized for providing bespoke and innovative financial solutions for its clients. The bank is the leading Bookrunner for Philippine G3 bonds, having been actively involved in 75% of G3 currency issuances by Philippine issuers in 2021 (according to the 2021 Bloomberg league tables). The bank also holds the top Bookrunner spot for Philippine FIG PHP bonds which the bank has consistently held since 2018.

Testament to its leadership position is the host of awards the bank has received over the years. Recently, SCB Philippines was given the Top Corporate Issue Manager/Arranger Award (Bank Category) and Top Five Corporate Securities Market Maker by the Philippine Dealing System Holdings Corps and Subsidiaries (PDS Group); Best in Foreign Market Coverage Award by the Fund Managers Association of the Philippines; the Best Sub Custodian Bank by both the Global Custodian Awards and The Asset Triple A Servicing Awards; and the Best Bond Adviser (Global) by The Asset Triple A Country Awards.

As it moves forward beyond its historic past, SCB further commits to being a “Force for Good,” by promoting economic activity with positive social impact. One of the main ways SCB has been doing this is by supporting its clients in accelerating net-zero targets through sustainable finance. The bank has successfully assisted its clients with ESG issuances, in particular, acting as a Sustainability Structuring Advisor to the Republic of the Philippines’ (ROP) US$1-billion 25-year sustainability bond issuance and Sole Arranger to BDO Unibank’s PHP52.7-billion two-year ASEAN Sustainability bond offering earlier this year.

Alongside this effort, SCB is also promoting economic inclusion through its Futuremakers global initiative. Seeing how the pandemic made inequality worse, Futuremakers by Standard Chartered tackles inequality across SCB’s markets through fund raising and community programs that are anchored on the pillars of education, employability, and entrepreneurship.

It supports disadvantaged young people, to learn new skills and improve their chances of getting a job or starting their own business. In the Philippines, the bank works with local partners to provide capability trainings, seed funding and micro loans to lift economic participation of the youth, particularly women and girls. The bank’s community programs also promote digital adoption to align with the Bangko Sentral ng Pilipinas’ (BSP) digital payments push.

More than bearing witness to the Philippine development as the country’s longest-standing international bank, SCB Philippines remains steadfast and committed to play a significant role in boosting sustainable progress for the country.

A trailblazer in sustainable finance in the Philippines

Even as the world begins to pick up the pieces from a ravaging pandemic, it lies on the precipice of another great crisis: that which is brought about by climate change. The problem is far-reaching, intensifying with every passing year, and is severe enough to be dubbed “the biggest threat to modern humanity” today. Yet, the pandemic has proven that a global, united, collaborative effort can be a powerful force that can overcome any challenge. If individuals, enterprises, and organizations in both the public and private sectors can work together to find solutions to create a more inclusive, sustainable future, there is much reason to hope.

Green finance is one such solution. At its simplest, the World Economic Forum defines green finance as any structured financial activity — a product or service — that’s been created to ensure a better environmental outcome. It includes an array of loans, debt mechanisms and investments that are used to encourage the development of green projects or minimize the impact on the climate of more regular projects, or a combination of both.

In the Philippines, Standard Chartered Bank (SCB) is a leader in this space. The bank promotes sustainable finance to support economic growth, expanding renewables financing and investing in sustainable infrastructure where it is needed most.

The bank was mandated as a structural adviser of the Philippines Sustainable Finance Framework designed to support its sustainability commitments and set out how the country intends to raise green, social or sustainability bonds, loans, and other debt instruments in the international capital markets. The framework marks an important milestone for the country’s sustainability journey and the Philippine sustainable finance market more broadly, as it lays out the process that will be used to ensure transparency and disclosure of the use of proceeds, as well as the expected environmental and social impact of eligible green and social projects, in keeping with international best practices.

This is not the first time SCB has enabled sustainability-focused collaboration in the financial markets either. For over 150 years, it has aimed to provide banking services that help people and companies to succeed, creating wealth, jobs, and growth across some of the world’s most dynamic markets.

SCB led the Rizal Commercial Banking Corporation PHP17.87-billion ASEAN sustainability bond which won Best Sustainability Bond at the 2021 The Asset Country Awards. The bank acted as sole lead arranger and bookrunner in this first ASEAN sustainability bond issuance out of the Philippines in 2021.

Both RCBC and SCB have aligned their sustainable finance frameworks to prioritize capital raising and lending to sectors that benefit the environment and society. These range from renewable energy, green buildings, clean transportation, and pollution prevention and control — through to affordable housing, water provision, education and healthcare.

