Introspective

By Romeo L. Bernardo

I am pleased to share with readers a post Christine Tang and I wrote for GlobalSource Partners (globalsourcepartners.com ) on March 18 on the potential economic growth impact of COVID-19 and on March 19 on the recent actions government has taken in the monetary and fiscal policy areas.

On Monday last week, as it became evident that putting Metro Manila on lockdown was not going to significantly limit the movement of people, President Rodrigo Duterte, upon the recommendation of health officials, expanded the lockdown to the entire island of Luzon, imposing strict home quarantine on all households, at the same time, suspending all public transport systems and closing down private establishments except those providing basic necessities, including health-related outlets, groceries and supermarkets, and banks. Also allowed to continue operating are export-oriented firms, including the business process outsourcing sector, while movement of goods will remain unhampered. Additional permissions followed a day later, including trading in capital markets, deliveries of food and medicines, and easing of restrictions for outbound international passengers, including overseas workers.

Considering the limited supply of testing kits when local transmissions began multiplying early this month, the lockdown appears to be the government’s only avenue to “flatten the curve” of daily infections and reduce the stress on local health facilities. As of March 21, 307 people have tested positive for COVID-19, with 19 fatalities and 13 recoveries.

Clearly, it is not possible at this time to quantify the cost of the lockdown. The assessment of the Central Bank governor of quarterly activity, taking note that the lockdown straddles the end of Q1 and start of Q2, is as follows: if it succeeds, the economy is in for a sharp V-shaped rebound; if it fails, the cost could be “large and protracted” with the recovery taking an elongated U shape.

This uncertainty on the adverse impact of the local lockdown is compounded by similar uncertainties regarding the effectiveness of drastic measures taken by governments in the west to contain the spread of the coronavirus in their own countries. Quite apart from the broadening impact on international economic activity (travel and trade), plunging stock prices, and outsized monetary policy responses, with the US Fed cutting rates by 150bp to zero, are reminiscent of conditions during the 2008-09 Global Financial Crisis, when world GDP contracted. The main piece of good news at this time is that China is starting to get back on its feet, with factory activity returning to “normal”

