A first look at the medium-term fiscal program

I am pleased to share with readers a post that Christine Tang and I wrote for Globalsource Partners (globalsourcepartners.com) subscribers on the Philippines fiscal outlook. We are their Philippine Advisers.

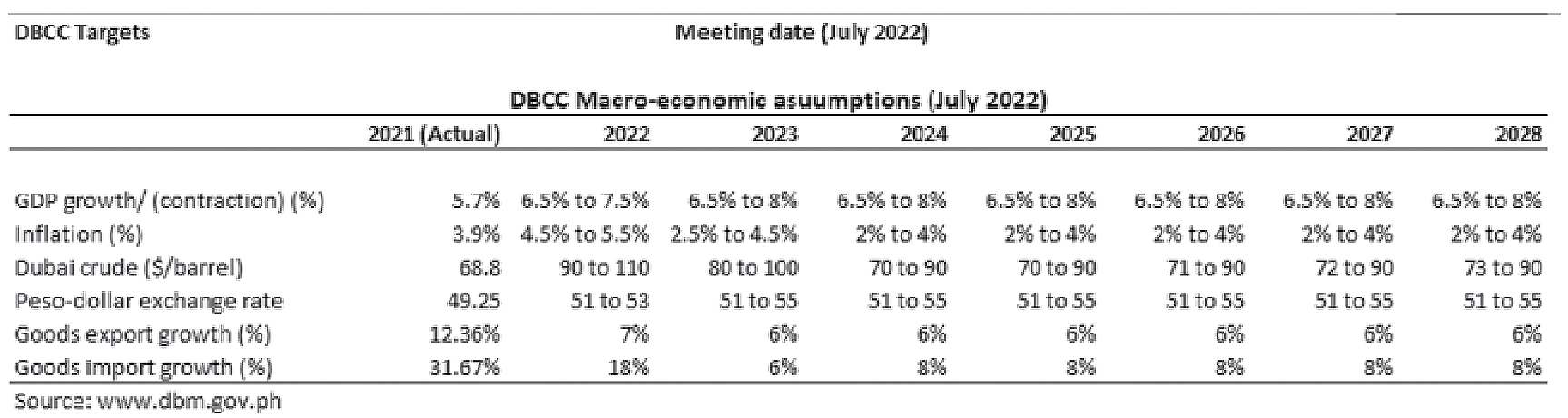

Last Friday, the Development Budget Coordination Committee (DBCC), an inter-agency body made up of the departments of budget, finance, planning and the BSP (Bangko Sentral ng Pilipinas), presented the new administration’s fiscal program for 2022 to 2028. The medium-term program hinges on the economy sustaining its growth clip at 6.5% to 8% starting 2023 and inflation returning to the BSP’s 2% to 4% target starting 2024.

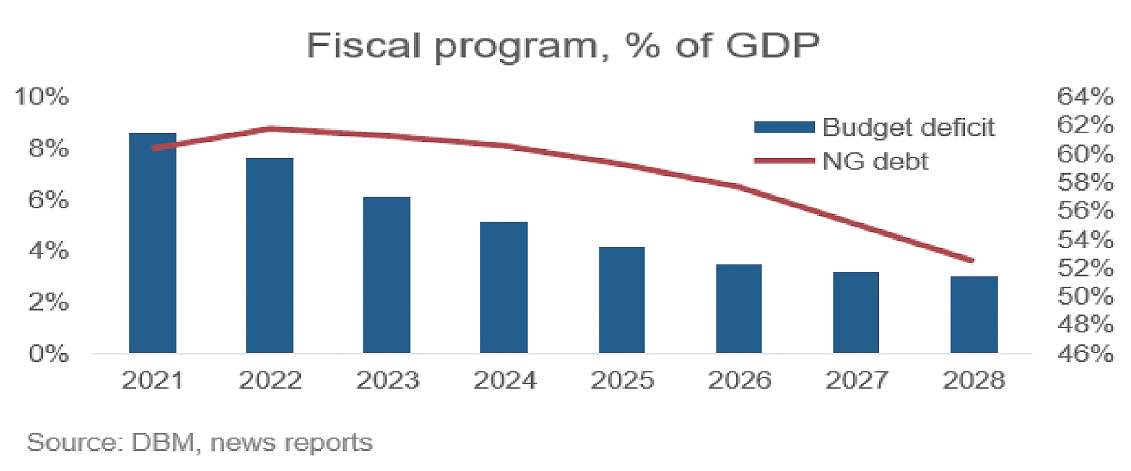

Given nominal GDP growth of 9% to 10%, the fiscal program aims to reduce the overall national government (NG) budget deficit, which reached 8.6% of GDP last year, by 1 ppt every year until it falls to 3% of GDP, the pre-pandemic deficit target. With this performance, it expects the NG debt ratio, which is anticipated to creep up to 61.8% of GDP this year, to gradually drop to 52.5% of GDP by the end of the administration.