The bank is also Sole Arranger to BDO Unibank’s PHP52.7-billion two-year ASEAN Sustainability bond offering earlier this year. This landmark transaction represents the largest-ever Environmental, Social, and Governance (ESG) issuance out of the Philippines. Proceeds of the issue are intended to diversify the bank’s funding sources, and finance/refinance eligible assets under the bank’s Sustainable Finance Framework.

SCB also acted as a Sustainability Structuring Advisor to the Republic of the Philippines (RoP) US$1-billion 25-year sustainability bond issuance.

These issuances affirm the bank’s position as the leading ESG bond arranger in the country, having been part of approximately 42% of all Philippine USD and PHP denominated ESG bond offerings to date.

Collaboration within any industry is crucial towards creating long-term impact, and SCB believes that finance plays a key role in enabling such changes. Through multiple partnerships, the bank helps individuals to build a positive future for themselves and their families, businesses to thrive and grow, and governments to deliver economic prosperity for the wider community.

A leader in Philippine banking

Standard Chartered has come a long way as a strong partner to the country’s economic development and nation-building. Through the years, the bank has sought to live up to its brand promise — to be ‘Here for good,’ by supporting its clients while promoting a positive impact on the wider economy, and by accelerating net zero, lifting participation and resetting globalization.

SCB had long been a pillar of excellence for the Philippine financial industry. The bank has been recognized as a top-rated custody and fund administration service provider to leading foreign and domestic institutional clients, and has been recognized as Consistent Category Outperformer, Market Outperformer and Global Outperformer in industry surveys. The bank received back-to-back Best Sub-Custodian Bank awards at the Global Custodian Awards 2021 for three consecutive years and The Asset Triple A Asset Servicing Awards 2021.

The bank also continues to invest in its technology platforms, alliance, and networks to deliver quick and uninterrupted service to its valued clients. This is part of the bank’s efforts in accelerating its digital transformation and increasing collaboration with corporates, FinTech companies and developer communities. SCB Philippines is one of the few global banks to roll-out Instapay in its e-channels and an open loop payment gateway service through its Straight2Bank Pay solutions providing clients with access to online collections from various InstaPay, PESONet, and Real Time Gross Settlement (RTGS) participating institutions. The bank has also launched its Open Banking Application Programming Interface (API) services geared towards providing efficient services to its clients including their cash requirements, notifications, and real-time alerts.

Through its digitalization journey, the bank continues to enhance its capabilities allowing it to service the growing and complex needs of its clients in trade and commerce.

“We will continue to leverage on our extensive network, local expertise and global capabilities to provide innovative financial solutions to our clients,” country CEO Lynette Ortiz said.

“It is crucial that we ensure sustainable development through our business, operations and communities,” Ms. Ortiz added.

With the bank’s broad range of banking capabilities and on-the-ground expertise, Standard Chartered is helping businesses and society to navigate through the current crisis with an aim to build a more equitable and sustainable Philippines.”

Committed to being a ‘force for good’

SCB helps uplift Filipinos’ lives, backs education and inclusion

Standard Chartered Bank has been helping communities to tackle inequality through economic inclusion in markets. In the Philippines, it has been supporting disadvantaged women and young girls, young farmers and microentrepreneurs to earn, learn and grow.

Having been supporting the country through financial services and nation-building for 150 years now, Standard Chartered Bank (SCB) is indeed “here for good.” Still, for the international bank, being here for good is not good enough. SCB also aspires to be a “force for good.”

Merging its commitment to being a responsible and sustainable organization, SCB not merely seeks to create prosperous communities but also provide long-term value.

Globally, SCB has been preparing the next generation and empowering them to build their own future. Futuremakers by Standard Chartered is the bank’s global initiative to tackle inequality and promote greater economic inclusion for disadvantaged young people in our communities through education, employability, and entrepreneurship.

They would have the opportunity to learn new skills and have better chances to get a job or set up businesses.

In the Philippines, SCB partnered with SOS Children’s Villages to provide more than 1400 youth beneficiaries, particularly young women and people with disabilities, with decent employment and alternative sources of income through partnership development and various capacity-building interventions.

The bank’s initiative would pilot at least five business centers as venues for entrepreneurial training. It would also work with the government and private sector organizations for youth employability projects like youth mentoring, soft skills training, capacity building, organizational skills training, and reproductive health awareness. The project would also support the youth in their digital upskilling.

SCB also partnered with two microfinance institutions Tulay Sa Pag-Unlad, Inc. (TSPI) and the Alalay Sa Kaunlaran, Inc. (ASKI) to extend micro loans to women-led microenterprises to help them scale up their digital enterprises. The program also promotes digital adoption for microenterprises supporting the Bangko Sentral ng Pilipinas’ (BSP) digital payments push.

This year, SCB Philippines will launch a COVID-19 Economic Recovery program to provide more funding to small businesses gravely affected by the pandemic to boost community-based economic activities.

