I am pleased to share with readers a brief we posted to GlobalSource Partners (GSP) subscribers on the looming power shortage this summer. GSP (globalsourcepartners.com) is a network of independent analysts in emerging market countries. Christine Tang and I assisted by Shane Sia) are their local partners.

“The country entered 2022 with typhoon-related damage to power facilities that could lead to reserve shortfalls (yellow alerts) in the Luzon and Visayas grids. This came on top of outstanding issues related to the contracting of reserve power and the looming expiry of the supply agreement of the 1,200-megawatt (MW) Ilijan power plant fueled by Malampaya gas. Now two weeks in, power sector players are again in crisis management mode following Indonesia’s coal export ban, with the energy department joining other countries in the region in urging Indonesia to lift the ban.

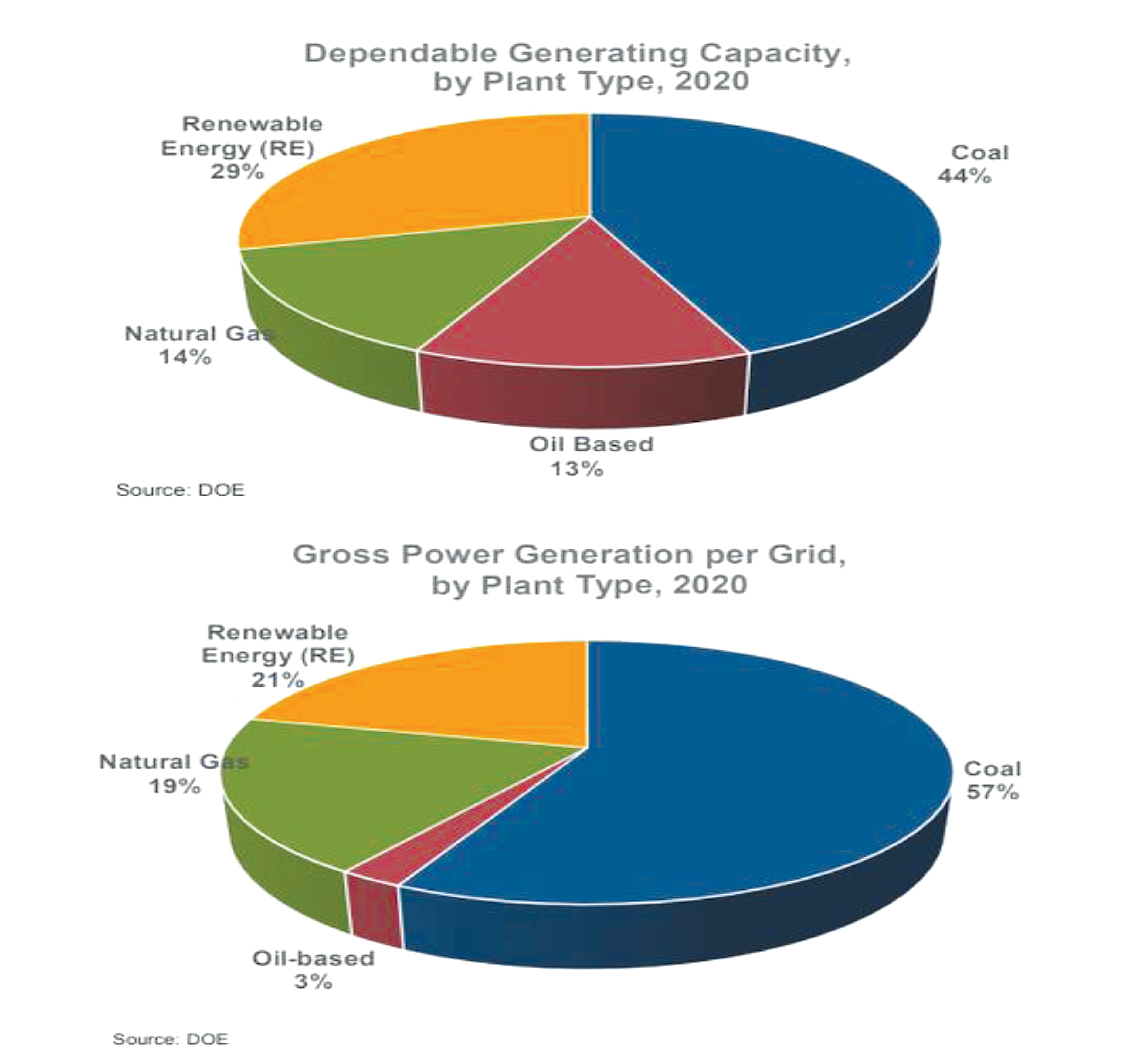

“Indonesia supplies over 95% of the Philippine’s coal imports. Coal-based plants, which comprise 44% of the power sector’s dependable capacity in 2020 and close to 60% of power generation, rely mainly on Indonesian coal. Although Indonesia has started to allow coal shipments to other countries in the region, industry players tell us that the Philippines is not among the priority destination countries. Reports indicate that with some plants scheduled for maintenance shutdown, available coal stocks may still last three weeks to two months, which from an aggregate perspective would tide the country over until the lifting of the export ban at end-January. (See the figures.)

“That however has not stopped understandably concerned power plant operators from planning for contingencies associated with logistical delays through purchases of coal in the spot market. There is after all no assurance at this time that the ban will not be extended nor that their orders will be placed ahead of the queue of countries trying to secure their own supplies; buyers that include heavyweights China and Japan. Although sourcing coal supplies from other countries is always an option, technical experts tell us that the closest alternative, Australian coal, costs more because of the higher quality, and is not even a perfect substitute, i.e., the plants were not designed to run on it.

