Delivering on business and consumer expectations

There was clear convergence among the three major international financial institutions (IFIs) in terms of the Philippines’ growth prospects for 2022. True, the International Monetary Fund (IMF) slightly downgraded its prognosis but both the World Bank and the Asian Development Bank (ADB) actually upscaled their forecasts. The three institutions were one in estimating that the Philippine economy will grow by 6.5% this year. The outlier is the Singapore-based ASEAN+3 Macroeconomic Research Office (AMRO) that topped the three IFIs’ common forecast, by elevating its April forecast of 6.5% to 6.9%.

Except for AMRO’s, the growth forecasts of the three intersect the Philippines’ official target of 6.5-7.5% at its tail.

It is quite interesting that despite the directions of their updates, they all collapsed into one single growth rate.

They have their own reasons. The IMF is worried that the potential recession in the United States and China could affect local conditions. Such global shocks could come from reduced external trade with both countries such that the country’s growth momentum in the first half of the year is likely to slow down. For the World Bank, the sentiment is very bullish because of accommodative fiscal policy that is expected to recover domestic demand. For the ADB, the easing of mobility restrictions is expected to motivate a rebound in domestic demand and business activities. Like the ADB, AMRO holds that the growth driver is the reopening of the economy. Infrastructure projects will be key to investment demand.

But what is happening on the ground?