Through the years, SCB has demonstrated its commitment to the communities.

For the past five years, the SCB Livelihood and Education for Agri/Aquaculture Development (SCB LEAD), one of the bank’s flagship programs under Futuremakers, has been supporting the farm school Catbalogan City Agri-Industrial School (CCAIS) in Samar.

The program equipped its senior high school and graduate students with skills and knowledge to help them become professional farmers. It also offered them entrepreneurial opportunities through the set-up of agri-businesses.

This year, SCB has provided CCAIS with an additional model farm technology in poultry raising, and seed funding for its youth beneficiaries to help them start with their home-based agri enterprises.

In response to the COVID-19 pandemic, SCB launched a US$50-million charitable fund to support victims of the pandemic. The bank was cited by Leathwaite, an executive search and human capital specialist firm based in London, for leading in the global response to the COVID-19 pandemic.

From the US$50-million fund, the bank used the US$25 million for immediate relief efforts in the most vulnerable communities. The bank donated US$10 million to Red Cross and UNICEF, and US$15 million was allocated to local NGO partners across its markets. The remaining US$25 million was allocated for COVID-19 recovery programs supporting the youth and women through education, employability and entrepreneurship.

In the Philippines, SCB supported COVID-19 relief efforts in partnership with Philippine Business for Social Progress (PBSP).

The bank provided 10,000 family food packs to the most vulnerable communities in the National Capital Region and Region IV-A. Aside from the food packs, the bank also distributed more than 11,000 sets of reusable protective personal equipment (PPEs) to more than 40 hospitals and treatment centres nationwide.

Leader in diversity and inclusion

Standard Chartered is committed to promoting equality in the workplace and creating an inclusive culture where its employees can achieve their full potential. The bank continues to provide a collective voice to drive change. For years, the bank has embedded diversity and inclusion into its organizational DNA, celebrated female role models and allies to reaffirm its commitment to gender equality.

In 2021, Philippines CEO Lynette V. Ortiz was chosen as the UN Women Philippine WEPs Awards Champion in the Leadership Commitment Category. The WEPs Awards honour Asia-Pacific private businesses that champion gender equality in the workplace, marketplace and community in alignment with the Women’s Empowerment Principles (WEPs).

SCB ranked among the top 100 companies in Equileap’s 2022 Gender Equality Global Report and Ranking, and recognized on Bloomberg Gender Equality Index 2022 for the seventh year in a row. Financial Times also recognized StanChart as a diversity leader and signed a statement of support to the UN Women’s Empowerment Principles in 2018.

SCB offers its employees a differentiated workplace focusing on employee wellbeing, diversity and inclusion. Even before COVID-19 forced companies to adapt remote working, the bank has a flexible workplace policy already in place for years. At the onset of the pandemic in 2020, the bank immediately implemented flexible and split operations, safeguarding the health and safety of its employees by providing them with daily shuttle service and meals for two years.

The bank also formalized the implementation of its permanent hybrid working model. This data-led approach to work combines remote and office-based working with greater flexibility in working patterns and locations with the objective to redesign jobs, enable its workforce and prepare for the way forward.

Spotlight is BusinessWorld’s sponsored section that allows advertisers to amplify their brand and connect with BusinessWorld’s audience by enabling them to publish their stories directly on the BusinessWorld Web site. For more information, send an email to online@bworldonline.com.

Belonging to the advertising and communications industry that specializes in winning people’s hearts and minds, DDB Group Philippines has always seized opportunities to create positive impact on society through its work and its people.

For the upcoming May 9 elections, DDB Group came up with an “Election Day” information and advocacy campaign, which captures anew its commitment to help shape society by encouraging people to go out and vote.

This election, after all, is a rare opportunity to fully harness the power of democracy – that is, in choosing the leaders who will assume government positions – from the highest presidential post to that of a barangay councilor.

“Voting is the basic foundation of our democracy. It is a right that we Filipinos should not take for granted. It gives us the power to choose the kind of government, and yes, the kind of country we want to see in the near future,” said DDB Group Philippines Chairman and CEO Gil G. Chua.

Notably, to give the 65.7 million locally registered Filipino voters the chance to fully participate in the elections, Comelec has signed a resolution asking Malacañang to declare May 9 as a nationwide holiday.

“We encourage all registered voters within the DDB Group of companies to set aside their deadlines and job orders for the most important task on election day, that is, to cast their ballots. There is simply no reason not to go out there and vote. Every single vote matters!” said Chua.

Like their employees, DDB hopes that all Filipinos will prioritize voting on Monday as their participation in this election is the most valuable contribution they can give for the country’s future.

Spotlight is BusinessWorld’s sponsored section that allows advertisers to amplify their brand and connect with BusinessWorld’s audience by enabling them to publish their stories directly on the BusinessWorld Web site. For more information, send an email to online@bworldonline.com.