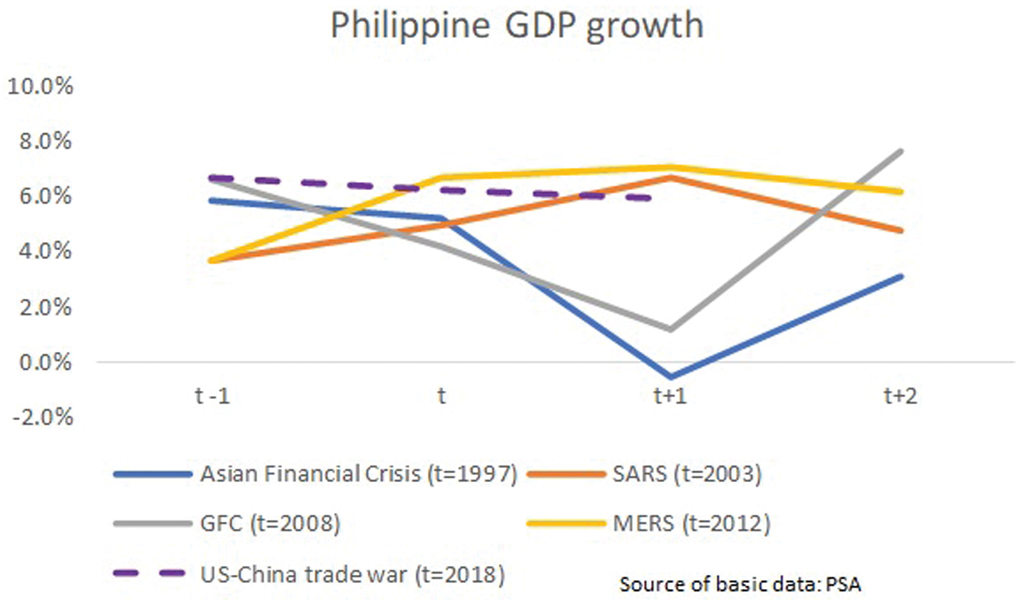

For now, we leave with readers the chart below of Philippine GDP performance during similar episodes in the past. We note that overall growth in past coronavirus outbreaks (SARS and MERS) held steady, suggestive of within-year recovery from any adverse impacts. On the other hand, past financial crises tended to drag on, taking time to resolve, with growth rates sharply down the year after the onset of the crisis. Considering trade tensions, the global spread of COVID-19 (it is a pandemic), the stringent measures taken by many governments, and the fact that the local lockdown covers an area accounting for about 70% of Philippine GDP, we think that the dotted line will continue to trend down, less sharply the sooner the virus is contained and the lockdown lifted. Lately, other analysts have started to downgrade GDP forecasts to below 5.5%. We think the likely downsides are deeper, even going to negative territory, unless stimulus measures from fiscal and monetary authorities to counter the downsides bring quick relief.

There is room for accommodation on both fiscal and monetary fronts, although ensuring bang for the buck will require careful targeting. For instance, on the monetary side, more interest rate cuts are expected beyond the “almost certain” 25bp signaled so far, which will also make the BSP’s rediscounting facility more attractive and encourage banks to lend to firms facing liquidity problems. On the fiscal side, in addition to a higher budget deficit (3.6% of GDP signaled so far) that preserves programmed spending, finance managers have announced additional off-budget support that will be coursed through public financial institutions with mandates to promote affected sectors, including tourism and micro/small/medium-sized enterprises, agriculture as well as incomes support through unemployment benefits for members of pension institutions.

This health crisis is happening at a time when the private side is much weaker and the credit cycle is nearing its end. Domestic investment activity did not perform up to par last year and some of the negative effects on current consumption are not readily recoverable within the year (e.g. permanent income losses, cancelled events). Moreover, the health of the world economy is much weaker considering ongoing trade tensions, tenuous geopolitical conditions (including an ongoing oil price war), and weakened international cooperation mechanisms.

MONETARY POLICY RESPONSE TO COVID-19

The Monetary Board (MB) of the Bangko Sentral ng Pilipinas (BSP) has introduced a package of measures to help combat the adverse effects of COVID-19 on domestic economic activity. These included: 1.) a 50bp cut in the set of policy rates, with the key overnight borrowing and lending rates reduced to 3.25% and 3.75%, respectively; 2.) temporarily setting the interest rate on its rediscounting facility equal to the lending rate; and, 3.) authorizing certain regulatory forbearance for banks involving more relaxed rules on compliance reporting, calculation of penalties on required reserves, and single borrower limits.

Per its statement, given the significant downward adjustment in its inflation forecast (2.2% this year and 2.4% next), the set of measures is intended not only to support growth momentum and uplift market confidence but mitigate the risk of financial sector volatility, ensure adequate domestic liquidity and credit in the financial system, and lower borrowing costs for affected firms and households. While signaling readiness to provide other supplemental measures, the MB nonetheless stressed the need for “urgent and carefully coordinated measures with other government agencies to alleviate the spillover effects of the pandemic on people and firms, with a view toward preventing any long-lasting economic and social damage.”

We agree with this. Policy stimulus needs to provide quick relief to affected sectors to avert a deeper decline in GDP growth and ensure more rapid recovery. As monetary policy works with a lag, the greater burden at this time falls on fiscal policy, which needs to provide immediate support not only to the health sector but direct subsidies to poor households who do not have the means to pay for basic food requirements if they are ordered to stay home. Philippine employment statistics show a large number of “underemployed” workers (over 6 million for the entire country) who, like some of the other non-regular/contractual wage/salaried workers, would receive no pay if they do not work.

So far, of the P27.1 billion mostly off-budget package announced by the economic team, only P3.2 billion will benefit displaced workers in the near-term. This is just a fraction of the P13.6-billion income replacement cost estimated by the Chairman of the House Ways and Means Committee for Metro Manila alone. Also, the government would need to consider providing tax relief for firms with short-term liquidity problems (as in other countries) and plan for continuing social distancing measures even after the lockdown is lifted, for example, supporting public transport systems.

We think that given the seriousness of the crisis and how other countries have responded with large stimulus packages, markets would be forgiving of a one-off unplanned increase in the budget deficit in 2020 that allows the economy to recover quickly. Considering the continuous downtrend in the debt ratio and rise in the tax effort since the administration came into office, we think an overall deficit number not exceeding 5% for this year would be reasonable.

Romeo L. Bernardo was finance undersecretary during the Cory Aquino and Fidel V. Ramos administrations.