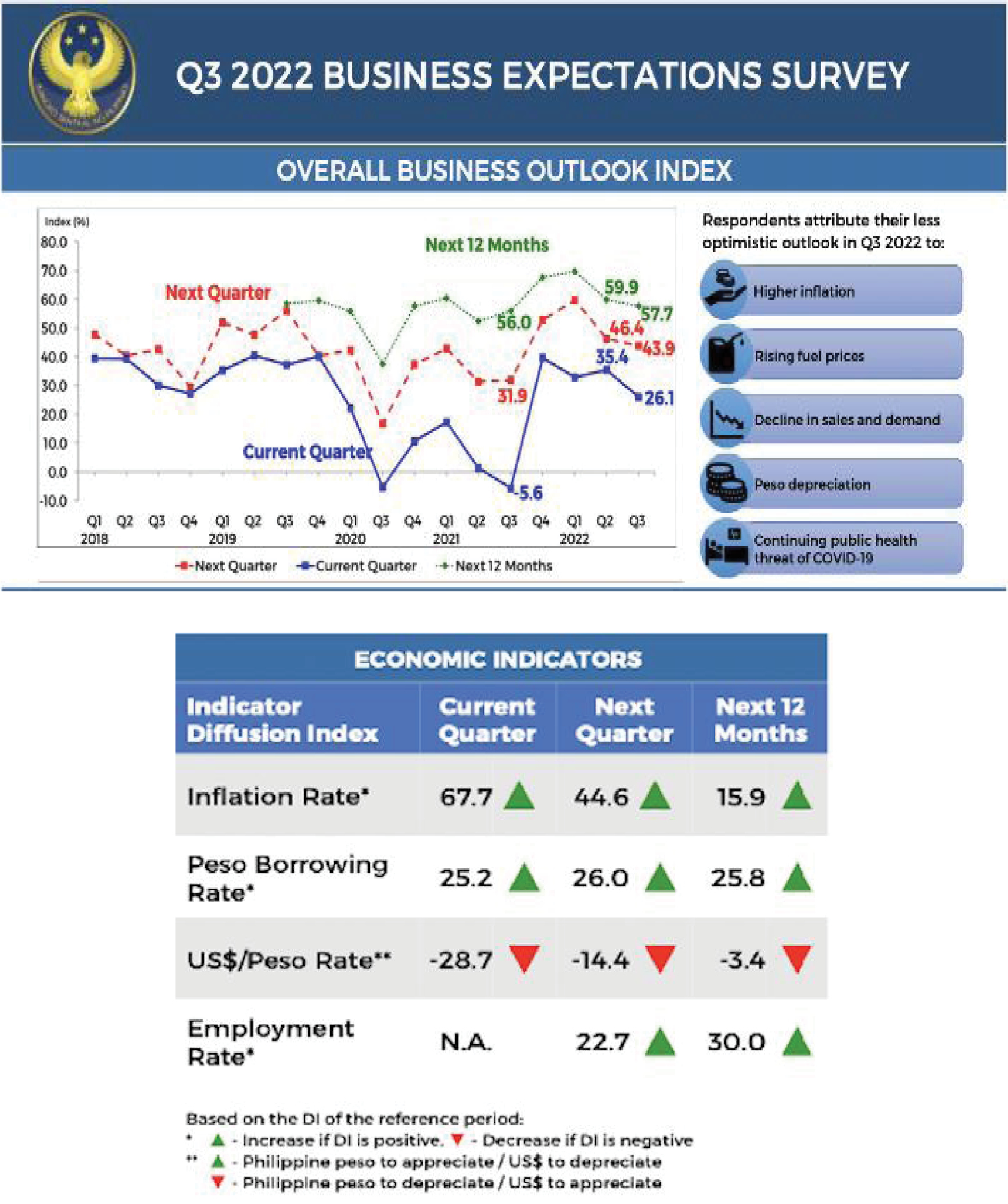

Based on the Bangko Sentral ng Pilipinas’ (BSP) Business Expectations Survey (BES) for the third quarter of 2022 conducted between July 6 to Aug. 15, overall business sentiment dropped for the same quarter, next quarter, and the next 12 months.

This quarterly survey has been reliable in terms of the representativeness of its sample as well as the reasonable correlation between business sentiment and actual economic growth. Loosely, the results may be considered good predictor of economic growth. If we take the BES as a proxy for gross capital formation in the national income accounts, it covers 25% of total gross domestic product (GDP). The BES is useful for planning purposes because the actual national income accounts are available only after more than two months from the subject quarter.

Respondent firms are drawn at random from the list of Top 7,000 corporations ranked based on total assets. The BSP represents in its regular survey results that BES provides “advance indication of the direction of change in overall business activity in the (Philippine) economy and in the various companies’ operations as well as in selected economic indicators.”

If the third quarter 2022 BES results point to the south, these may not be exactly positive for the Philippines’ actual GDP numbers. The respondents explained their less optimistic sentiment in terms of five factors: one, higher inflation of consumer goods, services, raw materials and production costs; two, rising fuel prices; three, decline in sales and demand; four, peso depreciation; and five, continuing public scare of COVID-19.

Less optimism or more pessimism appears to be the more prevailing sentiment across the global economies. This spirit is pervasive because of the risk of recession on account of an unprecedented rise in inflation and the subsequent monetary tightening by central banks all over the world. Undue rise in consumer prices destroys the public’s purchasing power and disincentivizes business from expanding the scale of their operations and hiring more workers. This is how poverty and inequality are birthed and intensified.

China, Croatia, France, Germany, Greece, Hungary, Mexico, South Korea, and the United States also reported less optimistic business sentiment for the same quarter. While business sentiment was more optimistic in Australia, Bulgaria, Israel, and the Netherlands, it turned pessimistic in Brazil, Canada, and Thailand and more pessimistic in New Zealand and the United Kingdom.

For the fourth quarter 2022, Philippine businessmen were less optimistic about the prospects of doing business. The reasons are basically of the same cut: rising prices of relevant commodities; lower demand/sales of construction materials and medicines; higher fuel prices; weaker peso and higher interest rates; and the usual decline in business due to the rainy season.

What about the business prospects for the next 12 months?