Israel shares best practices in cyber protection of the financial sector with the Bankers Association of the Philippines.

Israel shares best practices in cyber protection of the financial sector

The Embassy of Israel in Manila and the Israel Economic & Commercial Mission to the Philippines, in cooperation with the Bankers Association of the Philippines (BAP), hosted a virtual event last Feb. 16 focusing on cybersecurity entitled “Optimizing Cyber Protection of the Financial Sector: Best Practices from Israel.”

The program was divided into two parts: introducing the unique model of protecting financial institutions in Israel, and pitching of Israeli leading companies with innovative cybersecurity technologies and solutions for the financial sector.

Tomer Heyvi, economic counsellor and head of the Mission, shared that the purpose of this event is to share the Israeli expertise and technologies in the cybersecurity field in light of the growing challenges and threats that financial institutions around the world, including the Philippines, are facing these days.

In his opening remarks, Israeli Ambassador to the Philippines H.E. Ilan Fluss shared, “My vision for the future of relations between Israel and the Philippines is to see growth in cooperation in innovation and technologies especially in these critical and sensitive areas. Israel has proven itself as a reliable and solid partner of the Philippines, therefore, I believe we should see more partnerships in the cybersecurity area.”

In the first session of the program, Governor Benjamin E. Diokno of the Bangko Sentral ng Pilipinas shared his insights on Philippines Cybersecurity ecosystem and challenges in the financial sector.

In his speech, Governor Diokno mentioned some key areas for collaboration such as threat intelligence platform and setting up a national CERT, given the industry-wide initiatives in the Philippines and the maturity and sophistications of Israel in terms of cybersecurity controls and management.

“I hope this session will strengthen ties and cooperation between Israel and the Philippines so that our respective financial services sectors remain safe, innovative and resilient in the digital economy,” Mr. Diokno added.

Additionally, Jose Arnulfo A. Veloso, BAP president, highlighted in his remarks that cybersecurity remains to be a top priority of the association. He shared a number of advocacies of the BAP to promote and intensify its cybersecurity framework in the Philippine banking and financial services sector. “Together with the partnership of the guests in this forum, we can take them [cyberthreats] head on,” he noted.

Doron Liberman, director of International Cooperation Development in the Israel National Cyber Directorate (INCD), in his remarks shared the Israeli national approach and strategy to the cybersecurity ecosystem as a whole in the civilian sphere. “The INCD looks at its constituencies in different layers: critical infrastructure, sectoral and general public,” he said.

Mr. Liberman further shared that the INCD is a national agency that provides national intelligence and active defense tools and methodologies, and awareness events where their assistance is needed.

Rahav Shalom-Revivo, head of Financial-Cyber Innovation and International Engagements from the Israel Ministry of Finance, shared the multinational financial cyber simulation that the Ministry executed with countries that Israel has financial cyber relations with. In that simulation, she highlighted that international collaboration is key and that there must be synchronization between finance and cyber decision makers. She added, “The collaborative understanding that only together we can overcome such dramatic attacks that at some point in time will happen in the future.”

A study case highlighting the power of collaboration was shared by Eden Cohen, security head of Security Operation Center of Bank Hapoalim, the largest commercial bank in Israel. In her presentation, she shared that in the last three years, there has been a significant rise in organized cyber crimes towards financial organizations by new and advanced tactics to penetrate the digital world. With this, she highlighted that the best way to handle the new generation-attackers is by collaboration as a necessity to protect ourselves and our customers. She added that collaboration between people, businesses, technology, intelligence, and enforcements is a key factor to be able to face cyber-attacks in a quick and thorough way.

The discussion was followed by a pitching session of four companies offering cybersecurity technologies: Semperis: “Protecting your Active Directory, the keys to your Kingdom”; Trustpeers: “Turn Chaos into a Controlled Event with the TrustPeers Cyber Crisis Management SaaS platform”; Cybowall: “AI Powered Cybersecurity”; and CYE: “Continuous Cyber Risk Visibility — Cyber Risk Quantification — Cyber Exposure Optimization.”

Benjamin Castillo, managing director of the BAP, shared in his closing remarks that the power of collaboration is very important in cybersecurity. He mentioned continuing discussions with INCD and the Israel Ministry of Finance as the BAP continues to explore its options in building a national CERT.

Israel is one of the leaders in cybersecurity expertise around the globe, and it has about 40% of the global cybersecurity investments. Israeli’s cybersecurity industry continued to grow in 2021 with a record of USD 8.8 billion in investments in 131 funding rounds — this was tripled compared to 2020 at US$2.9 billion. Further, 33% of the Cybersecurity unicorns in the world are Israeli.