Colliers Insights

By Joey Roi Bondoc

FILIPINO consumers’ propensity to shop and visit brick-and-mortar malls is starting to rebound. We now see the resurgence of high-density retail segments such as family entertainment centers, and this should result in greater traffic in malls.

Many mall operators are reporting that consumer traffic is starting to return to 2019 levels. Colliers sees holiday-induced spending further propping up the sector and supporting a slight rise in rents through end-2022. More retailers are now willing to take up physical space, which should bode well for retailers and mall operators. We are optimistic that vacancy will improve by 2024 and this should lift mall lease rates.

We recommend that developers take advantage of the retail sector’s rebound and the lifting of travel curbs by strategically opening malls sized to the catchment area considering the new retail environment; curate retail mixes; future-proof high density retail; and utilize activity centers to draw more customers and entice them to spend.

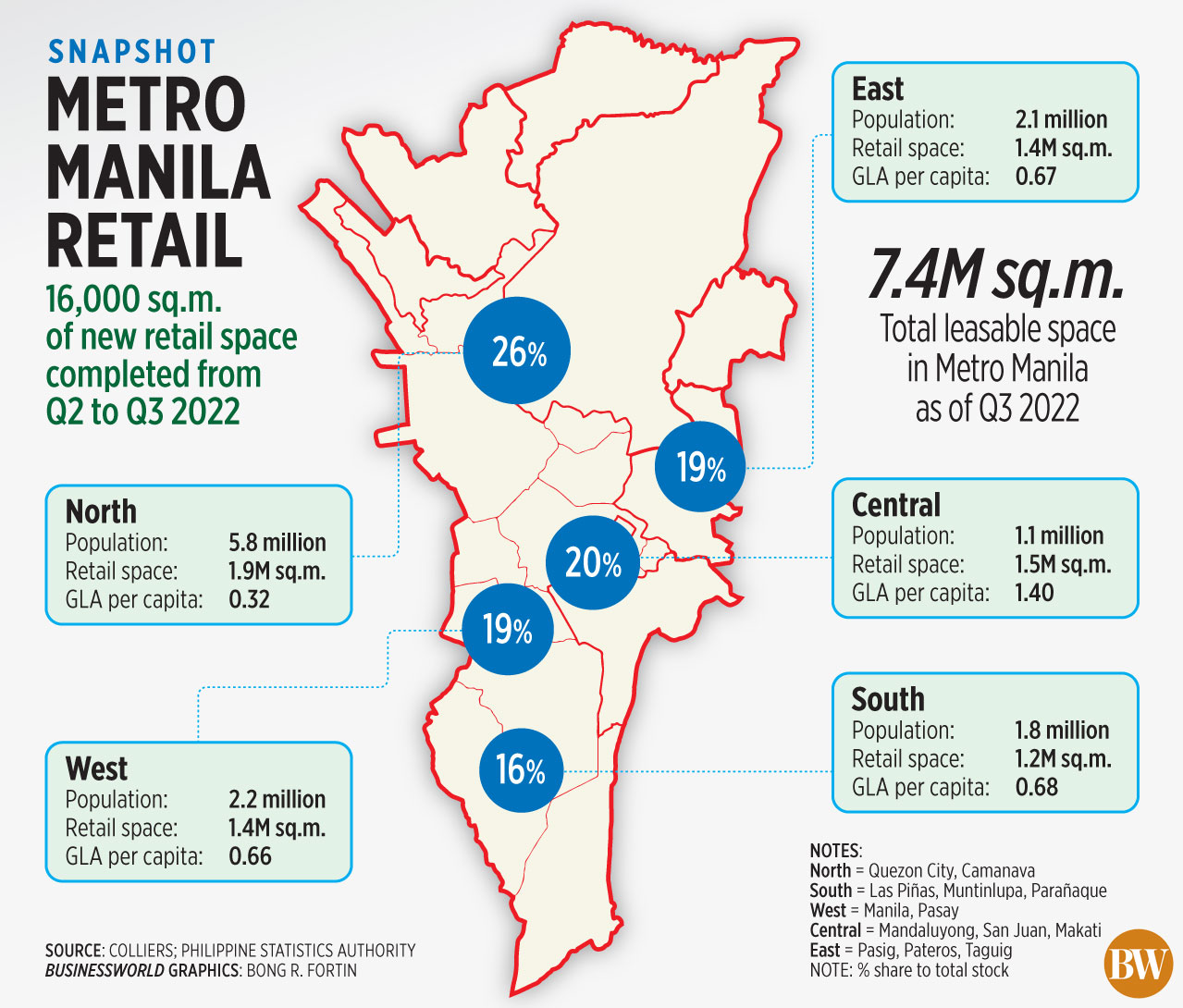

TAPERED NEW SUPPLY

From the second quarter to third quarter this year, Colliers recorded the delivery of 16,000 square meters (sq.m.) of new retail space with the completion of neighborhood malls such as The Shops at Ayala Triangle in Makati central business district (7,000 sq.m.), The Link at Robinsons Metro East in Pasig City (5,000 sq.m.) and Waltermart Novaliches in Quezon City (4,000 sq.m.).