As the chart shows for the two more forward-looking periods of reckoning — next quarter and the next 12 months — business sentiment is expected to trend lower. If we invoke the correlation between business sentiment and actual GDP, the slowdown of real GDP from the first to the second quarter might continue in the third quarter of this year and for the next 12 months. Those factors behind the weak business sentiment are just too overriding. In fact, for the next 12 months, business respondents also added the burning issue of “shortage in (the) supply of food and raw materials” like fuel and construction materials.

On specific business operations, the sentiment is discouraging. Firms expect their financial condition and access to credit to be tighter, showing an actual decline. The BSP noted in its report that this specific finding was consistent with the second quarter Senior Bank Loan Officers Survey (SLOS) which indicated “an expectation of a net tightening of overall credit standards for loans to enterprises for the third quarter 2022.”

For the fourth quarter 2022, the employment outlook looks dim. A decline was reported even as the prospects for the next 12 months are more optimistic. Among the business constraints were stiff domestic competition and insufficient demand.

All told, business respondents expect a weak peso, and higher borrowing and inflation rates for the third quarter. Their inflation rate expectation of 5.6% for the whole year 2022 coincides with the latest BSP forecast. While the average exchange rate expectation of P55.2 for the year is weaker than the emerging P53.02 for the first nine months of the year, for business purposes, the prevailing exchange rate might be more relevant considering that their operations are forward-looking. It is likely that the last quarter of the year could see the peso averaging at least P57 to a dollar.