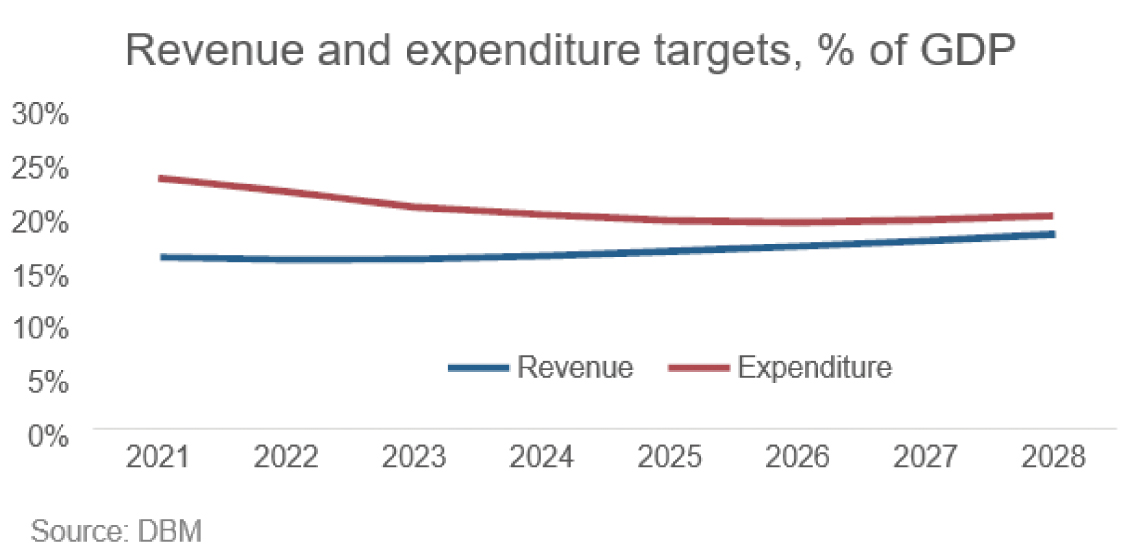

The reduction in the deficit and debt ratios to GDP will be done through a combination of raising revenues and cutting expenditures relative to GDP. The revenue effort is programmed to rise from 15.5% last year to 17.6% by 2028 or an increase of 2.1 ppt, while spending as a share of GDP is programmed to fall from 24.1% last year to 20.6% in 2028, equivalent to a decrease of 3.5 ppt. Despite the reduction in expenditures, government intends to keep infrastructure spending at 5% to 6% of GDP.

OUR VIEW

As far as the numerical targets are concerned, the latest medium-term fiscal program is basically an extension of the last one, crucial mainly in terms of signaling to markets that the new administration is committed to pursuing fiscal consolidation. The 2028 target for the debt ratio, i.e., 52.5% of GDP, is certainly more realistic and supportive of post-pandemic recovery needs, than a promise of quickly paring it to the pre-pandemic ratio of 39.6%.

We are looking forward to the nuts and bolts of the fiscal program, particularly:

1. New economic growth drivers that will keep the medium-term GDP growth rate at 6.5% to 8%, an ambitious target for the post-pandemic period especially with the lingering effects of the pandemic, the many external headwinds (end of cheap credit, elevated commodity prices, slowing global economic growth) and government’s more limited macro policy space (both fiscal and monetary) to support domestic consumption and investments.

We note that the 6% growth target for goods exports is itself unaspiring, especially in light of the new laws liberalizing foreign investments.

2. Sources of new revenues that will keep revenue growth above nominal GDP growth from 2023 onwards. The Finance secretary said recently that the economic team will pursue the remaining tax packages of the Duterte administration, dealing with property valuation and financial sector taxation which, while revenue neutral, will make the tax system more efficient. He is also in favor of imposing taxes on digital transactions but did not specify expected revenue inflows.

3. Expenditure reforms that will create space for continuing social protection programs, especially in health and education, and maintaining infrastructure spending at 5-6% of GDP, even as government pared its overall spending as a share of GDP. The budget for military pension liabilities alone is expected to take up about 1% of GDP annually during the term of this administration.

We await the President’s State of the Nation Address later this month where he is expected to present his administration’s economic program.

End.

POSTSCRIPT:

Although we expect GDP growth this year to reach 6.8% (driven by base effects and election spending), we think the government’s 6.5% to 8% growth target through 2028 is rather ambitious.

My own gut feel is medium-term growth potential is now much lower, closer to 4-5%, the long-term Philippine growth rate rather than the 6-7% of the past decade pre-pandemic. As mentioned in our post, this is because of the drag from scarring from the pandemic (closed businesses, education, and labor mismatches) and considering the end of decade long credit cycle (cheap credit), elevated inflation everywhere affecting consumption and investments, global economic slowdown, even risk of recession, and government’s more restricted fiscal space.

But I would like this government to prove me wrong. The way I think it can do this is if it can quickly earn investors’ trust to attract more FDIs, especially job creating ones, and revive PPP (public-private partnerships) as a way of sustaining infrastructure investments, including digital ones. Moving us towards more investment rather than consumption driven growth.

On PPP, there are immediate to do’s:

1) Signal respect for sanctity of contracts and the rule of law by complying soonest with the terms of the MWSS concession agreements and the international arbitration ruling. (See the column of National Scientist and UP Economics Professor Raul Fabella https://bit.ly/Fabella060622).

2) Scrap the midnight revisions on IRR (implementing rules and regulations) on build-operate-transfer (BOT) projects and PPPs. The flawed revisions include overly restrictive MAGA coverage (material adverse government action), and removal of provisions on parametric formula for rate setting, and on international dispute settlement. (Please see the Op Ed that summarizes the specific concerns of the Foundation for Economic Freedom and the Makati Business Club https://bit.ly/BOT_amendments ).

Romeo L. Bernardo was finance undersecretary from 1990-96. He is a trustee/director of the Foundation for Economic Freedom, Management Association of the Philippines, and FINEX Foundation. He is Philippines principal adviser to Globalsource Partners

romeo.lopez.bernardo@gmail.com