In 2022, we expect the delivery of about 356,000 sq.m. of new supply, 13% lower than our previous forecast of 409,000 sq.m. as some developers pushed back completion of their projects. From 2022 to 2025, we see the annual completion of 247,700 sq.m. Of the new supply, 80% will likely be in the Bay Area and Quezon City.

MARGINAL RISE IN VACANCY

In the third quarter, vacancy across malls in the capital region reached 15.4%, a slight increase from the 15.2% recorded in the first quarter. Major developers have been reporting that consumer traffic has now reverted to 85-95% of pre-pandemic levels.

Retailers have also been active in taking up physical mall space from the second quarter to third quarter this year, as they take advantage of rising consumer traffic, coupled by an anticipated increase in purchasing power due to the holiday season. Among the retailers that took up space during the period include: Skechers and Superga in Powerplant Mall, Rumba at The Shops at Ayala Triangle, Café Kitsune at The Podium, Ever New Melbourne at Trinoma and Yoshinoya at Eastwood Mall.

In our view, the headwinds that will likely hinder the retail sector’s expansion include supply chain disruptions, global recession fears, and persistently high inflation.

The Bangko Sentral ng Pilipinas reported that third quarter consumer confidence was −12.9%, 7.7 percentage points lower quarter on quarter. However, the outlook for consumer confidence in the next 12 months turned more optimistic, reaching 33.4% in the third quarter from the 32.4% reported in the second quarter.

Meanwhile, the Philippine Retailers Association is also bullish on the sector’s growth trajectory despite rising inflation as more consumers return to physical retail formats. The rise in remittances as well as release of employees’ holiday bonuses should also boost retail spending in the fourth quarter.

Colliers retains its forecast of a 16% vacancy in 2022 from 14.8% in 2021. We attribute the rise to the completion of 356,000 sq.m. of new supply. We project vacancy to further rise to 17.0% in 2023 before receding to 14% in 2024.

SLIGHT RISE IN RENTS

Colliers recorded a slight uptick in lease rates in the third quarter, up 0.4% compared to the 1.7% correction in the first quarter. In our view, the projected pick up in retail space absorption and consumer traffic for the remainder of 2022 should support the rebound in rents. In 2022, we project rents to grow by 1%, an improvement following a combined 15% correction from 2020 to 2021.

MONITOR RETAIL SEGMENTS VULNERABLE TO INFLATION SPIKES

Data from the Philippine Statistics Authority show that inflation in the first nine months averaged 5.1% from 4.0% in 2021. In our opinion, this will constrain spending on some consumer subsegments.

Hence, Colliers recommends that mall operators and retailers constantly monitor which segments are likely to be affected by inflation spikes and which are likely to withstand the impact of rising consumer prices.

Despite rising inflation, we have observed that retailers from the food and beverage (F&B) and fashion segments continue to take up physical space. Colliers’ data show that the F&B segment will likely account for about 50% of the upcoming retailers, followed by clothing & footwear at 21%. This should also enable mall operators to better curate and future-proof their retail mixes.

ASSESS IDEAL SIZES FOR NEW MALLS

Colliers encourages developers to reassess the ideal sizes for upcoming retail outlets as they welcome more consumers under a better and newer normal. From 2024 to 2026, we see the delivery 62,000 sq.m. of new mall space yearly, only a fifth of the annual completion of 327,200 sq.m. of new retail space that we recorded from 2017 to 2019.

INNOVATIVE USE OF SPACES TO DRAW CONSUMERS

Colliers believes that mall operators should reactivate their event spaces or activity centers and attract more mallgoers by organizing events such as trade fairs, exhibits and concerts to drum up retail interest. Meanwhile, F&B and clothing and footwear retailers should consider opening pop-up stores, especially those testing the Metro Manila retail market which is starting to rebound post-Covid.

FUTURE-PROOF HIGH-DENSITY RETAIL SPACES

High-density retail spaces were greatly affected by the coronavirus disease 2019 (COVID-19) lockdowns. Now that restrictions have eased and consumers are starting to go out and gather, Colliers recommends that retailers continue encouraging social distancing measures and implementing regular sanitation and other health and safety protocols. Now is an opportune time to ramp up marketing of these high-density retail spaces.

Joey Roi Bondoc is associate director for research at Colliers Philippines.