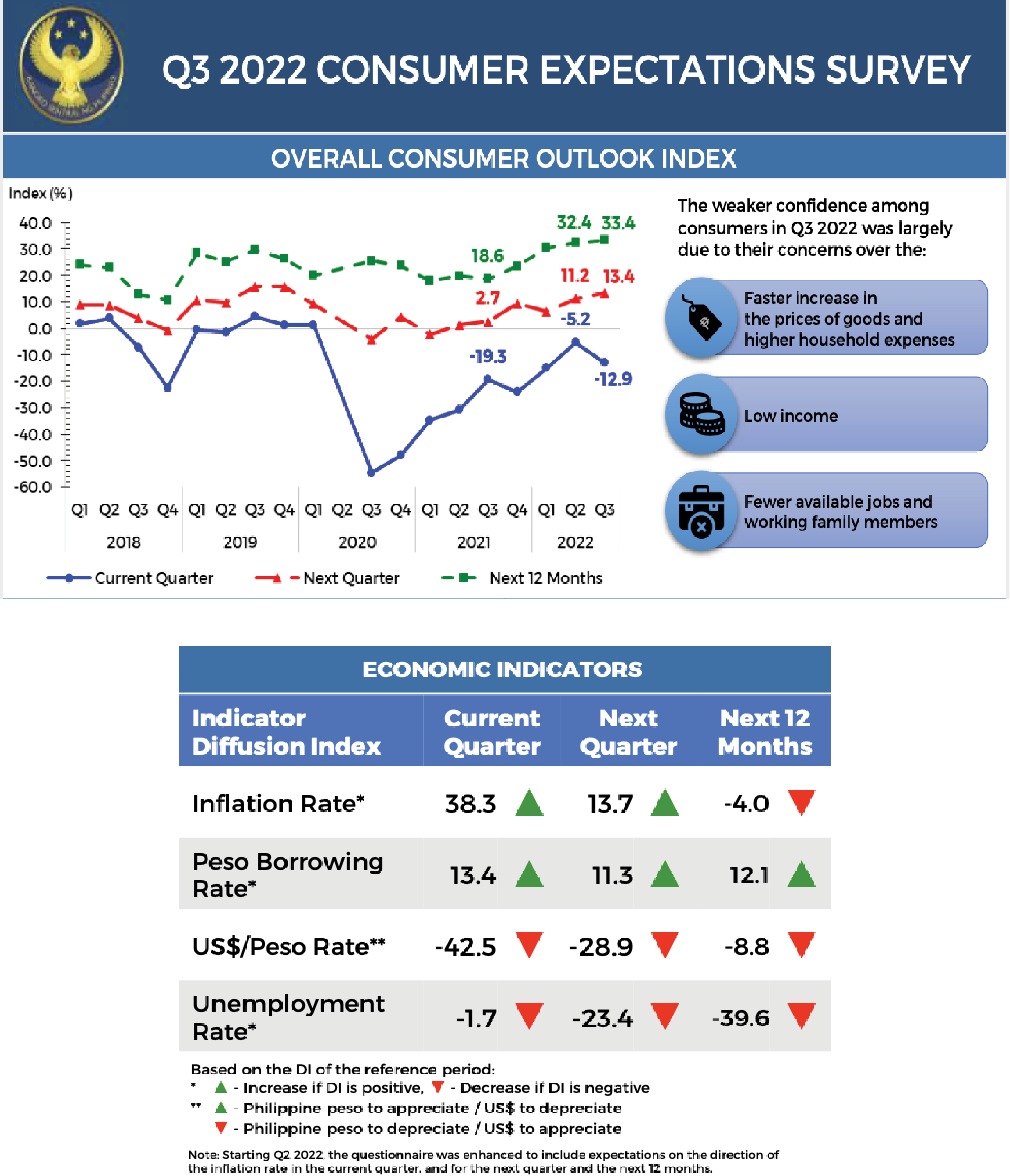

The other quarterly BSP survey covers the consumers as respondents. This is also an important survey because it gives us a glimpse of things to come from the consumption side of economic growth. Household consumption accounts for more than 70% of total GDP and therefore is the one big important driver of overall business activities. Consumer respondents are a random sample of some 5,000 households all over the Philippines.

The consumer outlook is based on three components namely, economic condition which captures their perception of the economic situation; family financial situation which covers the household income level, savings, debts, investment, and assets; and family income which includes primary income and receipts from other sources.

There is bad news and good news from our consumer expectations survey.

Bad news is the current quarter sentiment which turned more pessimistic as the index turned more negative, from -5.2 to -12.9. The reasons behind such pessimism are quite analogous with those of their business counterparts: higher inflation and household expenses; lower income; and limited job opportunities.

More countries also reported the prevailing negative sentiment for the third quarter particularly Australia, the Czech Republic, Finland, France, Italy, Japan, South Korea, Switzerland, and Taiwan.

The good news is that for the next quarter and 12 months, the consumer outlook index indicates more optimistic sentiment, being positive and rising. Consumer respondents point to more jobs, additional income, good governance, good public policies, and financial assistance.

It is also useful to know the consumers’ expectations about key economic indicators. For all the reckoning periods, they expect unemployment to decline — meaning, output growth could rise; interest rates to increase; and the peso-dollar rate to depreciate. As expected, households believe that inflation may rise this quarter and the next, breaching the official target of 2-4%. Inflation, however, is expected to ease in the next 12 months. This is consistent with the current BSP forecasts of 5.6% for this year and 4.1% next year although both are in excess of the target.

It will be a big challenge to deliver on this favorable household sentiment because the underlying assumptions require effective government policies, sufficient supply of goods and services, and stable health conditions. While IFIs could take the extra mile of encouraging their member countries to pursue sensible policy and structural reforms, it is our own political leaders and their economic managers who have the mandate to make things happen, and convert those conditional propositions of economic growth with price stability to reality.

True, Nobel laureate in Physics Niels Bohr was once quoted to have said “Prediction is very difficult, especially if it’s about the future.” For this very reason, it would be best for those in authority to take on Peter Drucker’s challenge that “the best way to predict your future is to create it.”

Diwa C. Guinigundo is the former deputy governor for the Monetary and Economics Sector, the Bangko Sentral ng Pilipinas (BSP). He served the BSP for 41 years. In 2001-2003, he was alternate executive director at the International Monetary Fund in Washington, DC. He is the senior pastor of the Fullness of Christ International Ministries in Mandaluyong.