China trade dominance and small Philippine exports

The Philippine Statistics Authority (PSA) released the country’s international merchandise trade statistics for March. Merchandise trade means goods only — services trade like overseas workers remittances, international tourism revenues, etc. are not included. I compared the numbers with similar periods in 2023 and 2024 and the results are amazing.

First, our total imports in the first quarter or January-March this year were similar to 2023’s level at nearly $32 billion.

Secondly, imports from China are rising by an average of $1 billion/year, the percent share of China is rising, from 21.7% of total imports in 2023 to 27.9% in 2025. If we combine China plus Hong Kong, their share is 29.4% of our total imports which is huge.

Third, the combined share of imports from the US plus Japan plus South Korea is declining, from 22.5% in 2023 to 21.4% in 2025. This implies that Philippine businesses are slowly replacing their Isuzu, Hino, Hyundai, Ford, etc. buses and trucks in favor of Howo, Jac, Sinotruck, Yutong, King Long buses and trucks.

Fourth, the share of ASEAN-5 (Indonesia, Malaysia, Singapore, Thailand, Vietnam) is also declining, from 29.7% in 2023 to 26.9% in 2025 (see Table 1).

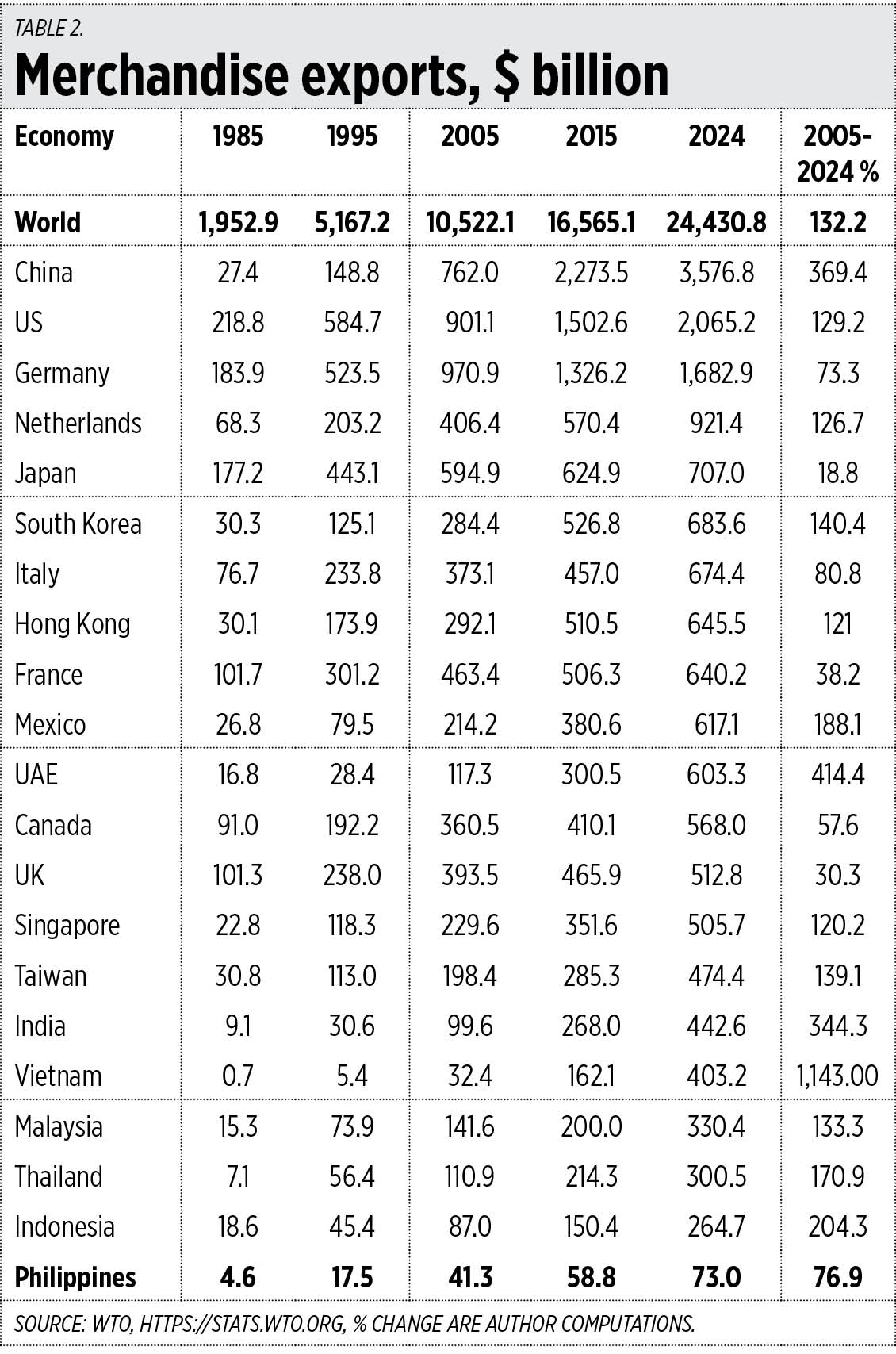

Also, a few weeks ago the World Trade Organization (WTO) released the full year 2024 merchandise exports data by country. The numbers there are also interesting.

First, world exports on average were doubling per decade from 1985 to 2005. There is a similar trend for industrial countries like the US, Germany, the Netherlands, and Canada.

Second, for many East Asian nations the expansion was much larger over the same period: on average a tripling per decade in countries like South Korea, Hong Kong, Singapore, Taiwan, Malaysia, Thailand, and the Philippines. But others have expanded four or five times per decade, like China and Vietnam. China joined the WTO only in 2001 while Vietnam joined the WTO in 2007.

Third, from 2005 to 2024, those that experienced trade expansion of more than 300% were China, India, Vietnam and the United Arab Emirates (UAE).

Fourth, until 2000 all G7 countries except Italy had higher exports than China. By 2005 China had overtaken them all except the US and Germany. By 2010, China had overtaken both. In 2024, China exports were 1.7 times larger than those of the US, 2.1 times larger than Germany’s, five times larger than Japan’s, 5.6 times larger than France’s, and seven times larger than the UK’s (see Table 2).

The Philippines still has the smallest number of exports among the ASEAN-6, with Vietnam’s exports 5.2 times larger than ours. There are two proximate reasons: geography and size of power generation. Vietnam can export to Thailand or China and vice-versa by land. Germany can export to France or Italy by land too. An archipelago, the Philippines can export only by sea and air.

In 2023, the Philippines’s generated only 119 terawatt-hours (TWH) of power while Malaysia generated 188 TWH, Thailand had 190 TWH, and Vietnam generated 276 TWH.

The country’s economic team can work with the infrastructure team to hasten the improvement of our infrastructure (airports, seaports, toll roads, rails, power generation-distribution, etc.). Our economic and fiscal policies should be as liberal, if not more liberal, than our neighbors because of our geographical isolation and disadvantage. We can also compensate with the increased exports of services, like attracting more foreign tourists, expanding the business outsourcing sector, and sending skilled Filipino workers overseas.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.