“There is also the worry that this episode will be a precedent that will be repeated in the future considering all the uncertainties related to global climate change policy. Hence, the more policy-oriented are also urging government to make good use of strong neighborly ties to formalize an energy cooperation agreement with Indonesia or under the ASEAN framework to bolster Philippine energy security. As it is, concerns over medium-term energy security are growing with the Malampaya service contract ending in 2024 and estimates suggesting that remaining reserves would last only a few more years thereafter.

“The government has rightly stressed attracting new investments as a necessary condition for the economy’s post-pandemic recovery. Survey after survey of investment climates reveal the importance of quality infrastructure, including power supply stability, for attracting FDI.

“Yet, this early in the new year, private players, including the transmission company NGCP (National Grid Corporation of the Philippines), the power sector’s system operator, are already again warning of thin supplies in the summer months and calling for demand side management.” (End of GSP post.)

There are short term demand management measures to mitigate the impact of a possible summer power shortage, such as tapping the backup generation capacity of big firms, voluntary shifting of operations (peak/off peak pricing), interruptible load programs (first employed by Veco [Visayan Electric Company], now Meralco), and in the worst case, rotating brownouts for non-critical areas.

In addition, firm contracting of ancillary services (to protect us from potential blackouts resulting from a lack of supply because it ensures that ancillary services are allocated from a separate pool of capacity), prioritization by NGCP of critical transmission lines, i.e., Dinginin, Negros-Cebu interconnection upgrading, Viz-Min interconnection, etc. will allow stranded generation to be dispatched.

The medium to long term solutions lie with creating the incentive framework and enforcing the regulations for needed transmission facilities and new power plants to be built. This includes lifting the caps on WESM (Wholesale Electricity Spot Market) pricing and allowing more imbedded generation, bypassing the high voltage transmission lines. Due to the influx of more variable renewable energy into the grid, regulators must revisit generation capacity, the mix of energy technologies, and energy storage requirements to ensure uninterrupted supply of power.

I have written on the subject in two earlier columns (“Red Alert and EPIRA,” June 13, 2021, https://www.bworldonline.com/red-alert-and-epira/ and “It’s not easy being green: balancing energy security and de carbonization in an emerging economy,” Nov. 7, 2021, https://www.bworldonline.com/its-not-easy-being-green-balancing-energy-security-and-decarbonization-for-an-emerging-economy/).

EXCERPTING SOME KEY POINTS: On the regulatory regime (from “Red Alert and EPIRA”):

1.) “Our regulators play an important role in seeing to it that the rules are properly enforced. On this front, I can only describe our regulator’s approach as schizophrenic, where they have tended to over-regulate the competitive part of the industry and under-regulate the regulated part of the industry.

“EPIRA designed the power generation side to be competitive, and allow competition to yield lower prices and higher reliability. There are rules in place, including market power restrictions, to keep any one player from unfairly prejudicing the consumer. Unfortunately, since then, the regulators have churned out regulation after regulation to curb the activities of generators. Each regulation is designed with the consumer in mind, but, as with many regulations and laws, they often carry unintended consequences that distort the behavior and incentives of market participants. When investors do not build new plants or do so slowly because the business environment has been riddled with regulatory uncertainty and risks, end consumers and our entire economy lose.”

2.) “On the other hand, the regulators have fallen short in its responsibility to enforce the rules over NGCP, which has the monopoly over the transmission lines in the country. Our regulators should focus on regulating the regulated business of transmission of power and consider simplifying the rules for gencos to allow the market to work, to de-risk the environment and to attract more long-term private capital. In order to ensure that we have adequate reserves, the regulators should compel the Systems Operator to contract the full, firm reserve requirement. This can be done within 30 days, as there are genco offers today sitting on the desks at NGCP. This would ensure that we have the spare reserves the next time that the supply of power thins.

“Lastly, we need to fast track the implementation of the transmission line network. A three to four-year year lag creates significant uncertainty and an imbalance in the market. Correcting this will de-risk the investment environment and will encourage the entry of more power capacity into the grid.”

On the managing de-carbonization and the energy transition for the Philippines (from “It’s not easy being green…”):

1.) “A key consideration is intermittency of new solar and wind. Given the current state of technology and cost of battery storage, only fossil fuels can provide the Philippine base load capacity needed to drive industry. Especially required now as we try to recover from this pandemic — we need secure and affordable power to attract investment and quality jobs to lift the quarter of our people who are jobless and in absolute poverty.

2.) “…We are expected to be hard hit by adverse effects of climate change and therefore will need to invest considerably in adapting to what is a global crisis that we alone cannot solve. All of this points to the conclusion that we should bear considerably less of the cost of the transition than other countries. To his credit, Finance Secretary Carlos Dominguez III has recently publicly taken developed countries to task on this matter. Ultimately, we all share a common goal but our responsibilities will vary. Let’s learn from the experiences in the developed world and avoid quick-fix pathways and craft an energy transition with the Filipino people in mind and that the Filipino people can afford.”

3.) “Our power regulators, financial regulators, and other public stewards should be mindful of the tradeoffs and high stakes in climate-related decisions. We all dislike coal and other carbon intensive industries, but we should dislike seeing our people in abject poverty even more.”

Romeo L. Bernardo was finance undersecretary during the Cory Aquino and Fidel Ramos Administrations. He serves as a trustee/director in the Foundation for Economic Freedom, the Management Association of the Philippines, and the FINEX Foundation. He is an independent director in a diversified publicly listed holding company with major investments in power generation (both fossil fuels and renewables) and distribution. The views herein are his.